PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959335

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959335

Mobile Car Crusher Trailer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

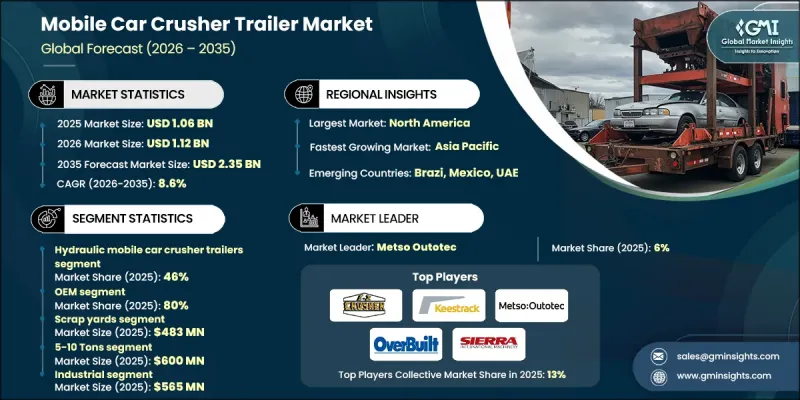

The Global Mobile Car Crusher Trailer Market was valued at USD 1.06 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 2.35 billion by 2035.

The market continues to gain momentum as rising vehicle retirement rates worldwide increase the need for faster and more efficient recycling processes. Tighter environmental policies and End-of-Life Vehicle compliance requirements are pushing recycling operators to modernize their crushing infrastructure. Scrap yards, vehicle dismantlers, and industrial recycling facilities are increasingly focused on improving productivity, lowering emissions, and meeting safety obligations, which is accelerating demand for advanced mobile crusher trailers. The growing shift toward on-site crushing is also reducing transportation costs and operational delays. Large-scale recycling facilities and multi-site scrap operators are actively investing in mobile, high-capacity, and modular crusher trailers to maintain flexibility and operational control. Market growth is further supported by increasing adoption of hydraulic, electric, and diesel-powered systems designed to handle diverse vehicle types while delivering consistent performance across varied operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.06 Billion |

| Forecast Value | $2.35 Billion |

| CAGR | 8.6% |

Ongoing innovation is reshaping mobile car crusher trailer operations through intelligent process controls, digitally enabled performance monitoring, automated safety mechanisms, and advanced power systems. These improvements enhance crushing accuracy, increase throughput, and improve material recovery while ensuring compliance with environmental and workplace standards. The integration of modular trailer structures and predictive maintenance tools is extending equipment lifespan and reducing downtime. Energy-efficient electric and hybrid crusher systems are also helping operators reduce fuel dependency and emissions, allowing them to achieve higher operational efficiency and lower long-term costs while aligning with evolving sustainability targets.

Hydraulic mobile car crusher trailers accounted for roughly 46% of the total market share in 2025 and are projected to grow at a CAGR exceeding 8.4% from 2026 to 2035. This segment continues to lead due to its ability to deliver controlled, high-force crushing with minimal manual handling. Operators favor hydraulic systems for their reliability, adaptability to different vehicle sizes, and enhanced safety performance, particularly in high-volume scrappage environments and operations managing multiple sites.

The OEM segment held 80% share in 2025 and is forecast to grow at a CAGR of 8.8% through 2035. OEM dominance is driven by direct access to fully engineered and certified crusher trailers that offer durability, customization options, and integrated compliance features. End users prioritize OEM solutions for their warranty coverage, technical support, and ability to meet strict operational and regulatory standards, making them the preferred procurement choice across large recycling networks.

United States Mobile Car Crusher Trailer Market held 83% share and reached USD 314.6 million in 2025. The region benefits from a well-established vehicle recycling infrastructure and widespread deployment of advanced mobile crushing technologies. Strong investment in automation, digital monitoring, and high-capacity trailer solutions continues to position North America at the forefront of efficient and technology-driven vehicle recycling.

