PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959583

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959583

Industrial PC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

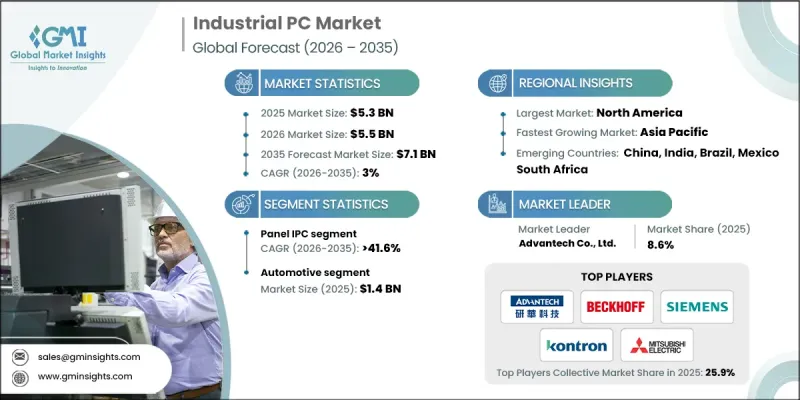

The Global Industrial PC Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 3% to reach USD 7.1 billion by 2035.

Market expansion is supported by accelerating demand for industrial automation, smart manufacturing infrastructure, and Industrial Internet of Things (IIoT) frameworks. As industries move toward digital transformation, organizations are investing in high-performance and durable industrial computing platforms capable of operating in complex and demanding environments. The integration of intelligent production systems and cloud-enabled data architectures is further strengthening the requirement for reliable computing hardware that ensures seamless connectivity, operational visibility, and process efficiency. Industrial PCs play a critical role in supporting real-time analytics, system interoperability, and continuous production monitoring. Growing emphasis on improving productivity, minimizing downtime, and enhancing data-driven decision-making continues to reinforce global demand for robust industrial computing systems across multiple verticals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 3% |

Rising deployment of industrial PCs across manufacturing, energy, and logistics environments is creating new growth avenues for advanced control and computing solutions. Organizations increasingly require dependable platforms capable of handling continuous workloads, managing automated equipment, and processing real-time operational data. Within IIoT ecosystems, industrial PCs function as centralized nodes that gather, process, and transmit information from connected sensors and industrial devices. Expanding adoption of predictive analytics, asset monitoring, and process optimization strategies is intensifying the need for rugged, scalable, and high-performance industrial computing systems. The integration of artificial intelligence and edge computing capabilities into industrial hardware allows companies to interpret large volumes of live data and execute automated responses efficiently. This evolution in industrial computing architecture enhances system responsiveness, improves operational accuracy, and supports streamlined automation across diverse industrial settings.

The Panel IPC segment accounted for 41.6% share in 2025. Growth in this segment is driven by increasing demand for integrated touchscreen systems that combine display functionality with embedded computing power. These all-in-one solutions simplify installation, reduce space requirements, and enhance user interaction with industrial equipment. By enabling direct monitoring and control of processes, panel-based industrial PCs contribute to improved workflow management and operational transparency. Their compact structure and intuitive interfaces support productivity improvements across multiple industrial applications, reinforcing their strong market presence and sustained adoption.

The automotive segment generated USD 1.4 billion in 2025, making it the largest end-use category within the Industrial PC market. Growth in this segment is supported by expanding requirements for advanced computing systems capable of handling real-time data processing and automated production workflows. Industrial PCs are widely utilized in manufacturing environments to enhance quality control, streamline production lines, and improve supply chain coordination. As mobility solutions evolve and vehicle production processes become increasingly technology-driven, manufacturers are prioritizing computing platforms designed for high reliability, rapid data handling, and seamless automation integration. Emphasis on intelligent production systems and connected technologies continues to stimulate demand for specialized industrial computing hardware tailored to automotive applications.

