PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959564

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959564

Automotive Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

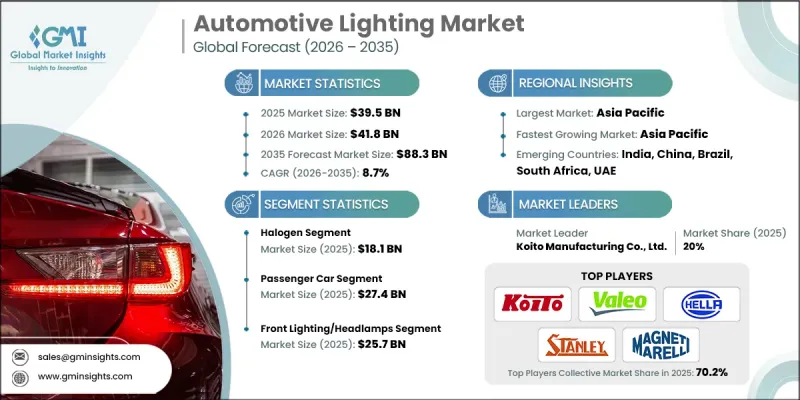

The Global Automotive Lighting Market was valued at USD 39.5 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 88.3 billion by 2035.

The industry's growth is driven by increasing adoption of LED and adaptive lighting systems, stricter vehicle safety and emissions regulations, rising popularity of electric and autonomous vehicles, consumer demand for energy-efficient and stylish lighting, and expansion of automotive manufacturing in emerging markets. Regulatory compliance with global safety standards and energy-efficiency mandates is encouraging the integration of advanced lighting technologies, enhancing driver visibility, reducing glare, and contributing to overall vehicle efficiency. The shift toward electrification and autonomous driving has further amplified the use of sophisticated lighting solutions as critical components of safety, energy management, and aesthetic design in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.5 Billion |

| Forecast Value | $88.3 Billion |

| CAGR | 8.7% |

The halogen segment accounted for USD 18.1 billion in 2025, maintaining strong demand due to its low production costs, straightforward manufacturing processes, and broad compatibility with existing vehicle electrical systems. Halogen lighting continues to be widely used in entry-level and mid-segment vehicles where premium lighting technologies like LEDs or adaptive systems are not yet standard, offering a cost-effective solution without compromising basic safety requirements. Its relevance extends to aftermarket replacements, supported by the growing global vehicle parc, which ensures a consistent demand for retrofitting older vehicles. Additionally, halogen bulbs provide reliability under diverse driving conditions and require minimal maintenance, making them a preferred choice for fleet operators, commercial vehicles, and markets in developing regions where cost efficiency remains a priority.

The passenger car segment reached USD 27.4 billion in 2025, driven by strong demand for advanced lighting features such as adaptive, LED, and matrix systems, which enhance both safety and visual appeal. These technologies provide dynamic beam adjustments, improved nighttime visibility, and glare reduction for oncoming traffic, contributing to higher driving safety ratings. Furthermore, passenger car buyers increasingly consider lighting aesthetics as part of vehicle design and brand identity, pushing automakers to differentiate their models with signature lighting patterns. Regulatory frameworks in major markets, including mandatory daytime running lights, adaptive headlamps, and energy-efficiency standards, further accelerate adoption.

North America Automotive Lighting Market held an 18.5% share in 2025, driven by rising vehicle electrification, widespread adoption of LED and smart adaptive lighting systems, and strict compliance with federal lighting and safety standards. The region's advanced automotive manufacturing ecosystem, strong regulatory enforcement, and consumer preference for high-performance, energy-efficient lighting solutions underpin market expansion. Advanced front lighting systems, matrix LED, and laser-based technologies are becoming standard in new passenger and commercial vehicle models, supporting enhanced visibility, reduced power consumption, and improved driving safety. Additionally, North American manufacturers are investing heavily in R&D for intelligent and connected lighting solutions, integrating sensors and IoT technologies to enable adaptive, autonomous vehicle-ready lighting that aligns with the growing focus on automated driving and smart mobility infrastructure.

Prominent players in the Global Automotive Lighting Market include Continental AG, General Electric Company, HELLA GmbH & Co. KGaA, Hyundai Mobis Co., Ltd, Ichikoh Industries, Ltd., Koito Manufacturing Co., Koninklijke Philips N.V., Lumax Industries, Magnetti Marelli S.p.A, Namyung Lighting, OSRAM GmbH, Robert Bosch GmbH, Samsung Electronics Co., Ltd., Seoul Semiconductor, Stanley Electric Co., Ltd., Tungsram Group, Valeo Visibility Systems, Varroc Lighting Solutions, Zizala Lichtsysteme GmbH, and ZKW Lichtsysteme GmbH. Companies in the Automotive Lighting Market are focusing on strategic initiatives such as expanding R&D for LED and adaptive systems, forming partnerships with OEMs to integrate intelligent lighting technologies, optimizing supply chains for global distribution, investing in sustainable energy-efficient solutions, launching aftermarket programs to capture legacy vehicle demand, and adopting digital and IoT-enabled lighting innovations. Emphasis on design differentiation, regulatory compliance, and modular, scalable solutions helps manufacturers strengthen market presence, improve brand recognition, and secure long-term contracts with automotive producers worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Vehicle type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for LED and adaptive lighting systems

- 3.2.1.2 Stringent vehicle safety and emission regulations

- 3.2.1.3 Increasing adoption of electric and autonomous vehicles

- 3.2.1.4 Growing consumer preference for stylish and energy-efficient lighting

- 3.2.1.5 Expansion of automotive production in emerging markets

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial costs of advanced lighting systems

- 3.2.2.2 Complexity in integration with vehicle electronics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 LED

- 5.3 Halogen

- 5.4 Xenon

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Two wheelers

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Front lighting/Headlamps

- 7.3 Rear lighting

- 7.4 Interior lighting

- 7.5 Side lighting

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 General Electric Company

- 9.1.2 Samsung Electronics Co., Ltd.

- 9.1.3 Koninklijke Philips N.V.

- 9.1.4 Robert Bosch Gmbh

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Continental AG

- 9.2.1.2 Lumax Industries

- 9.2.1.3 Varroc Lighting Solutions

- 9.2.2 Europe

- 9.2.2.1 HELLA GmbH & Co. KGaA

- 9.2.2.2 OSRAM Gmbh

- 9.2.2.3 Tungsram Group

- 9.2.2.4 Zkw Lichtsysteme Gmbh

- 9.2.2.5 Zizala Lichtsysteme Gmbh

- 9.2.2.6 Magnetti Marelli S.p.A

- 9.2.2.7 Valeo Visibility Systems

- 9.2.3 Asia Pacific

- 9.2.3.1 Hyundai Mobis Co., Ltd

- 9.2.3.2 Koito Manufacturing Co.

- 9.2.3.3 Ichikoh Industries, Ltd.

- 9.2.3.4 Seoul Semiconductor

- 9.2.3.5 Stanley Electric Co.Ltd

- 9.2.1 North America

- 9.3 Niche Player/Disruptor

- 9.3.1 Namyung Lighting