Key companies active in the Global Mobile Car Crusher Trailer Market include Metso Outotec, Sandvik, Al jon Manufacturing, Sierra International Machinery, Eagle Crusher Company, McCloskey International, OverBuilt, EZ Crusher, Hammel Recyclingtechnik, and Keestrack. Companies operating in the mobile car crusher trailer market are strengthening their market position through continuous product innovation, strategic equipment upgrades, and expanded service offerings. Manufacturers are focusing on developing higher-capacity trailers with improved energy efficiency and advanced control systems to meet evolving customer demands. Many players are investing in modular designs and smart monitoring technologies to enhance flexibility and reduce maintenance costs. Strategic partnerships with recycling operators and regional distributors are helping companies expand their geographic reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power Source

- 2.2.3 Capacity

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Vehicle Scrappage & Recycling Needs

- 3.2.1.2 Technological Advancements

- 3.2.1.3 Environmental & Regulatory Compliance

- 3.2.1.4 Expansion of Industrial & Scrap Yard Operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment & Maintenance Costs

- 3.2.2.2 Fragmented Market & Limited Standardization

- 3.2.3 Market opportunities

- 3.2.3.1 Rising Demand for On-Site and Portable Recycling

- 3.2.3.2 Emerging Markets & Untapped Regions

- 3.2.3.3 Electric & Hybrid Crusher Trailers

- 3.2.3.4 Sustainability and Circular Economy Focus

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, OSHA, and RCRA Compliance Guidelines

- 3.4.1.2 Canada Revenue Agency (CRA) & Environment and Climate Change Canada Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry for the Environment & ELV Regulations

- 3.4.2.2 France: Ministry of Ecological Transition & ELV Guidelines

- 3.4.2.3 UK: Environment Agency & Waste Regulations

- 3.4.2.4 Italy: Ministry of Environment & ELV Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Ecology and Environment Standards

- 3.4.3.2 Japan: Ministry of Economy, Trade and Industry & ELV Recycling Law

- 3.4.3.3 South Korea: Ministry of Environment & ELV Regulations

- 3.4.3.4 India: Ministry of Environment, Forest and Climate Change & Vehicle Scrappage Policy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Environment Council (CONAMA) & Recycling Standards

- 3.4.4.2 Mexico: SEMARNAT Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Environment Agency - Abu Dhabi & Federal Standards

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hydraulic Mobile Car Crusher Trailers

- 5.3 Diesel-Powered Mobile Car Crusher Trailers

- 5.4 Electric Mobile Car Crusher Trailers

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 5-10 Tons

- 6.3 Up to 5 Tons

- 6.4 Above 10 Tons

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Scrap Yards

- 7.3 Automotive Recycling

- 7.4 Construction & Demolition

- 7.5 Emergency Response

- 7.6 Military

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Commercial

- 8.4 Municipal

- 8.5 Other

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Al-jon Manufacturing

- 11.1.2 Eagle Crusher Company

- 11.1.3 EZ Crusher

- 11.1.4 Hammel Recyclingtechnik

- 11.1.5 Keestrack

- 11.1.6 McCloskey International

- 11.1.7 Metso Outotec

- 11.1.8 OverBuilt

- 11.1.9 Sandvik

- 11.1.10 Sierra International Machinery

- 11.2 Regional Player

- 11.2.1 BENLEE

- 11.2.2 Big Mac

- 11.2.3 Enerpat

- 11.2.4 Gensco Equipment

- 11.2.5 Granutech-Saturn Systems

- 11.2.6 RM Johnson Company

- 11.2.7 SAS of Luxemburg

- 11.2.8 The Auto Crusher

- 11.2.9 VYKIN Crushers

- 11.2.10 Youngs Auto Center & Salvage

- 11.3 Emerging Players

- 11.3.1 Baichy Heavy Industrial Machinery

- 11.3.2 Fabo Company

- 11.3.3 Guangxi Mesda Engineering Machinery

- 11.3.4 SBM Mineral Processing

- 11.3.5 Senya Crushers