North America Industrial PC Market held a 25.9% share in 2025, establishing itself as a key regional contributor. Market growth in the region is supported by rapid implementation of automation technologies and digital manufacturing strategies. Increased focus on advanced production systems and connected industrial frameworks has accelerated demand for computing platforms capable of delivering real-time processing and secure connectivity. Companies operating in this region are emphasizing the development of industrial PCs equipped with automation-ready features, robust processing capabilities, and integrated communication technologies to support evolving industrial requirements.

Major companies participating in the Global Industrial PC Market include Siemens AG, Advantech Co., Ltd., Schneider Electric, Beckhoff Automation, Mitsubishi Electric Corporation, Honeywell International Inc., Kontron, IEI Integration Corp., American Portwell Technology, Inc., Nexcom International, DFI, B&R Automation, Avalue Technology, InoNet Computer GmbH, Elpro Technologies, Hibertek International Limited, Panelmate, and Quinta. Companies in the Industrial PC Market are strengthening their competitive position through continuous product innovation, strategic partnerships, and expansion into high-growth industrial sectors. Manufacturers are investing in research and development to enhance processing power, durability, and connectivity features tailored to evolving automation requirements. Many firms are integrating AI-ready architectures and edge computing capabilities to differentiate their offerings and address advanced industrial applications. Expanding distribution networks and collaborating with system integrators enable broader market reach and improved customer engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Processor Architecture trends

- 2.2.3 Application trends

- 2.2.4 End-Use trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of industrial automation and smart manufacturing systems.

- 3.2.1.2 Growth of Industrial Internet of Things (IIoT) deployments across sectors.

- 3.2.1.3 Increasing demand for real-time data processing and predictive analytics.

- 3.2.1.4 Expansion of edge computing and AI integration in industrial environments.

- 3.2.1.5 Rising investments in robust, rugged computing solutions for harsh conditions.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs of industrial PC solutions and integration.

- 3.2.2.2 Complexity of deployment for legacy system upgrades.

- 3.2.3 Market opportunities

- 3.2.3.1 Cloud-enabled industrial PC services and remote monitoring offerings.

- 3.2.3.2 Rising demand from emerging markets undergoing industrial modernization.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Industrial PC Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends,

- 5.2 Panel IPC

- 5.2.1 Resistive touch panel

- 5.2.2 Capacitive touch panel

- 5.3 Rack mount IPC

- 5.4 Embedded IPC

- 5.4.1 Fanless embedded PCs

- 5.4.2 Compact industrial box PCs

- 5.5 DIN rail IPC

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Processor Architecture, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 x86 (Intel/AMD)

- 6.3 ARM based

- 6.4 RISC / Other Architectures

Chapter 7 Industrial PC Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Process automation

- 7.3 Machine / factory automation

- 7.4 Human machine interface (HMI)

- 7.5 Data acquisition & monitoring

- 7.6 Edge computing / AI analytics

- 7.7 Others

Chapter 8 Industrial PC Market Estimates & Forecast, By End-Use, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Chemicals

- 8.4 Semiconductor & electronics

- 8.5 Aerospace & defense

- 8.6 Energy & power

- 8.7 Healthcare

- 8.8 Others

Chapter 9 Industrial PC Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends, by region

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia-Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Advantech Co., Ltd.

- 10.2 American Portwell Technology, Inc.

- 10.3 Avalue Technology

- 10.4 B&R Automation

- 10.5 Beckhoff Automation

- 10.6 DFI

- 10.7 Elpro Technologies

- 10.8 Hibertek International Limited

- 10.9 Honeywell International Inc.

- 10.10 IEI Integration Corp.

- 10.11 InoNet Computer GmbH

- 10.12 Kontron

- 10.13 Mitsubishi Electric Corporation

- 10.14 Nexcom International

- 10.15 Panelmate

- 10.16 Quinta

- 10.17 Schneider Electric

- 10.18 Siemens AG