PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959549

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959549

Lawn and Garden Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

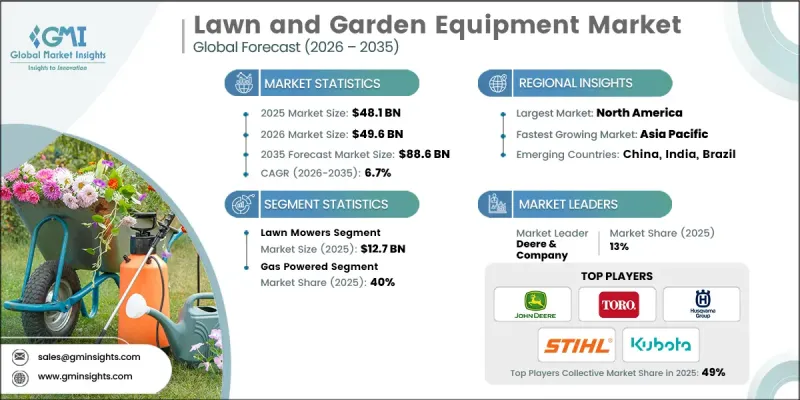

The Global Lawn and Garden Equipment Market was valued at USD 48.1 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 88.6 billion by 2035.

The industry is experiencing steady demand from residential consumers alongside rapid growth in commercial and institutional landscaping sectors. Urban expansion and new housing developments have transformed how homeowners perceive their outdoor spaces, particularly in suburban and peri-urban areas, making lawn and garden care a lifestyle activity rather than simple maintenance. This shift has driven demand for equipment that is user-friendly, ergonomic, multifunctional, and convenient. At the same time, commercial clients, including contractors, municipalities, and recreational facilities, continue to demand high-performance, durable, and productive equipment capable of heavy-duty use. Seasonal fluctuations still influence purchasing patterns, but strong dealer networks, rental programs, and comprehensive after-sales services now play a key role in boosting revenue and fostering customer loyalty. Technological advancements, particularly the rise of battery-powered and electric equipment, are reshaping the competitive landscape and supporting sustainable growth in the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $48.1 Billion |

| Forecast Value | $88.6 Billion |

| CAGR | 6.7% |

The lawn mowers segment generated USD 12.7 billion in 2025. Across both consumer and contractor segments, mowers are considered indispensable for maintaining well-manicured outdoor spaces, contributing to a sizable installed base and shorter replacement cycles compared to other lawn and garden tools. Consumers prioritize ease of use, efficiency, and consistent cutting performance, while contractors and commercial users demand high-capacity mowers capable of handling frequent, heavy-duty operation. The growing trend of landscaping as a lifestyle activity, coupled with increased suburbanization and emphasis on outdoor aesthetics, is further fueling demand for advanced mower designs, including self-propelled, robotic, and multi-functional models.

The gas-powered equipment segment held a 40% share in 2025. Renowned for their durability, high power output, and versatility, gas engines remain the equipment of choice for large properties, professional landscapers, and contractors who require long operational runtime, rapid refueling, and consistent performance on uneven or challenging terrain. Gas-powered mowers and trimmers excel in cutting dense or overgrown grass, making them indispensable for commercial landscaping operations, golf courses, sports fields, and expansive residential lawns. Despite the rising popularity of electric and battery-powered alternatives, gas-powered tools maintain their dominance due to reliability, heavy-duty endurance, and adaptability across diverse climates and work conditions.

U.S. Lawn and Garden Equipment Market held 80% share, generating USD 91 billion in 2025. Lawn and garden equipment demand is driven by a deep-rooted lawn care culture, high home ownership, and widespread suburban properties that require regular upkeep. Homeowners are motivated to maintain lawns and gardens to enhance curb appeal, preserve property values, and create functional outdoor living spaces, making daily or weekly maintenance a common routine.

Key players in the Global Lawn and Garden Equipment Market include Ariens Company, Briggs & Stratton Corporation, Deere & Company, Falcon Garden Tools, Fiskars Group, Honda Motor Co., Ltd, Husqvarna Group, Koki Holdings Co., Ltd, Kubota Corporation, Makita Corporation, Robert Bosch GmbH, Stanley Black & Decker, STIGA S.p.A, Stihl Holding AG & Co. KG, Techtronic Industries Co., Ltd (TTI), and The Toro Company. Companies in the Lawn and Garden Equipment Market are strengthening their foothold by focusing on product innovation, such as ergonomic designs, battery-powered solutions, and multifunctional tools. Expanding global distribution networks and forming strategic partnerships with dealers and service providers improve market reach and customer support. Investment in digital platforms, smart connectivity, and after-sales services enhances brand loyalty, while targeted marketing campaigns build awareness among both residential and commercial customers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 regional

- 2.2.2 product type

- 2.2.3 power

- 2.2.4 price

- 2.2.5 end user

- 2.2.6 distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Increasing interest in eco-friendly and sustainable products

- 3.2.1.3 Growth in home improvement and outdoor leisure activities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Technological advancements

- 3.2.2.2 Increasing interest in eco-friendly and sustainable products

- 3.2.2.3 Growth in home improvement and outdoor leisure activities

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for smart gardening tools

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 by product type

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirement

- 3.9.2 Certification standards

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Lawn mowers

- 5.3 Tractors

- 5.4 Sprinkler and hoses

- 5.5 Blowers

- 5.6 Chain saws

- 5.7 Cutters and shredders

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By power, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Gas powered

- 6.3 Electric powered

- 6.4 Manual

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By price, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Specialty stores

- 9.3.2 Home improvement stores

- 9.3.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Ariens Company

- 11.2 Briggs & Stratton Corporation

- 11.3 Deere & Company

- 11.4 Falcon Garden Tools

- 11.5 Fiskars Group

- 11.6 Honda Motor Co., Ltd

- 11.7 Husqvarna Group

- 11.8 Koki Holdings Co., Ltd

- 11.9 Kubota Corporation

- 11.10 Makita Corporation

- 11.11 Robert Bosch GmbH

- 11.12 Stanley Black & Decker

- 11.13 STIGA S.p.A

- 11.14 Stihl Holding AG & Co. KG

- 11.15 Techtronic Industries Co. Ltd (TTI)

- 11.16 The Toro Company