PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959333

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959333

Industrial Actuators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

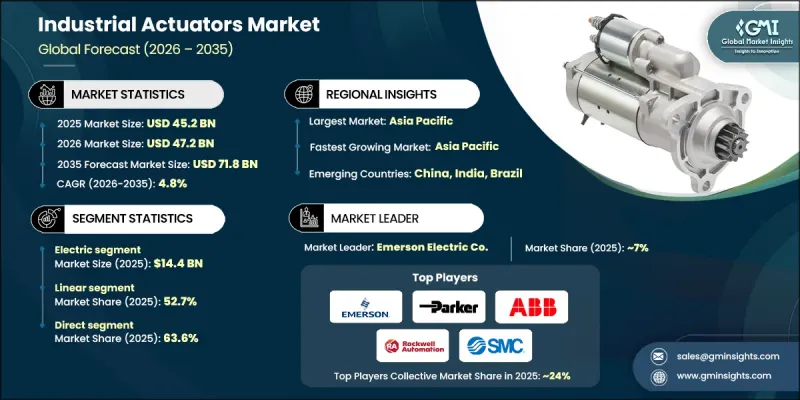

The Global Industrial Actuators Market was valued at USD 45.2 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 71.8 billion by 2035.

The growth reflects the increasing adoption of automated production systems designed to enhance operational efficiency, improve precision, and support scalable manufacturing output. Actuators enable controlled motion within automated equipment, making them a foundational element of modern motion control systems. As automation deepens across production environments, reliance on actuator technology continues to intensify. Ongoing advancements in manufacturing processes are prompting consistent upgrades in actuator design, performance, and integration capabilities. Manufacturers increasingly define their productivity and efficiency goals around automation readiness, which directly elevates the importance of advanced actuator solutions. Continuous innovation in actuator technology is therefore expected to remain central to the evolution of industrial automation worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.2 Billion |

| Forecast Value | $71.8 Billion |

| CAGR | 4.8% |

The electric actuators segment generated USD 14.4 billion in 2025 and is expected to grow at a CAGR of 4.6% from 2026 to 2035. These systems are gaining preference due to higher energy efficiency, reduced servicing requirements, and smooth compatibility with digital control platforms. Compared to hydraulic and pneumatic alternatives, electric actuators consume less energy and support more precise motion control. Their ability to integrate with sensors, connected systems, and predictive monitoring tools supports modern automation frameworks and sustainability goals. The advantages position electric actuators as a primary choice for future automation investments.

The linear actuator segment accounted for 52.7% share in 2025 and is forecast to grow at a CAGR of 4.1% through 2035. Linear actuators are valued for dependable performance, design simplicity, and broad functional adaptability. Their extensive deployment across industrial motion and flow control systems has established them as a dominant revenue contributor. The segment's strong position highlights the structural role linear motion solutions play within plant operations and equipment infrastructure.

U.S. Industrial Actuators Market reached USD 6 billion in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. The country holds a leading share within North America due to its advanced automation ecosystem and high demand for precision motion technologies. Strong investment in large-scale industrial infrastructure and process optimization continues to support actuator adoption. The market benefits from a mature manufacturing base that prioritizes efficiency, reliability, and advanced control capabilities.

Key companies operating in the Global Industrial Actuators Market include Parker Hannifin Corp, ABB, Emerson Electric Co., SMC Corporation, Rotork plc, Eaton Corporation plc, Rockwell Automation, Flowserve Corporation, Moog Inc., Festo AG & Co. KG, Curtiss-Wright, IMI Critical Engineering, KITZ Corporation, Tolomatic, Inc., and Venture MFG. Co. Companies in the industrial actuators market focus on technology innovation, portfolio expansion, and strategic partnerships to strengthen their market position. Many players invest heavily in research and development to enhance energy efficiency, precision, and digital compatibility. Integration of smart features such as condition monitoring and predictive maintenance is a key priority. Firms also pursue mergers, acquisitions, and collaborations to expand geographic reach and access new customer segments. Customization capabilities and application-specific solutions help suppliers differentiate their offerings. Additionally, manufacturers emphasize sustainability initiatives and compliance with evolving industrial standards to reinforce long-term competitiveness and customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Motion Type

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrial automation & robotics adoption

- 3.2.1.2 Demand for energy-efficient & precise control systems

- 3.2.1.3 Growth of smart manufacturing (industry 4.0)

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High cost of advanced actuators

- 3.2.2.2 Requirement for skilled professionals

- 3.2.3 Opportunities

- 3.2.3.1 Rising adoption of electric actuators

- 3.2.3.2 Expansion in Asia Pacific & emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US: Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.2 Canada: International Organization for Standardization (ISO) 4210

- 3.7.2 Europe

- 3.7.2.1 Germany: Deutsches Institut fur Normung (DIN) European Norm (EN) ISO 4210

- 3.7.2.2 UK: European Norm (EN) ISO 4210 / United Kingdom Conformity Assessed (UKCA)

- 3.7.2.3 France: European Norm (EN) ISO 4210

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Guobiao (GB) 3565

- 3.7.3.2 India: Indian Standard (IS) 10613

- 3.7.3.3 Japan: Japanese Industrial Standard (JIS) D 9110

- 3.7.4 Latin America

- 3.7.4.1 Brazil: Associacao Brasileira de Normas Tecnicas (ABNT) Norma Brasileira (NBR) ISO 4210

- 3.7.4.2 Mexico: International Organization for Standardization (ISO) 4210

- 3.7.5 Middle East & Africa

- 3.7.5.1 South Africa: South African National Standard (SANS) 311

- 3.7.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization (SASO) Gulf Standardization Organization (GSO) ISO 4210

- 3.7.1 North America

- 3.8 Trade statistics (HS code- 84819090)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Electric

- 5.3 Pneumatic

- 5.4 Hydraulic

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Motion Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Linear

- 6.3 Rotary

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Valves

- 7.3 Pumps

- 7.4 Dampers

- 7.5 Conveyors

- 7.6 Robotics

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Oil & gas

- 8.3 Power generation

- 8.4 Water & wastewater treatment

- 8.5 Chemical & petrochemical

- 8.6 Food & beverage

- 8.7 Pharmaceuticals

- 8.8 Mining & metals

- 8.9 Automotive & manufacturing

- 8.10 Aerospace & defense

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Curtiss-Wright

- 11.3 Eaton Corporation plc

- 11.4 Emerson Electric Co.

- 11.5 Festo AG & Co. KG

- 11.6 Flowserve Corporation

- 11.7 IMI Critical Engineering

- 11.8 KITZ Corporation

- 11.9 Moog Inc.

- 11.10 Parker Hannifin Corp

- 11.11 Rockwell Automation

- 11.12 Rotork plc

- 11.13 SMC Corporation

- 11.14 Tolomatic, Inc.

- 11.15 Venture MFG. Co.