PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959322

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959322

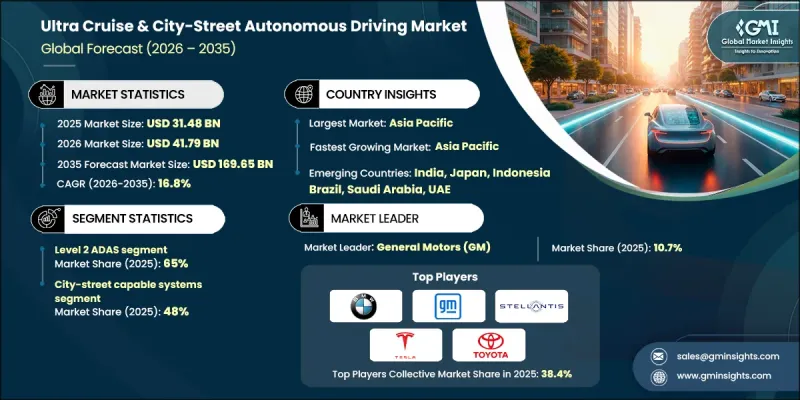

Ultra Cruise and City-Street Autonomous Driving Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Ultra Cruise & City-Street Autonomous Driving Market was valued at USD 31.48 billion in 2025 and is estimated to grow at a CAGR of 16.8% to reach USD 169.65 billion by 2035.

The integration of advanced hands-free driving and city-level automation is reshaping vehicle design, embedded software frameworks, and next-generation mobility solutions. Automakers are moving away from isolated driver-assistance features toward adaptive, software-defined driving platforms that support progressively higher autonomy while retaining human supervision. Urban driving conditions, including congestion, unpredictable road users, and inconsistent infrastructure, are placing higher performance demands on city-street autonomous systems. These solutions rely on sophisticated sensor integration, continuous environment perception, and high-speed computing to manage intersections, traffic signals, lane changes, and complex traffic flows. Because vehicles operate within defined operational design domains, such technologies are essential for extending autonomy beyond limited-access roads into everyday urban use. Automakers and technology providers are heavily investing in scalable autonomy stacks that emphasize safety, reliability, and gradual feature expansion through software updates rather than full automation deployment. This step-by-step approach supports regulatory alignment, consumer trust, and faster commercialization.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.48 Billion |

| Forecast Value | $169.65 Billion |

| CAGR | 16.8% |

The Level 2 ADAS segment held a 65% share in 2025 and is projected to grow at a CAGR of 16.5% through 2035. This segment leads due to its ability to deliver advanced automated functionality while maintaining driver oversight, making regulatory approval and market rollout more practical across regions. Existing safety standards, liability frameworks, and certification processes strongly favor supervised autonomy, enabling faster adoption compared to higher autonomy levels.

The city-street capable systems segment held 48% share in 2025 and is expected to register a CAGR of 17.8% between 2026 and 2035. These systems dominate because they address everyday driving environments where most vehicle usage occurs. Urban operation involves frequent stops, intersections, vulnerable road users, and mixed traffic conditions, making city-focused automation more valuable than highway-only solutions. Growing consumer demand for stress reduction in urban commuting, parking, and short-distance travel continues to accelerate adoption.

United States Ultra Cruise & City-Street Autonomous Driving Market held an 85% share, generating USD 9.2 billion in 2025. Market expansion in the U.S. remains strong, driven by continuous innovation in advanced driver assistance and supervised autonomy solutions, along with substantial investment from major automakers. A well-developed software-defined vehicle ecosystem is enabling manufacturers to extend hands-free driving capabilities beyond controlled highway environments into complex urban settings. This progress is supported by artificial intelligence-based perception systems, high-precision digital mapping, and over-the-air software updates that allow ongoing improvements in functionality, safety, and driving performance.

Key participants active in the Global Ultra Cruise & City-Street Autonomous Driving Market include NVIDIA, Toyota Motor, Continental, Mobileye, General Motors, Stellantis, BMW, Nissan Motor, and Mercedes-Benz Group. Companies in the ultra cruise and city-street autonomous driving market are strengthening their foothold through sustained investment in software-centric vehicle architectures and artificial intelligence-driven perception systems. Automakers are prioritizing modular autonomy platforms that allow features to scale across vehicle models and price segments. Strategic partnerships with semiconductor firms and software developers help accelerate processing performance and algorithm refinement. Many players emphasize over-the-air update capabilities to enhance system reliability and functionality post-sale. Extensive real-world data collection is used to improve urban driving accuracy and safety validation.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Autonomy Level

- 2.2.3 Operational Design Domain

- 2.2.4 Vehicle

- 2.2.5 Sensor Technology

- 2.2.6 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Hands-Free & Convenience-Driven Mobility

- 3.2.1.2 Advancements in AI, Sensor Fusion & Onboard Compute

- 3.2.1.3 OEM Shift Toward Software-Defined Vehicles (SDVs)

- 3.2.1.4 Expanding Urbanization & Traffic Complexity

- 3.2.1.5 Regulatory Support for Supervised Autonomy & ADAS Evolution

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High System Cost & Hardware Complexity

