PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959551

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959551

Construction Equipment Rental Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

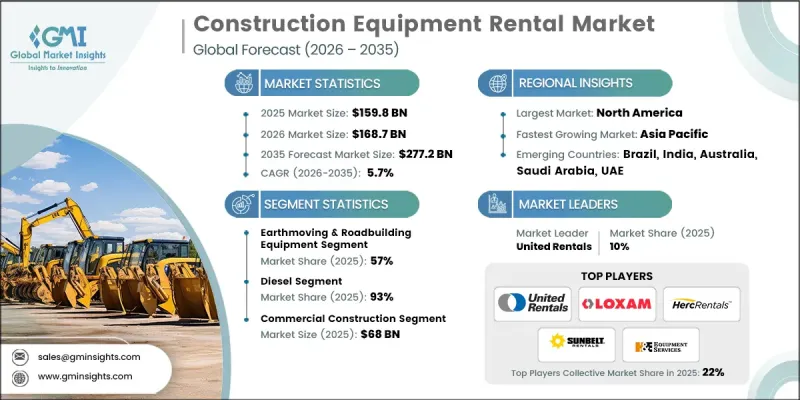

The Global Construction Equipment Rental Market was valued at USD 159.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 277.2 billion by 2035.

The industry is witnessing high demand for earthmoving, materials handling, and aerial lift equipment across residential, commercial, and large infrastructure projects. Small and mid-sized contractors are among the fastest adopters of rental solutions, while large contractors are increasingly using rented machinery to meet peak demands and access specialized equipment without long-term investment. Rental companies are shifting their business models, focusing on customer retention, service bundling, and predictable pricing. Expansion of fleets targeted to high-value sectors, such as renewable energy, tunneling, and major infrastructure, allows providers to offer purpose-built equipment, secure project-specific contracts, and develop loyal customer bases. This approach ensures rental companies can cater to evolving construction demands while improving operational efficiency and profitability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $159.8 Billion |

| Forecast Value | $277.2 Billion |

| CAGR | 5.7% |

The earthmoving and roadbuilding equipment segment held a 57% share in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. Companies are consolidating fleets and acquiring complementary businesses to provide diversified machinery options, expand regional presence, and serve larger established customer bases.

The diesel-powered equipment segment held a 93% share and is expected to grow at a CAGR of 5.2% between 2026 and 2035. Diesel machinery remains the preferred choice for heavy-duty operations due to its reliability, power, and efficiency in earthmoving, paving, and concrete applications. Rental fleets continue to focus on diesel-powered units to meet contractor needs in projects where electricity-based solutions are not feasible.

U.S. Construction Equipment Rental Market reached USD 75.6 billion in 2025. Growth in the U.S. is driven by robust infrastructure spending, mature commercial construction, and the established rental industry. Contractors increasingly rely on rental equipment to scale operations, reduce capital expenditure, and access specialized machinery for short-term or high-demand projects.

Key players operating in the Global Construction Equipment Rental Market include Allmand Brothers, Ashtead Technology (Sunbelt Rentals), Atlas Rents, Bakersfield Rental, Herc Rentals, JLG, John Deere Rental, Loxam, Ritchie Bros. Auctioneers, and United Rentals. Companies in the Construction Equipment Rental Market are strengthening their position by expanding regional and sector-specific fleets, acquiring complementary rental businesses, and offering bundled services with predictable pricing. Firms are investing in purpose-built equipment for high-value projects, forming strategic alliances with contractors, and leveraging digital platforms for equipment tracking and maintenance. Focus on customer loyalty programs, flexible rental terms, and specialized training services enhances client retention while improving operational efficiency. Emphasis on renewable energy, tunneling, and infrastructure sectors ensures access to premium contracts and market growth opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of connected and software-defined vehicles.

- 3.2.1.2 Rising consumer demand for personalization and hands-free operation

- 3.2.1.3 Expansion of EV and autonomous vehicle segments

- 3.2.1.4 Increasing aftermarket and software upgrade opportunities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Growing adoption of connected and software-defined vehicles.

