PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959579

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959579

Security Scanning Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

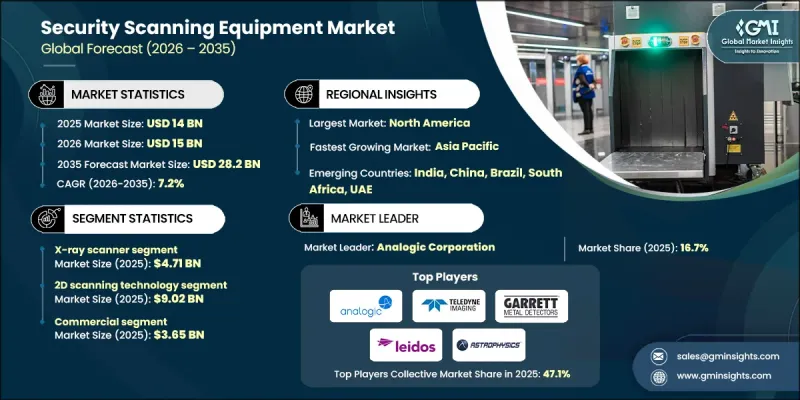

The Global Security Scanning Equipment Market was valued at USD 14 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 28.2 billion by 2035.

Market expansion is driven by rising global security risks, increasingly strict regulatory frameworks, continuous technological progress in detection capabilities, and growing investment in large-scale infrastructure. Governments and public authorities are strengthening security systems to address evolving threat patterns and increasingly complex risk environments. This has accelerated the adoption of advanced scanning solutions designed to improve detection accuracy, reduce operational vulnerabilities, and support proactive risk mitigation. Regulatory mandates continue to shape procurement decisions by defining performance benchmarks, deployment standards, and compliance timelines. The market is also benefiting from the rapid integration of artificial intelligence and automation, which enhances image analysis, reduces human error, and improves throughput. Expansion of transportation networks and public infrastructure further supports demand, as secure access control and screening are becoming essential components of modern facility design. These combined factors are positioning security scanning equipment as a critical investment across both public and private sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14 Billion |

| Forecast Value | $28.2 Billion |

| CAGR | 7.2% |

The X-ray scanning systems segment generated USD 4.71 billion in 2025. Demand for this segment remains strong due to the ongoing modernization of screening checkpoints and the replacement of older systems with digital platforms that offer improved resolution, faster processing, and enhanced detection reliability. Continued system upgrades are sustaining long-term procurement activity across regulated environments.

The 2D scanning technology segment reached USD 9.02 billion in 2025. This segment continues to see widespread adoption due to its cost efficiency, operational simplicity, and compatibility with existing security frameworks. These systems remain favored in high-volume screening environments where reliability and throughput are prioritized over advanced analytical complexity.

North America Security Scanning Equipment Market accounted for 40.6% share in 2025. The region benefits from mature infrastructure, high public safety standards, and early adoption of next-generation screening technologies. Continued investments in automated and intelligent scanning solutions are supporting sustained market leadership.

Key companies operating in the Global Security Scanning Equipment Market include Smiths Group PLC, OSI Systems, Inc., Thales Group, Nuctech, Garrett Metal Detectors, Analogic Corporation, Leidos Holdings, Inc., CEIA S.p.A., Bruker Corporation, NEC Corporation, Teledyne Digital Imaging, Gilardoni S.p.A., Autoclear LLC, Astrophysics Inc., Vanderlande Industries, LINEV Systems, Metrasens, Scanna MSC Ltd., Westminster Group Plc, and OSI Systems, Inc. Companies in the security scanning equipment market are strengthening their competitive positions through continuous investment in advanced detection technologies and software-driven innovation. Many players are integrating artificial intelligence, automation, and data analytics to improve threat recognition and operational efficiency. Strategic partnerships with government bodies and infrastructure operators are helping secure long-term contracts. Firms are also focusing on modular system designs that allow scalability and future upgrades. Expanding global service networks and offering lifecycle support solutions are key priorities to enhance customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Technology trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising security threats

- 3.2.1.2 Stringent government regulations

- 3.2.1.3 Technological advancements in detection systems

- 3.2.1.4 Expansion of transportation and infrastructure

- 3.2.1.5 Increasing adoption of AI and automation

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High equipment costs

- 3.2.2.2 Integration and interoperability issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 X-ray Scanners

- 5.3 Magnetic Resonance Imaging (MRI) Scanners

- 5.4 Computed Tomography (CT) Scanners

- 5.5 Ultrasound Scanners

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 2D Scanning Technology

- 6.3 3D Scanning Technology

- 6.4 4D Scanning Technology

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million & Units)

- 7.1 Key Trends

- 7.2 Commercial

- 7.3 Industrial

- 7.4 Public Infrastructure

- 7.5 Military and Defense & Correctional Facility

- 7.6 Institutional

- 7.7 Transportation and aviation

- 7.8 Healthcare

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Smiths Group PLC

- 9.1.2 OSI Systems, Inc.

- 9.1.3 Thales Group

- 9.1.4 Leidos Holdings, Inc.

- 9.1.5 NEC Corporation

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Analogic Corporation

- 9.2.1.2 Astrophysics Inc.

- 9.2.1.3 Autoclear LLC

- 9.2.1.4 Bruker Corporation

- 9.2.1.5 Teledyne Digital Imaging

- 9.2.2 Europe

- 9.2.2.1 CEIA S.p.A.

- 9.2.2.2 Gilardoni S.p.A.

- 9.2.2.3 Metrasens

- 9.2.2.4 Scanna MSC Ltd.

- 9.2.2.5 Westminster Group Plc

- 9.2.3 Asia Pacific

- 9.2.3.1 Nuctech

- 9.2.3.2 Vanderlande Industries

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Garrett Metal Detectors

- 9.3.2 LINEV Systems