PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959594

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959594

Automotive Electronics Control Unit (ECU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

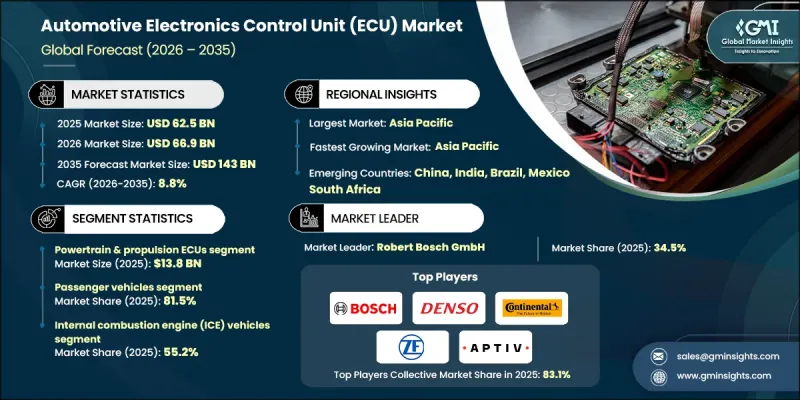

The Global Automotive Electronics Control Unit Market was valued at USD 62.5 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 143 billion by 2035.

Rising consumer demand for connected, intelligent vehicles is driving the adoption of advanced infotainment and digital services in modern automobiles. Vehicles now integrate sophisticated systems that provide navigation, multimedia, internet connectivity, and seamless smartphone integration. Real-time traffic updates, streaming capabilities, and hands-free communication are becoming standard expectations for drivers. Additionally, vehicle-to-everything (V2X) communication supported by ECUs enhances safety by offering collision warnings and live traffic signal information. Automakers are investing heavily in these technologies to deliver smart, connected vehicles that combine convenience, entertainment, and safety. Regulatory mandates aimed at improving fuel efficiency, reducing emissions, and enhancing road safety, such as Euro 6 and Corporate Average Fuel Economy standards, are further accelerating R&D efforts toward eco-friendly and technologically advanced vehicle systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $62.5 Billion |

| Forecast Value | $143 Billion |

| CAGR | 8.8% |

The powertrain and propulsion ECU segment was valued at USD 13.8 billion in 2025 and is expected to grow at a CAGR of 10.2% from 2026 to 2035. These ECUs optimize fuel efficiency, enhance vehicle performance, and manage emissions. In electrified vehicles, they coordinate conventional engines with electric motors for seamless power delivery and energy recovery. Centralized ECU architectures are gaining momentum, combining multiple domains to reduce wiring complexity while supporting advanced vehicle functionalities.

The passenger vehicle segment held a share of 81.5% in 2025, driven by increasing integration of connected services, advanced infotainment, and safety systems. Luxury and mid-size vehicles are increasingly equipped with premium ECUs supporting advanced driver-assistance systems, electrification, and software-driven features, delivering superior intelligent driving experience.

North America Automotive Electronics Control Unit Market accounted for 27.7% share in 2025. Growth in the region is fueled by early adoption of advanced automotive electronics, high EV penetration, and the shift toward software-defined vehicle architectures. Manufacturers are moving from distributed ECU systems to domain-based and centralized computing architectures to enhance ADAS, connectivity, and electrified powertrain capabilities. Strong R&D investment, stringent safety regulations, and rising demand for connected services across passenger and commercial vehicles are driving ECU adoption.

