PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959578

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959578

Single Board Computer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

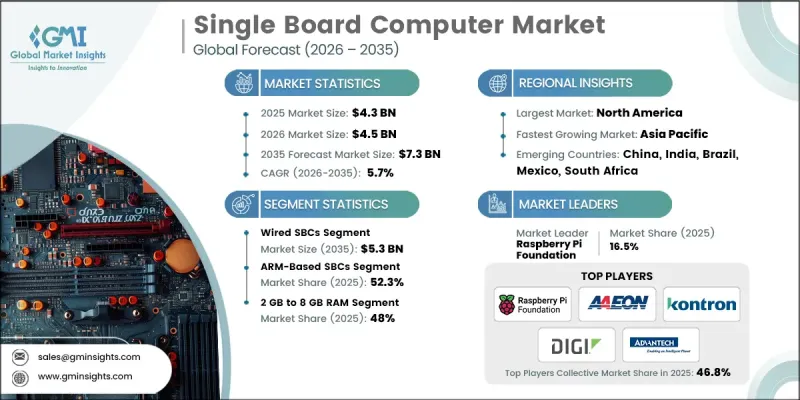

The Global Single Board Computer Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 7.3 billion by 2035.

The market is witnessing rapid expansion due to the rising adoption of IoT devices across industries. As businesses increasingly integrate IoT into operations, the demand for compact, efficient, and versatile computing solutions such as SBCs is accelerating. Educational and DIY projects are further supporting growth, with institutions using SBCs to train students in programming, electronics, and other tech skills. SBCs are shaping a new generation of tech-savvy individuals while creating long-term market opportunities. Additionally, the use of SBCs in AI, machine vision, and edge computing is fueling demand, as these applications require low-latency, high-performance computing capable of real-time data processing. As robotics, autonomous systems, security, and industrial automation expand, SBCs are becoming a critical backbone of modern technological infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 5.7% |

The wired SBC segment is projected to reach USD 5.3 billion by 2035. Wired SBCs are increasingly preferred in industrial and enterprise environments because they deliver high-speed, stable connectivity and ensure uninterrupted data transmission for mission-critical applications. These boards are essential for manufacturing automation, real-time monitoring systems, and industrial IoT networks, where even minimal downtime can disrupt operations or compromise safety. Their reliability under continuous use, resistance to interference, and compatibility with existing wired networks make them a cornerstone for sectors that demand precision, low latency, and consistent performance across complex systems.

The ARM-based SBC segment held a 52.3% share in 2025, gaining traction due to its power-efficient architecture and adaptability for AI, embedded computing, and edge processing. These boards are especially valued for fanless designs and compact footprints, allowing deployment in space-constrained environments without sacrificing performance. Their low power consumption, combined with high computational efficiency, supports long-term operation and reduces energy costs, making them ideal for robotics, mobile devices, and automated industrial equipment.

North America Single Board Computer Market contributed 36.7% share in 2025. The region's strong adoption of industrial automation, IoT integration, and edge computing solutions has propelled SBC demand. Enterprises and government agencies rely on these compact computing systems for real-time data acquisition, process monitoring, and seamless integration with existing industrial networks. Advanced technology infrastructure, robust supply chains, and ongoing investments in smart manufacturing and connected systems have reinforced North America's leadership in the Single Board Computer Market, positioning it as a hub for innovation and large-scale deployment.

Prominent players in the Global Single Board Computer Market include Advantech Co., Ltd., DFI Inc. (Diamond Flower Inc.), AAEON Technology Inc., Abaco Systems, Inc., ADLINK Technology Inc., ASUSTeK Computer Inc., Axiomtek Co., Ltd., Congatec AG, Digi International Inc., IEI Integration Corp., Eurotech S.p.A., Kontron AG, Radisys Corporation, Raspberry Pi Foundation, and Texas Instruments Incorporated. Key strategies adopted by companies in the Single Board Computer Market include expanding product portfolios to cover diverse applications from AI and industrial automation to education and embedded systems. Firms focus on enhancing processing power while maintaining energy efficiency and compact form factors. Companies invest heavily in R&D to develop specialized SBCs for edge computing, robotics, and AI workloads. Strategic partnerships, collaborations, and acquisitions are used to enter new markets and access innovative technologies. Manufacturers also emphasize reliability, high-speed connectivity, and long-term technical support to strengthen customer loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Processor architecture trends

- 2.2.2 Memory configuration trends

- 2.2.3 Connectivity interface trends

- 2.2.4 End-use application trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid adoption of IoT and edge computing applications

- 3.2.1.2 Widespread use of SBCs in educational and DIY projects

- 3.2.1.3 Rising utilization in AI and machine vision systems

- 3.2.1.4 Increasing investments in defense and aerospace programs

- 3.2.1.5 Expansion of educational and maker communities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions and component shortages

- 3.2.2.2 Competition from alternative computing technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in autonomous vehicles and drones

- 3.2.3.2 Opportunities in energy management and smart grids

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Processor Architecture, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 ARM-Based SBCs

- 5.3 x86 / x64-Based SBCs

- 5.4 RISC-V-Based SBCs

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Memory Configuration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 2 GB RAM

- 6.3 2 GB to 8 GB RAM

- 6.4 8 GB to 16 GB RAM

- 6.5 16 GB to 32 GB RAM

Chapter 7 Market Estimates and Forecast, By Connectivity Interface, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Wired SBCs

- 7.2.1 Industrial fieldbus protocols

- 7.2.2 Standard ethernet

- 7.2.3 Usb / Serial

- 7.2.4 Others

- 7.3 Wireless SBCs

- 7.3.1 Wi-Fi

- 7.3.2 Cellular

- 7.3.3 Others

Chapter 8 Market Estimates and Forecast, By End-use Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Automotive

- 8.2.1 In-vehicle infotainment & telematics

- 8.2.2 ADAS & autonomous driving systems

- 8.2.3 Others

- 8.3 Food & beverage

- 8.3.1 Process automation & control

- 8.3.2 Quality monitoring & safety systems

- 8.3.3 Others

- 8.4 Medical & healthcare

- 8.4.1 Medical devices & diagnostics

- 8.4.2 Telemedicine & remote health monitoring

- 8.4.3 Others

- 8.5 Defense, aerospace & public safety

- 8.6 Energy & utilities

- 8.7 Chemical & pharmaceutical manufacturing

- 8.8 Telecommunications & networking

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Advantech Co., Ltd.

- 10.1.2 Kontron AG

- 10.1.3 Digi International Inc.

- 10.1.4 Texas Instruments Incorporated

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Abaco Systems, Inc.

- 10.2.1.2 Radisys Corporation

- 10.2.1.3 IEI Integration Corp.

- 10.2.2 Europe

- 10.2.2.1 Congatec AG

- 10.2.2.2 Eurotech S.p.A.

- 10.2.2.3 DFI Inc. (Diamond Flower Inc.)

- 10.2.3 APAC

- 10.2.3.1 AAEON Technology Inc.

- 10.2.3.2 ADLINK Technology Inc.

- 10.2.3.3 ASUSTeK Computer Inc.

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Raspberry Pi Foundation

- 10.3.2 Axiomtek Co., Ltd.