PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959561

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959561

Automotive Vehicle-to-Everything (V2X) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

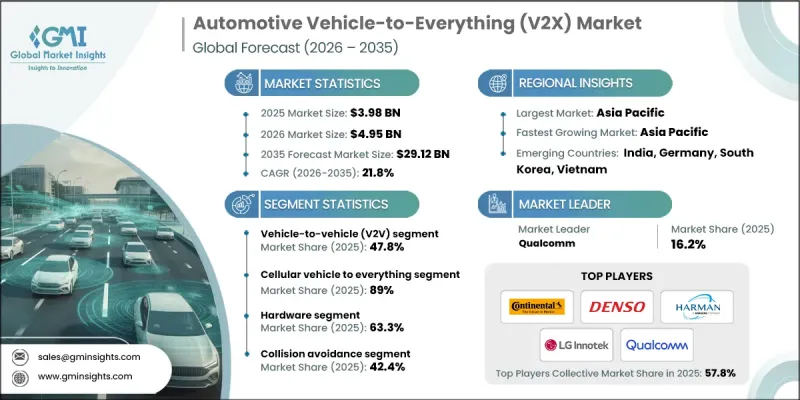

The Global Automotive Vehicle-to-Everything (V2X) Market was valued at USD 3.98 billion in 2025 and is estimated to grow at a CAGR of 21.8% to reach USD 29.12 billion by 2035.

Rising concerns surrounding road safety and the accelerating shift toward vehicle automation are significantly driving the adoption of automotive V2X communication technologies. Governments worldwide are implementing intelligent transportation infrastructure and digital tolling frameworks to enhance traffic flow management and emergency response efficiency. Public authorities across major economies are promoting cooperative intelligent transport deployments along strategic mobility corridors, demonstrating measurable reductions in congestion at connected intersections. The growing penetration of connected and electric vehicles is further strengthening the overall V2X ecosystem. Advancements in ultra-low latency communication standards are improving the commercial viability of V2X solutions, with fifth-generation cellular networks capable of delivering end-to-end latency below 10 milliseconds to enable real-time decision-making for collision avoidance, vehicle platooning, and coordinated autonomous driving in mixed traffic environments. At the same time, cybersecurity and data governance have become critical priorities as connected vehicles generate more than 25 gigabytes of data per hour, prompting OEMs and regulators to implement robust identity authentication, encryption protocols, and secure access control systems to ensure trusted communication across public road networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.98 Billion |

| Forecast Value | $29.12 Billion |

| CAGR | 21.8% |

The vehicle-to-vehicle segment accounted for 47.8% share in 2025 and is expected to grow at a CAGR of 20.8% from 2026 to 2035. V2V communication enables direct data exchange between vehicles, including information related to speed, position, and braking behavior. Safety authorities estimate that a substantial share of multi-vehicle accidents could be prevented through widespread deployment of connected safety technologies, encouraging broader OEM integration across passenger and commercial vehicle platforms. Vehicle-to-infrastructure communication further enhances this ecosystem by enabling interaction between vehicles and roadway systems, supporting traffic optimization and coordinated mobility management.

The cellular vehicle-to-everything segment held 89% share in 2025 and is forecast to grow at a CAGR of 22.7% through 2035. Cellular V2X architecture delivers an integrated communication framework linking vehicles, infrastructure, network operators, and cloud platforms. This connectivity supports continuous software updates, remote diagnostics, and progressive vehicle automation capabilities. By unifying vehicles, pedestrians, roadside systems, and backend networks within a single communication ecosystem, cellular V2X enhances interoperability across private vehicles, commercial fleets, and public transportation systems, accelerating scalable deployment.

China Automotive Vehicle-to-Everything (V2X) Market held 63.8% share, generating USD 1.2 billion in 2025. Strong national coordination, large-scale intelligent transportation initiatives, and integrated smart city strategies have positioned China as a key environment for V2X deployment. Domestic automakers are embedding V2X functionality across vehicle platforms while collaborating with telecom operators and digital service providers to standardize protocols and expand nationwide connectivity across urban and highway infrastructure.

Key companies operating in the Global Automotive Vehicle-to-Everything (V2X) Market include Qualcomm, NXP, Continental, Bosch, Denso, Harman, Nokia, LG Innotek, and AT&T. Companies in the automotive vehicle-to-everything market are strengthening their competitive position through strategic telecom partnerships, advanced chipset development, and software-driven innovation. Leading players are investing heavily in 5G and next-generation connectivity solutions to enhance latency performance and scalability. Collaboration with automotive OEMs enables early integration of V2X modules into new vehicle platforms. Firms are also prioritizing cybersecurity frameworks, secure credential management systems, and over-the-air update capabilities to meet evolving regulatory standards.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Component

- 2.2.5 Application

- 2.2.6 Deployment

- 2.2.7 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising road safety regulations

- 3.2.1.2 Growth of connected and autonomous vehicles

- 3.2.1.3 Expansion of smart city programs

- 3.2.1.4 Deployment of fifth generation networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure deployment cost

- 3.2.2.2 Interoperability and standardization issues

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with autonomous driving systems

- 3.2.3.2 Expansion of vehicle to infrastructure projects

- 3.2.3.3 Growth in electric and connected vehicle fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States connected vehicle and intelligent transportation regulations

