PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959331

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959331

Self-Healing Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

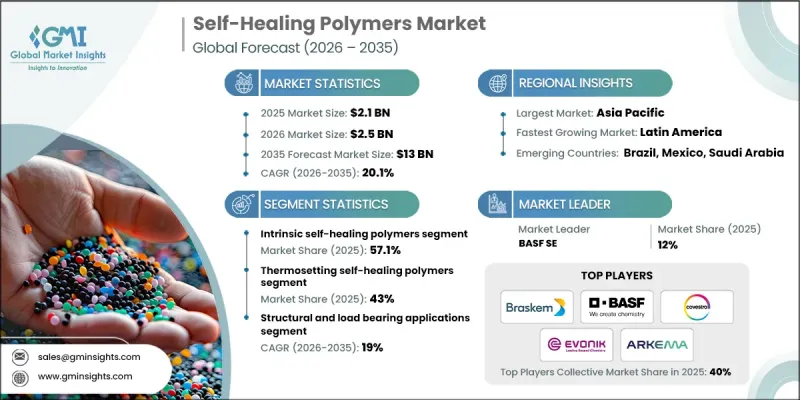

The Global Self-Healing Polymers Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 20.1% to reach USD 13 billion by 2035.

Self-healing polymers have evolved from early-stage laboratory concepts into commercially viable materials, particularly between 2022 and 2025, as industries increasingly focus on durability, lifecycle extension, and performance optimization. A noticeable rise in academic and technical publications referencing self-healing polymers indicates growing innovation around dynamic molecular networks and responsive chemical systems that enable autonomous material repair. This surge in research activity aligns with expanding industrial interest, as manufacturers seek advanced materials capable of restoring functionality after damage. The market benefits from rising demand for materials that reduce maintenance needs, minimize downtime, and improve long-term reliability. As development efforts continue to shift from theoretical exploration to scalable production, self-healing polymers are being integrated into a wider range of high-value applications, supported by improved manufacturing techniques and increasing awareness of their economic and performance advantages.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $13 Billion |

| CAGR | 20.1% |

Within industrial manufacturing, self-healing polymers are increasingly adopted to address recurring material degradation challenges. These materials enable original equipment manufacturers to enhance component longevity by embedding repair mechanisms directly into coatings and composite systems, particularly in high-performance sectors. Market demand is also shifting toward materials that combine multiple functional properties within a single polymer system. Self-healing solutions are now designed to integrate mechanical recovery with additional performance attributes, enabling broader applicability across advanced material platforms. This multifunctional approach supports wider adoption by enabling manufacturers to simplify material complexity while enhancing overall system efficiency and reliability.

The thermosetting self-healing polymers segment accounted for held 43% share in 2025 and is projected to grow at a CAGR of 19.6% from 2026 to 2035. The market landscape shows increasing alignment between polymer system selection and end-use requirements rather than reliance on generalized material platforms. Thermosetting systems remain dominant in applications requiring structural integrity and surface protection, while thermoplastic and elastomeric systems support flexibility-driven use cases. Blend and interpenetrating network technologies enable tailored performance by balancing rigidity, toughness, ease of processing, and repeatable healing capability, further strengthening their commercial appeal.

The structural and load-bearing applications held 29.2% share in 2025 and are expected to grow at a CAGR of 19% through 2035. Adoption across structural, protective, electronic, biomedical, consumer, and energy-related segments continues to expand as organizations aim to lower total ownership costs and reduce operational interruptions. In load-bearing environments, self-healing functionality helps slow material fatigue and crack development, while protective applications emphasize surface restoration and resistance to environmental stressors. These performance benefits continue to drive integration across demanding operating conditions.

North America Self-Healing Polymers Market reached USD 652.5 million in 2025 to USD 1.9 billion by 2035 at a CAGR of 19.3%. Growth across the region is supported by strong adoption across coatings, advanced composites, and electronic materials, along with a well-established innovation ecosystem. The United States remains the central hub for commercialization activity, supported by close collaboration among material producers, research institutions, and manufacturing end users. These partnerships accelerate qualification processes and early-stage deployment across multiple high-performance applications.

Prominent participants in the Global Self-Healing Polymers Market include BASF SE, Arkema S.A., Covestro AG, The Dow Chemical Company, Evonik Industries AG, Huntsman Corporation, DSM-Firmenich (formerly Royal DSM), 3M Company, Henkel AG & Co. KGaA, AkzoNobel N.V., SABIC, LG Chem Ltd., Mitsubishi Chemical Group, Toray Industries, Inc., Sumitomo Chemical Co., Ltd., and Nippon Paint Holdings Co., Ltd. Companies active in the self-healing polymers market employ a combination of strategic initiatives to strengthen their competitive positioning. Investment in research and development remains a primary focus, enabling firms to improve healing efficiency, durability, and compatibility with existing manufacturing processes. Strategic partnerships with industrial end users support faster commercialization and application-specific customization. Many companies expand production capabilities to support scaling and cost optimization. Portfolio diversification across coatings, composites, and advanced materials allows suppliers to address multiple industries. Sustainability-focused innovation, including extended material lifespans and reduced maintenance requirements, further enhances market acceptance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Healing mechanism

- 2.2.3 Polymer matrix type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Healing mechanism

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Healing mechanism, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Intrinsic self-healing polymers

- 5.2.1 Reversible covalent bond-based systems

- 5.2.2 Supramolecular (non-covalent) interaction-based systems

- 5.2.3 Dynamic crosslinked networks

- 5.2.4 Thermally reversible networks

- 5.3 Extrinsic self-healing polymers

- 5.3.1 Microcapsule-based systems

- 5.3.2 Vascular or microchannel-based systems

- 5.3.3 Particulate or phase-separated healing agents

- 5.3.4 Embedded shape-memory or stimulus-triggered systems

Chapter 6 Market Estimates and Forecast, By Polymer matrix type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Thermosetting self-healing polymers

- 6.3 Thermoplastic self-healing polymers

- 6.4 Elastomeric self-healing polymers

- 6.5 Polymer blends and interpenetrating networks

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Structural and load-bearing applications

- 7.3 Protective coatings and paints

- 7.4 Electronics and soft devices

- 7.5 Biomedical and healthcare applications

- 7.6 Consumer goods and textiles

- 7.7 Energy and environmental applications

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Covestro AG

- 9.3 Evonik Industries AG

- 9.4 Arkema S.A.

- 9.5 Huntsman Corporation

- 9.6 The Dow Chemical Company

- 9.7 3M Company

- 9.8 AkzoNobel N.V.

- 9.9 Henkel AG & Co. KGaA

- 9.10 DSM-Firmenich (formerly Royal DSM)

- 9.11 LG Chem Ltd.

- 9.12 SABIC

- 9.13 Mitsubishi Chemical Group

- 9.14 Toray Industries, Inc.

- 9.15 Sumitomo Chemical Co., Ltd.

- 9.16 Nippon Paint Holdings Co., Ltd.