PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959558

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959558

Semiconductor Foundry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

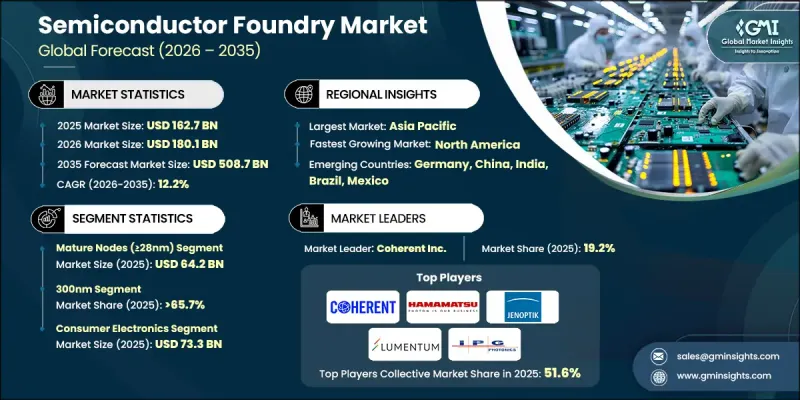

The Global Semiconductor Foundry Market was valued at USD 162.7 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 508.7 billion by 2035.

A semiconductor foundry functions as a specialized manufacturing facility that produces integrated circuits based on designs supplied by fabless companies, using advanced photolithography and precision etching processes on silicon wafers. Pure-play foundry models focus solely on fabrication services, enabling customers to accelerate innovation across artificial intelligence, automotive electronics, high-performance computing, and next-generation connectivity technologies. Rising demand for AI-driven systems, electric vehicles, and 5G infrastructure is strengthening reliance on outsourced chip manufacturing. Foundries play a critical role in delivering advanced nodes, supporting real-time processing, and enabling automation across complex industrial environments. Growing investments in Industry 4.0 and AI infrastructure from both governments and enterprises are further accelerating capacity expansion. As industries require increasingly sophisticated and energy-efficient semiconductors, the semiconductor foundry market continues to expand its technological capabilities and global production footprint to support long-term digital transformation initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $162.7 Billion |

| Forecast Value | $508.7 Billion |

| CAGR | 12.2% |

The mature nodes (>=28nm) segment generated USD 64.2 billion in 2025, representing the largest share of the market. Demand for automotive semiconductors, power devices, industrial IoT sensors, and analog components continues to support strong utilization of mature process technologies. These nodes offer cost efficiency and high-volume manufacturing stability compared to more advanced technologies. At the same time, manufacturers are focusing on scaling sub-2nm processes, advancing chiplet architectures, and enhancing packaging technologies such as CoWoS and 3D integration. Supply chain expansion initiatives and sustainable production strategies are also becoming key priorities.

The 300nm segment accounted for 65.7% share in 2025, maintaining a dominant position within the semiconductor foundry industry. Expansion of 300mm fabrication facilities is increasing production capacity to meet demand for mature-node semiconductors. Facility upgrades and regional diversification programs are being supported by government incentives, including CHIPS Act funding. Constraints in advanced node production are reinforcing demand for analog, power, and legacy chips. Market participants are prioritizing sub-2nm scaling, chiplet integration, diversified supply chains, sustainability programs, and advanced packaging solutions to address AI and high-performance computing requirements while mitigating geopolitical and capital expenditure risks.

North America Semiconductor Foundry Market held a 29.6% share in 2025, driven by substantial CHIPS Act investments and rising demand for AI and high-performance computing semiconductors. Expansion of domestic manufacturing facilities and growing data center capacity are strengthening regional advanced-node output. Increasing automotive semiconductor production and efforts to reduce supply chain dependency on Asia are also contributing to growth. Manufacturers are concentrating on establishing advanced fabrication facilities capable of producing sub-2nm nodes, AI accelerators, and automotive-grade chips, while aligning operations with regulatory compliance and advanced packaging capabilities.

Key companies operating in the Global Semiconductor Foundry Market include ALPHALAS GmbH, Coherent Inc., CrystaLaser, LLC, Daheng New Epoch Technology, Inc., Edgewave, Hamamatsu Photonics K.K., Jenoptik Laser GmbH, Jiangsu Lumispot Technology Co., Ltd., Laserglow Technologies, LASEROPTEK Co., Ltd., Lumentum Operations LLC, LUMIBIRD, Northrop Grumman Corporation, Quanta System S.p.A. and IPG Photonics. Companies in the Semiconductor Foundry Market are reinforcing their competitive position through aggressive capacity expansion, advanced node innovation, and strategic regional investments. Leading players are allocating capital toward sub-2nm research, chiplet ecosystem development, and advanced packaging integration to support AI and high-performance computing applications. Partnerships with fabless design firms and government-backed incentive programs are helping secure long-term production contracts. Firms are also diversifying supply chains to reduce geopolitical risk and enhance operational resilience. Sustainability initiatives, including energy-efficient fabs and reduced water consumption processes, are becoming central to operational strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Equipment type trends

- 2.2.2 Technology node trends

- 2.2.3 Wafer size trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for AI and high-performance computing

- 3.2.1.2 Expansion of electric vehicles and autonomous driving

- 3.2.1.3 Proliferation of 5G and edge computing deployments

- 3.2.1.4 Advancements in advanced process nodes (sub-3nm)

- 3.2.1.5 Growth in fabless semiconductor business model

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditures for leading-edge fabs

- 3.2.2.2 Geopolitical supply chain risks and restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Chiplet architectures and advanced packaging

- 3.2.3.2 Rise of regional foundry diversification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Wafer Processing Equipment

- 5.3 Wafer Handling & Automation Equipment

- 5.4 Metrology & Inspection Equipment

- 5.5 Assembly, Packaging & Test Equipment

Chapter 6 Market Estimates and Forecast, By Technology Node, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Leading-Edge Nodes (≤7nm)

- 6.3 Advanced Nodes (10nm-22nm)

- 6.4 Mature Nodes (≥28nm)

Chapter 7 Market Estimates and Forecast, By Wafer Size, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 200mm

- 7.3 300mm

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Consumer Electronics

- 8.3 Communication

- 8.4 Automotive

- 8.5 Industrial

- 8.6 Others

Chapter 9 Semiconductor foundry Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends, by region

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia-Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 ALPHALAS GmbH

- 10.2 Coherent Inc.

- 10.3 CrystaLaser, LLC

- 10.4 Daheng New Epoch Technology, Inc.

- 10.5 Edgewave

- 10.6 Hamamatsu Photonics K.K.

- 10.7 Jenoptik Laser GmbH

- 10.8 Jiangsu Lumispot Technology Co., Ltd.

- 10.9 Laserglow Technologies

- 10.10 LASEROPTEK Co., Ltd.

- 10.11 Lumentum Operations LLC

- 10.12 LUMIBIRD

- 10.13 Northrop Grumman Corporation

- 10.14 Quanta System S.p.A

- 10.15 IPG Photonics