- 3.2.2.2 Rising consumer demand for personalization and hands-free operation

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven predictive and generative assistants

- 3.2.3.2 Multimodal HMI adoption

- 3.2.3.3 Cloud connectivity and OTA updates

- 3.2.3.4 Regional adoption of intelligent cockpits

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 Occupational Safety and Health Administration (OSHA)

- 3.5.1.2 Environmental Protection Agency (EPA) Emission Standards

- 3.5.1.3 Transport Canada Workplace Safety & Equipment Regulations

- 3.5.2 Europe

- 3.5.2.1 EU Machinery Directive (MD) & CE Certification

- 3.5.2.2 EU Stage V Emission Standards

- 3.5.2.3 ISO 20474 (Earth-moving Machinery Safety Standards)

- 3.5.3 Asia-Pacific

- 3.5.3.1 Japan Industrial Safety & Health Act

- 3.5.3.2 China GB Standards for Construction Machinery

- 3.5.3.3 India AIS/Emission & Safety Guidelines

- 3.5.4 Latin America

- 3.5.4.1 Brazil INMETRO Certification

- 3.5.4.2 Colombia Ministry of Labor Safety Regulations

- 3.5.4.3 Argentina Construction Equipment Safety Guidelines

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Federal Authority for Human Resources & ESMA Standards

- 3.5.5.2 Oman Ministry of Labor Equipment Safety Regulations

- 3.5.5.3 South Africa SABS Construction Equipment Standards

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 OEM Pricing models

- 3.8.2 Aftermarket pricing trends

- 3.8.3 Subscription purchase models

- 3.8.4 Regional price variations

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Asset Utilization & Fleet Productivity Benchmarking

- 3.12 Electrification Readiness & Transition Roadmap

- 3.13 Rental Penetration & Ownership Shift Analysis

- 3.14 Digitalization & Telematics Impact Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Earthmoving & roadbuilding equipment

- 5.2.1 Backhoe

- 5.2.2 Excavator

- 5.2.3 Loader

- 5.2.4 Compaction equipment

- 5.2.5 Others

- 5.3 Material handling and cranes

- 5.3.1 Storage and handling equipment

- 5.3.2 Engineered systems

- 5.3.3 Industrial trucks

- 5.3.4 Bulk material handling equipment

- 5.4 Concrete equipment

- 5.4.1 Concrete pumps

- 5.4.2 Crusher

- 5.4.3 Transit mixers

- 5.4.4 Asphalt pavers

- 5.4.5 Batching plants

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 CNG/LNG

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.3 Commercial Construction

- 7.4 Industrial Construction

- 7.5 Mining & Quarrying

Chapter 8 Market Estimates & Forecast, By End use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Construction Companies

- 8.3 Mining Operators

- 8.4 Rental Companies

- 8.5 Government & Municipalities

- 8.6 Industrial Users

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Companies

- 10.1.1 Ashtead Technology (Sunbelt Rentals)

- 10.1.2 Capital Equipment Rental

- 10.1.3 Elliott Equipment Company

- 10.1.4 Herc Rentals

- 10.1.5 Hertz Equipment Rentals

- 10.1.6 JLG

- 10.1.7 John Deere Rental

- 10.1.8 Loxam

- 10.1.9 Ritchie Bros. Auctioneers

- 10.1.10 United Rentals

- 10.2 Regional Companies

- 10.2.1 Allmand Brothers

- 10.2.2 Atlas Rents

- 10.2.3 Bakersfield Rental

- 10.2.4 Maxim Crane Works

- 10.2.5 NESCO Rentals

- 10.2.6 Riwal

- 10.2.7 Stephenson's Rental Services

- 10.2.8 Sunstate Equipment

- 10.2.9 Toromont CAT

- 10.2.10 WesternOne

- 10.3 Emerging Companies

- 10.3.1 Allmand Brothers

- 10.3.2 Capital Equipment Rental

- 10.3.3 Bakersfield Rental

- 10.3.4 Sunstate Equipment