PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959338

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959338

Europe Outdoor Power Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

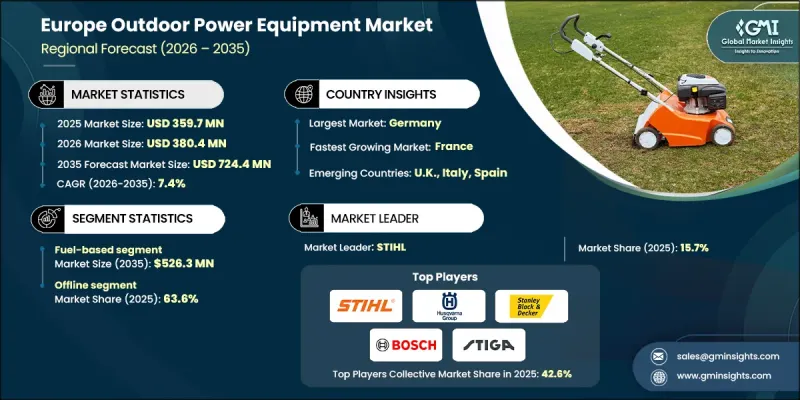

Europe Outdoor Power Equipment Market was valued at USD 359.7 million in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 724.4 million by 2035.

The market's growth is fueled by rising demand for equipment to maintain gardens, lawns, and landscaped areas across residential and commercial settings. Urbanization, increasing environmental awareness, and sustainability initiatives are encouraging the adoption of energy-efficient and low-emission equipment. Technological advancements, particularly in robotics and AI, are transforming the market, with manufacturers focusing on smart, connected solutions. The use of robotic lawnmowers and automated equipment is increasing as they provide greater convenience, efficiency, and ease of operation. Although weather conditions such as heavy rain and snowfall can limit equipment usage and temporarily impact revenues, consistent product innovation and digital integration are enabling the market to overcome these challenges. As urban green spaces expand, the need for reliable, high-performance outdoor power tools is expected to sustain long-term growth across Europe.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $359.7 Million |

| Forecast Value | $724.4 Million |

| CAGR | 7.4% |

In 2025, the fuel-based segment accounted for USD 258.2 million and is projected to reach USD 526.3 million by 2035. Fuel-powered equipment remains dominant due to its reliability, high efficiency, and ability to handle demanding tasks in forestry, landscaping, and large-scale maintenance projects. Professional users continue to prefer fuel-powered solutions for their extended operational time and robust performance compared to electric or battery-powered alternatives. According to the European Environmental Agency, nearly 58% of heavy-duty equipment sold in 2023 was fuel-based, highlighting continued reliance on these tools for challenging outdoor tasks.

The offline sales segment held 63.6% share in 2025. The preference for in-store purchases is driven by the ability of customers to physically inspect equipment, evaluate performance, and confirm quality before buying. Hands-on experiences allow buyers to build confidence in their purchases, while personalized guidance from trained sales staff ensures tailored recommendations and optimal equipment selection. Offline retail channels remain critical in establishing trust and providing post-purchase support, which strengthens customer loyalty and satisfaction.

Germany Outdoor Power Equipment Market held 19.1% share in 2025. Market growth in Germany is supported by widespread private gardens, well-maintained public green spaces, and significant investments in landscaping and municipal maintenance. The country's strong DIY culture, high disposable income, and frequent replacement cycles for mowers, trimmers, and chainsaws further drive demand. Additionally, environmental and noise regulations are encouraging the shift toward battery-powered and low-emission solutions. Government investments in sustainable urban infrastructure, parks, and recreational areas further boost market growth by expanding demand for high-quality outdoor maintenance tools.

Key players operating in the Europe Outdoor Power Equipment Market include Husqvarna, Emak, Briggs and Stratton, Honda Motor, John Deere, STIHL, Makita, Einhell, Karcher, Robert Bosch, Stiga, Stanley Black and Decker, The Toro Company, Yamabiko, and Techtronic Industries. Companies in the Europe outdoor power equipment market are adopting multiple strategies to strengthen their presence and expand market share. They are heavily investing in research and development to introduce innovative solutions, including AI-enabled robotic lawnmowers, battery-powered alternatives, and smart connected devices. Expanding distribution networks across both online and offline channels ensures products reach a broader customer base, while personalized services and after-sales support improve consumer loyalty. Strategic collaborations with landscapers, municipal authorities, and professional users help firms secure recurring business.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Type

- 2.2.3 Power

- 2.2.4 End User

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for landscaping and gardening services

- 3.2.1.2 Growing adoption of robotic lawn mowers

- 3.2.1.3 Rapid growth in the construction sector

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High dependence on weather conditions

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Opportunities

- 3.2.3.1 Sustainability-driven solutions

- 3.2.3.2 Expansion in emerging markets with rising power equipment usage

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Power trends

- 3.6.1 By product type

- 3.6.2 By country

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code- 8467)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behaviour analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.2 Germany

- 4.2.3 France

- 4.2.4 UK

- 4.2.5 Italy

- 4.2.6 Spain

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Lawn Mower

- 5.2.1 Push-behind/Walk-Behind Lawn Mowers

- 5.2.2 Riding/Ride-on Lawn Mowers

- 5.2.3 Robotic Lawn Mowers

- 5.3 Chainsaw

- 5.4 Trimmer & Edger

- 5.5 Blowers

- 5.6 Tillers & Cultivators

- 5.7 Snow Throwers

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Power, 2022-2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Electric

- 6.3 Fuel Based

Chapter 7 Market Estimates & Forecast, By End User, 2022-2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial/Industrial

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-Commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Supermarkets/Hypermarkets

- 8.3.2 Specialty Stores

- 8.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 9 Market Estimates & Forecast, By Country, 2022-2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Germany

- 9.3 France

- 9.4 UK

- 9.5 Italy

- 9.6 Spain

Chapter 10 Company Profiles

- 10.1 Briggs and Stratton

- 10.2 Einhell

- 10.3 Emak

- 10.4 Honda Motor

- 10.5 Husqvarna

- 10.6 John Deere

- 10.7 Karcher

- 10.8 Makita

- 10.9 Robert Bosch

- 10.10 STIHL

- 10.11 Stanley Black and Decker

- 10.12 Stiga

- 10.13 Techtronic Industries

- 10.14 The Toro Company

- 10.15 Yamabiko