PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959585

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959585

Corrugated Boxes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

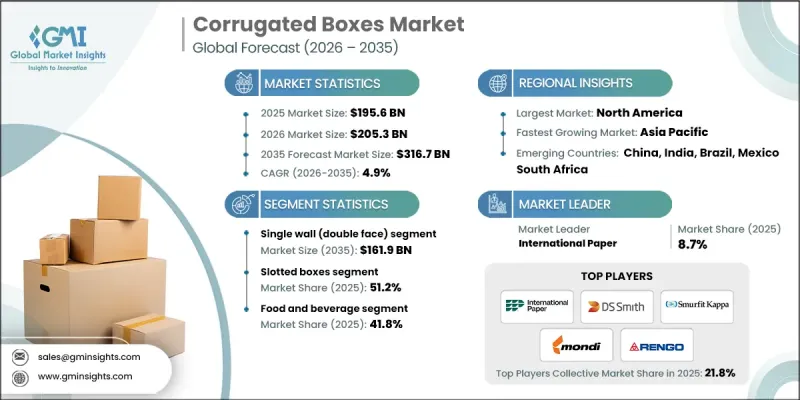

The Global Corrugated Boxes Market was valued at USD 195.6 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 316.7 billion by 2035.

The market is expanding rapidly, driven primarily by the surge in e-commerce and online retail, which demands reliable, durable, and cost-efficient packaging solutions. Rising consumption of FMCG products, including personal care, household goods, and food & beverages, is further fueling the need for corrugated boxes. Businesses increasingly recognize packaging as a strategic marketing tool that protects products, optimizes storage, and enables branding. Digital innovations, including QR codes, NFC tags, and augmented reality features, are enhancing consumer engagement and brand visibility. Lightweight yet strong corrugated materials are gaining preference, as they reduce shipping costs and environmental impact without compromising product protection. Urbanization and rising per capita income in emerging regions are driving FMCG demand, which in turn strengthens the global corrugated packaging sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $195.6 Billion |

| Forecast Value | $316.7 Billion |

| CAGR | 4.9% |

The single wall (double face) segment is projected to reach USD 161.9 billion by 2035. Demand for single wall double face corrugated boxes is rising due to their optimal balance of affordability, strength, and recyclability. These boxes are ideal for lightweight to medium-weight products, support high-volume production, and are compatible with automated packaging lines. Their sustainability and cost-effectiveness make them the preferred choice for manufacturers aiming to reduce environmental impact while maintaining operational efficiency.

The self-erecting boxes segment is expected to grow at a CAGR of 5.2% between 2026 and 2035. Companies are increasingly adopting self-erecting boxes to enhance operational efficiency, reduce labor dependency, and accelerate packing processes. These boxes allow consistent performance and faster assembly, making them highly suitable for e-commerce fulfillment centers, foodservice operations, and automated warehouses. The increasing adoption of automation and demand for scalable packaging solutions are major factors driving growth in this segment.

North America Corrugated Boxes Market held a 28.5% share in 2025. The region benefits from a mature manufacturing base, robust infrastructure, and advanced logistics networks. Corrugated boxes are preferred for their durability, recyclability, and product protection capabilities. The United States dominates this market, driven by demand from retail, industrial shipping, and consumer goods sectors. High-volume production, sophisticated supply chains, and growing e-commerce penetration contribute to the strong adoption of corrugated packaging solutions in the region.

Key players operating in the Global Corrugated Boxes Market include DS Smith, Smurfit Westrock, Mondi, Acme Machinery, Fosber Group, Packaging Corporation of America, Bohui Group, DING SHUNG MACHINERY, Dongguang Ruichang Carton Machinery, International Paper, Lee & Man Paper Manufacturing Ltd, Natraj Industries, NBM Pack, GB Pack, Nine Dragons Worldwide (China) Investment Group Co., Ltd., Packsize International, National Carton Factory (NCF), Pretoria Box Manufacturers (Pty) Ltd, Rengo Co. Ltd, Shanghai PrintYoung International Industry, and Shengli Carton Equipment Manufacturing. Companies in the corrugated boxes market are pursuing multiple strategies to strengthen their presence and market share. They are investing in R&D to develop lightweight, high-strength, and sustainable corrugated materials. Collaboration with e-commerce, FMCG, and industrial players allows for customized packaging solutions that meet specific operational and branding needs. Many are integrating smart packaging technologies such as QR codes, AR, and NFC to enhance consumer engagement and drive brand differentiation. Expansion of production facilities and global distribution networks ensures faster delivery and wider market reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Board type trends

- 2.2.2 Box style trends

- 2.2.3 Material type trends

- 2.2.4 Printing technology trends

- 2.2.5 Distribution channel trends

- 2.2.6 End use application trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in E-commerce and online retail channels

- 3.2.1.2 Expansion of fast moving consumer goods (FMCG) sector

- 3.2.1.3 Growth in food and beverage packaging requirements

- 3.2.1.4 Shift from plastic to paper-based packaging solutions

- 3.2.1.5 Emerging market urbanization and retail infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High raw material price volatility

- 3.2.2.2 High transportation and storage costs for bulk corrugated boxes

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for sustainable and biodegradable packaging solutions

- 3.2.3.2 Increasing adoption of smart and intelligent packaging technologies

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging Business Models

- 3.8 Compliance Requirements

- 3.9 Sustainability Measures

- 3.9.1 Sustainable Materials Assessment

- 3.9.2 Carbon Footprint Analysis

- 3.9.3 Circular Economy Implementation

- 3.9.4 Sustainability Certifications and Standards

- 3.9.5 Sustainability ROI Analysis

- 3.10 Global Consumer Sentiment Analysis

- 3.11 Patent Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Board Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Single face

- 5.3 Single wall (double face)

- 5.4 Double wall

- 5.5 Triple wall

Chapter 6 Market Estimates and Forecast, By Box Style, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Slotted boxes

- 6.3 Telescope boxes

- 6.4 Folder boxes

- 6.5 Rigid boxes

- 6.6 Self-erecting boxes

- 6.7 Interior forms

Chapter 7 Market Estimates and Forecast, By Material Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Linerboard

- 7.3 Medium

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Flexographic printing

- 8.3 Digital printing

- 8.4 Litho-label / offset printing

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Offline

- 9.3 Online

Chapter 10 Market Estimates and Forecast, By End-Use Application, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Food & beverage

- 10.3 E-commerce & direct-to-consumer

- 10.4 Electronics & electrical goods

- 10.5 Pharmaceuticals & healthcare

- 10.6 Industrial & manufacturing goods

- 10.7 Automotive & vehicle parts

- 10.8 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 International Paper

- 12.1.2 DS Smith

- 12.1.3 Smurfit Kappa

- 12.1.4 Mondi

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Packaging Corporation of America

- 12.2.1.2 Cascades Inc.

- 12.2.1.3 Visy

- 12.2.2 Europe

- 12.2.2.1 Rengo Co., Ltd.

- 12.2.2.2 GB Pack

- 12.2.2.3 Lee & Man Paper Manufacturing Ltd

- 12.2.3 APAC

- 12.2.3.1 Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- 12.2.3.2 TGI Packaging Pvt. Ltd

- 12.2.3.3 Natraj Industries

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 Dongguang Ruichang Carton Machinery

- 12.3.2 Shanghai PrintYoung International Industry

- 12.3.3 Shengli Carton Equipment Manufacturing

- 12.3.4 NBM Pack

- 12.3.5 Pretoria Box Manufacturers (Pty) Ltd

- 12.3.6 XINTIAN CARTON MACHINERY MANUFACTURING

- 12.3.7 Zemat Technology Group