- 3.4.1.2 Federal communications and spectrum allocation guidelines

- 3.4.1.3 Vehicle safety and connected mobility standards

- 3.4.1.4 Canada cooperative intelligent transport system regulations

- 3.4.2 Europe

- 3.4.2.1 European Union cooperative intelligent transport system framework

- 3.4.2.2 ETSI and CEN communication standards for V2X

- 3.4.2.3 Country level connected vehicle compliance requirements

- 3.4.2.4 Data protection and cybersecurity rules for connected mobility

- 3.4.3 Asia Pacific

- 3.4.3.1 China intelligent connected vehicle regulations

- 3.4.3.2 India connected transport and automotive communication standards

- 3.4.3.3 Japan cooperative driving and vehicle communication guidelines

- 3.4.3.4 South Korea smart mobility and V2X compliance

- 3.4.3.5 ASEAN regional connected transport frameworks

- 3.4.4 Latin America

- 3.4.4.1 Brazil intelligent transport and connected vehicle regulations

- 3.4.4.2 Argentina automotive communication compliance

- 3.4.4.3 Mexico connected mobility and transport digitization policies

- 3.4.4.4 Regional connected vehicle regulatory frameworks

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE smart mobility and connected vehicle regulations

- 3.4.5.2 Saudi Arabia intelligent transport system compliance

- 3.4.5.3 South Africa connected vehicle and road safety standards

- 3.4.5.4 Regional smart transport regulatory frameworks

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 OEM and infrastructure investment analysis

- 3.12.1 Automaker investment priorities

- 3.12.2 Public sector and municipal funding trends

- 3.12.3 Private sector and telecom investments

- 3.13 Deployment economics and ROI assessment

- 3.13.1 Cost benefit analysis for OEMs

- 3.13.2 Infrastructure ROI for public authorities

- 3.13.3 Payback timelines by application

- 3.14 Spectrum allocation and communication reliability analysis

- 3.14.1 Licensed vs unlicensed spectrum considerations

- 3.14.2 Network congestion and performance risks

- 3.14.3 Cross border spectrum harmonization challenges

- 3.15 Monetization and business model analysis

- 3.15.1 OEM led monetization models

- 3.15.2 Subscription and service based revenue streams

- 3.15.3 Data driven and platform based monetization

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Vehicle-to-Infrastructure (V2I)

- 5.3 Vehicle-to-Vehicle (V2V)

- 5.4 Vehicle-to-Pedestrian (V2P)

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Dedicated Short-Range Communications (DSRC)

- 6.3 Cellular Vehicle-to-Everything (C-V2X)

Chapter 7 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Hardware

- 7.2.1 Tracking and positioning

- 7.2.1.1 GNSS/GPS modules (standard)

- 7.2.1.2 High-precision GNSS (DGPS/RTK)

- 7.2.2 Safety and perception

- 7.2.2.1 Radar sensors

- 7.2.2.2 Cameras

- 7.2.2.3 LiDAR

- 7.2.2.4 Ultrasonic sensors

- 7.2.2.5 Thermal and time-of-flight sensors

- 7.2.3 Control and processing

- 7.2.3.1 V2X electronic control units (V2X ECU)

- 7.2.3.2 ADAS ECUs

- 7.2.3.3 Domain controllers

- 7.2.4 Communication and connectivity

- 7.2.4.1 C-V2X modems

- 7.2.4.2 DSRC radios

- 7.2.4.3 5G NR-V2X modules

- 7.2.4.4 On-board units (OBU)

- 7.2.4.5 Telematics control units (TCU)

- 7.2.4.6 V2X antennas

- 7.2.5 Human-machine interface

- 7.2.5.1 V2X displays

- 7.2.5.2 Head-up displays (HUD)

- 7.2.5.3 Instrument cluster alerts

- 7.2.5.4 Audio and haptic alert modules

- 7.2.6 Others

- 7.2.1 Tracking and positioning

- 7.3 Software

- 7.4 Services

- 7.4.1 Consulting & Integration Services

- 7.4.2 Cybersecurity & Data Protection Services

- 7.4.3 Traffic Management & Road Safety Services

- 7.4.4 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Fleet Management

- 8.3 Autonomous Driving

- 8.4 Collision Avoidance

- 8.5 Intelligent Traffic Systems

- 8.6 Parking Management Systems

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Deployment, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Cloud-based

- 9.3 On-premises

Chapter 10 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 Passenger vehicle

- 10.2.1 Sedan

- 10.2.2 SUV

- 10.2.3 Hatchback

- 10.3 Commercial vehicle

- 10.3.1 Light Commercial Vehicle (LCV)

- 10.3.2 Medium Commercial Vehicle (MCV)

- 10.3.3 Heavy Commercial Vehicle (HCV)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Norway

- 11.3.8 Netherlands

- 11.3.9 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 AT&T

- 12.1.2 Bosch

- 12.1.3 Continental

- 12.1.4 Denso

- 12.1.5 Harman

- 12.1.6 LG Innotek

- 12.1.7 Nokia

- 12.1.8 NXP

- 12.1.9 Qualcomm

- 12.2 Regional Players

- 12.2.1 Fujitsu

- 12.2.2 Huawei Technologies

- 12.2.3 Hyundai Mobis

- 12.2.4 NEC Corporation

- 12.2.5 Panasonic Automotive Systems

- 12.2.6 Renesas Electronics

- 12.2.7 Toyota Connected

- 12.2.8 ZTE Corporation

- 12.3 Emerging Players and Disruptors

- 12.3.1 Autotalks

- 12.3.2 Cohda Wireless

- 12.3.3 Commsignia

- 12.3.4 Danlaw

- 12.3.5 Kapsch TrafficCom