PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959562

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959562

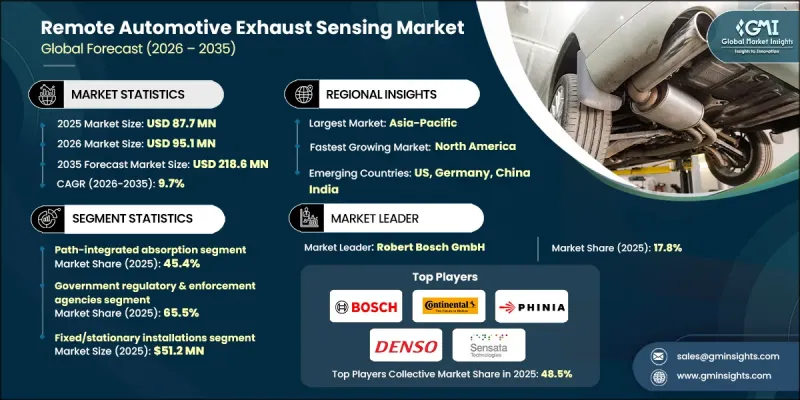

Remote Automotive Exhaust Sensing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Remote Automotive Exhaust Sensing Market was valued at USD 87.7 million in 2025 and is estimated to grow at a CAGR of 9.7% to reach USD 218.6 million by 2035.

The market is expanding due to stringent emission standards in major automotive regions worldwide, which are driving the adoption of real-world vehicle emissions monitoring solutions. Governments are heavily investing in remote exhaust sensing infrastructure, particularly in urban centers and high-traffic areas, to manage air quality. Unlike traditional laboratory testing or random inspections, these technologies capture real-time emissions data from vehicles, enabling authorities to address pollution more effectively. The market is further supported by public funding for urban air quality initiatives and integration of exhaust sensors into smart city transportation networks. Advances in sensing accuracy, data analytics, and automated reporting have increased trust among environmental and transport authorities, accelerating widespread deployment. Rising concerns over urban air pollution and compliance with evolving emission regulations are fueling the steady adoption of remote sensing systems globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $87.7 Million |

| Forecast Value | $218.6 Million |

| CAGR | 9.7% |

The path-integrated absorption segment held 45.4% share in 2025. These sensors are preferred for their ability to deliver highly accurate, real-time measurements of nitrogen oxides (NOx), carbon monoxide (CO), and particulate matter over extended distances. They enable continuous monitoring on busy roadways and can be integrated with automated roadside stations, supporting compliance with emission regulations and fleet management programs. Their efficiency in providing reliable data has made them a cornerstone technology for urban and regulatory applications.

The vehicle manufacturers segment is projected to grow at a CAGR of 9.6% during 2026 to 2035. Automotive OEMs and commercial fleet operators are increasingly deploying remote exhaust sensors to evaluate real-world emissions performance, optimize engine calibration, and comply with local and international emission standards. Heightened regulatory scrutiny and corporate sustainability initiatives are encouraging manufacturers to adopt on-road sensing solutions, especially across Europe, North America, and East Asia, where emissions performance is under continuous evaluation.

North America Remote Automotive Exhaust Sensing Market accounted for 18.9% share in 2025. Market growth in the region is driven by strict EPA emission standards, growing urban air quality programs, and rising demand for real-time emissions monitoring. Deployment of roadside sensing units is expanding in cities with high traffic density, enabling authorities and private fleets to monitor NOx and particulate matter emissions continuously. Investments in IoT-enabled sensors and AI-driven data analytics are enhancing the capability to track emissions in real time, allowing for prompt interventions and regulatory compliance.

Key players in the Global Remote Automotive Exhaust Sensing Market include Amphenol Advanced Sensors, AVL List GmbH, Continental AG, Denso Corporation, Hager Environmental & Atmospheric Technologies (HEAT), HELLA GmbH & Co. KGaA, Korea Environment Corporation (K-eco), Niterra India PVT. LTD., Opus Group AB, PHINIA Inc., Robert Bosch GmbH, Sensata Technologies, Inc., and Valeo SA. Companies in the Remote Automotive Exhaust Sensing Market are adopting multiple strategies to strengthen their market position. They are investing in advanced sensor technologies to improve accuracy, range, and data processing speed. Strategic collaborations with government agencies, transport authorities, and fleet operators are enabling early adoption and integration into smart city programs. Firms are expanding their global presence through partnerships, joint ventures, and localized manufacturing to meet regional regulatory requirements. Incorporation of AI, machine learning, and cloud-based analytics enhances predictive maintenance, emissions reporting, and fleet optimization services.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Sensing modality trends

- 2.2.2 Target pollutant trends

- 2.2.3 Offering trends

- 2.2.4 Deployment configuration trends

- 2.2.5 End user trends

- 2.2.6 Vehicle type trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stricter vehicle emission rules by governments globally

- 3.2.1.2 Government investment in roadside remote sensing programs

- 3.2.1.3 Rising urban air quality compliance monitoring needs

- 3.2.1.4 Need for fast on-road vehicle emission checks

- 3.2.1.5 Advances in infrared spectroscopy and data analytics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Accuracy variability under weather and traffic conditions

- 3.2.2.2 High installation and system maintenance costs

- 3.2.3 Market opportunities

- 3.2.3.1 Support for smart city air monitoring programs

- 3.2.3.2 Use by fleet operators for emission tracking

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Sensing Modality, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Path-integrated absorption

- 5.3 Laser ranging / active laser

- 5.4 Particle-phase optical

- 5.5 Imaging spectroscopy

Chapter 6 Market Estimates and Forecast, By Target Pollutant, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Gas-Phase

- 6.2.1 NOx (NO, NO2)

- 6.2.2 CO

- 6.2.3 CO2

- 6.2.4 HC/VOC

- 6.2.5 NH3

- 6.2.6 SO2

- 6.3 Other regulated/target gases (HCHO, CH4)

Chapter 7 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software & analytics

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By Deployment Configuration, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Fixed/stationary installations

- 8.3 Mobile enforcement platforms

- 8.4 Portable handheld/field devices

- 8.5 Networked sensor arrays

Chapter 9 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Light-duty vehicles

- 9.3 Heavy-duty vehicle

- 9.4 Two-wheelers

- 9.5 Non-road engines & off-highway equipment vehicle

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 Government regulatory & enforcement agencies

- 10.3 Vehicle manufacturers

- 10.4 Third-party inspection & certification bodies

- 10.5 Academic & research institutions

- 10.6 Commercial fleet owners

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Robert Bosch GmbH

- 12.1.2 Continental AG

- 12.1.3 Denso Corporation

- 12.1.4 Sensata Technologies, Inc.

- 12.1.5 Valeo SA

- 12.1.6 HELLA GmbH & Co. KGaA

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Amphenol Advanced Sensors

- 12.2.1.2 Opus Group AB

- 12.2.2 Asia Pacific

- 12.2.2.1 Niterra India PVT. LTD.

- 12.2.2.2 Korea Environment Corporation (K-eco)

- 12.2.3 Europe

- 12.2.3.1 AVL List GmbH

- 12.2.3.2 PHINIA Inc.

- 12.2.3.3 Hager Environmental & Atmospheric Technologies (HEAT)

- 12.2.1 North America