Prominent players operating in the Global Automotive Electronics Control Unit Market include Aptiv PLC, Autoliv Inc., Continental AG, Denso Corporation, Hella GmbH & Co. KGaA, Hitachi Astemo, Ltd., Hyundai Mobis Co., Ltd., Lear Corporation, Magneti Marelli (a CK Holdings Company), Mitsubishi Electric Corporation, Panasonic Holdings Corporation, Robert Bosch GmbH, United Automotive Electronic Systems (UAES), Valeo SA, and ZF Friedrichshafen AG. Key strategies adopted by companies in the Global Automotive Electronics Control Unit Market include accelerating innovation in centralized and domain-based architectures to simplify vehicle electronics and enhance performance. Manufacturers are focusing on developing high-precision, software-defined ECUs that support advanced driver-assistance systems, infotainment, and electrified powertrains. Strategic partnerships with automakers, software providers, and semiconductor companies allow companies to integrate advanced features while meeting regulatory compliance. Expanding regional presence, particularly in high-growth EV markets, and investing in localized R&D centers enables rapid customization and faster time-to-market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 ECU type trends

- 2.2.2 Vehicle type trends

- 2.2.3 Propulsion type trends

- 2.2.4 E/E Architecture type trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing connectivity and infotainment features

- 3.2.1.2 Rising demand for electric vehicles (EVs)

- 3.2.1.3 Increasing complexity of vehicle systems

- 3.2.1.4 Demand for enhanced safety features

- 3.2.1.5 Advancements in autonomous driving

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory standards

- 3.2.2.2 Supply chain disruptions

- 3.2.3 Market opportunities

- 3.2.3.1 Transition from distributed ECUs to domain and centralized architectures

- 3.2.3.2 Integration of ai and sensor fusion in vehicle control systems

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By ECU Type, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Powertrain & propulsion ECUs

- 5.2.1 Engine control units (ECU/ECM)

- 5.2.2 Transmission control units (TCU)

- 5.2.3 Hybrid control units (HCU)

- 5.3 Electrification ECUs

- 5.3.1 Battery management systems (BMS)

- 5.3.2 Inverter control units

- 5.3.3 Charging control units (onboard charger ECU)

- 5.3.4 Power control units (PCU)

- 5.4 Safety & ADAS ECUs

- 5.4.1 Foundation safety ECUs (ABS, ESC, airbag)

- 5.4.2 Adas domain controllers (level 2-3)

- 5.4.3 Automated parking ECUs

- 5.4.4 High-automation ECUs (level 4+)

- 5.5 Body control ECUs

- 5.5.1 Body control modules (BCM)

- 5.5.2 Lighting control units

- 5.5.3 HVAC control units

- 5.6 Infotainment & connectivity ECUs

- 5.6.1 Infotainment control units (head units)

- 5.6.2 Telematics control units (TCU)

- 5.6.3 Gateway ECUs

- 5.7 Chassis & dynamics ECUs

- 5.7.1 Steering control units

- 5.7.2 Suspension control units

- 5.8 Advanced architecture ECUs

- 5.8.1 Domain controllers

- 5.8.2 Zone controllers

- 5.8.3 Central vehicle controllers (CVC)

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.3 Commercial vehicles

- 6.4 Off-highway vehicles

Chapter 7 Market Estimates and Forecast, By Protection Type, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Internal combustion engine (ICE) vehicles

- 7.3 Hybrid electric vehicles (HEV) / plug-in hybrid electric vehicles (PHEV)

- 7.4 Battery electric vehicles (BEV)

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Distributed ECU architecture

- 8.3 Domain controller architecture

- 8.4 Zonal architecture

- 8.5 Centralized / software-defined vehicle (SDV) architecture

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Robert Bosch GmbH

- 10.1.2 Denso Corporation

- 10.1.3 Continental AG

- 10.1.4 ZF Friedrichshafen AG

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Aptiv PLC

- 10.2.1.2 Autoliv Inc.

- 10.2.1.3 Lear Corporation

- 10.2.2 Europe

- 10.2.2.1 Valeo SA

- 10.2.2.2 Hella GmbH & Co. KGaA

- 10.2.2.3 Magneti Marelli (a CK Holdings Company)

- 10.2.3 APAC

- 10.2.3.1 Hitachi Astemo, Ltd.

- 10.2.3.2 Hyundai Mobis Co., Ltd.

- 10.2.3.3 Mitsubishi Electric Corporation

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Panasonic Holdings Corporation

- 10.3.2 United Automotive Electronic Systems (UAES)