- 3.2.2.2 Regulatory Fragmentation Across Regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into Mid-Range & Mass-Market Vehicles

- 3.2.3.2 Subscription-Based & Feature-on-Demand Models

- 3.2.3.3 Integration with EV & Smart Mobility Ecosystems

- 3.2.3.4 Asia-Pacific Urban Autonomy Growth

- 3.2.3.5 Strategic Partnerships with AI, Mapping & Cloud Providers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 North America

- 3.3.1.1 United States: NHTSA Automated Driving Systems (ADS) Guidance & AV TEST Initiative

- 3.3.2 Europe

- 3.3.2.1 European Union: UNECE Regulation R157 (Automated Lane Keeping Systems - ALKS)

- 3.3.2.2 Germany: Autonomous Driving Act

- 3.3.2.3 United Kingdom: Connected and Automated Mobility (CAM) Regulations

- 3.3.2.4 France: Autonomous Vehicle Experimentation Framework

- 3.3.3 Asia Pacific

- 3.3.3.1 China: Intelligent Connected Vehicle (ICV) Simulation Standards

- 3.3.3.2 Japan: MLIT Automated Driving Safety Guidelines

- 3.3.3.3 South Korea: Autonomous Vehicle Act

- 3.3.3.4 Singapore: Autonomous Vehicle Safety Assessment Framework

- 3.3.4 Latin America

- 3.3.4.1 Brazil: National Intelligent Mobility & IoT Strategy

- 3.3.4.2 Mexico: Smart Mobility & Autonomous Vehicle Pilot Regulations

- 3.3.4.3 Chile: Intelligent Transport Systems (ITS) Policy

- 3.3.5 Middle East & Africa (MEA)

- 3.3.5.1 United Arab Emirates: Dubai Autonomous Transport Strategy

- 3.3.5.2 Saudi Arabia: Vision 2030 Smart Mobility Framework

- 3.3.5.3 South Africa: Green Transport & Automated Mobility Policy

- 3.3.1 North America

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Sustainability and environmental impact analysis

- 3.8.1 Sustainable practices

- 3.8.2 Waste reduction strategies

- 3.8.3 Energy efficiency in production

- 3.8.4 Eco-friendly initiatives

- 3.8.5 Carbon footprint considerations

- 3.9 Future outlook & opportunities

- 3.10 Human-machine interaction (HMI) & driver monitoring systems (DMS)

- 3.10.1 HMI design principles for autonomous systems

- 3.10.2 Driver monitoring system (DMS) technologies

- 3.10.3 Regulatory requirements for dms

- 3.10.4 User experience (Ux) challenges & solutions

- 3.10.5 Leading HMI/DMS technology providers

- 3.11 Data strategy & software stack economics

- 3.11.1 Data collection & management architecture

- 3.11.2 Software stack architecture

- 3.11.3 Software development economics

- 3.11.4 Data monetization strategies

- 3.11.5 Simulation & validation infrastructure

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Autonomy Level, 2022 - 2035 ($Bn, units)

- 5.1 Key trends

- 5.2 Level 2 ADAS

- 5.3 Level 3 ADAS

Chapter 6 Market Estimates & Forecast, By Operational Design Domain, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Highway-Only Systems

- 6.3 City-Street Capable Systems

- 6.4 Comprehensive / Door-to-Door Systems

Chapter 7 Market Estimates & Forecast, By Sensor Technology, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Camera-Based Systems

- 7.3 Radar-Based Systems

- 7.4 LiDAR-Enabled Systems

- 7.5 Multi-Sensor Fusion Systems

Chapter 8 Market Estimates & Forecast, By End-Use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Private / Personal Use

- 8.3 Ride-Hailing & Shared Mobility

- 8.4 Commercial Fleets

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger vehicle

- 9.2.1 Sedan

- 9.2.2 Hatchback

- 9.2.3 SUV

- 9.3 Commercial vehicle

- 9.3.1 LCV

- 9.3.2 MCV

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW

- 11.1.2 Continental

- 11.1.3 DENSO

- 11.1.4 General Motors (GM)

- 11.1.5 Mercedes-Benz

- 11.1.6 Mobileye

- 11.1.7 Nissan Motor

- 11.1.8 NVIDIA

- 11.1.9 Robert Bosch

- 11.1.10 Stellantis

- 11.1.11 Tesla

- 11.1.12 Toyota Motor

- 11.2 Regional Players

- 11.2.1 Baidu

- 11.2.2 Honda Motor

- 11.2.3 Huawei Technologies

- 11.2.4 Hyundai Motor

- 11.2.5 NIO

- 11.2.6 Renesas Electronics

- 11.2.7 StradVision

- 11.2.8 Valeo

- 11.2.9 Ghost Autonomy

- 11.3 Emerging Players

- 11.3.1 Ambarella

- 11.3.2 Aptiv

- 11.3.3 Innoviz Technologies

- 11.3.4 Luminar Technologies

- 11.3.5 Magna International

- 11.3.6 NXP Semiconductors

- 11.3.7 Qualcomm Technologies

- 11.3.8 Sony Semiconductor Solutions

- 11.3.9 ZF Friedrichshafen