PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959597

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959597

Automotive Belt Tensioner Pulleys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

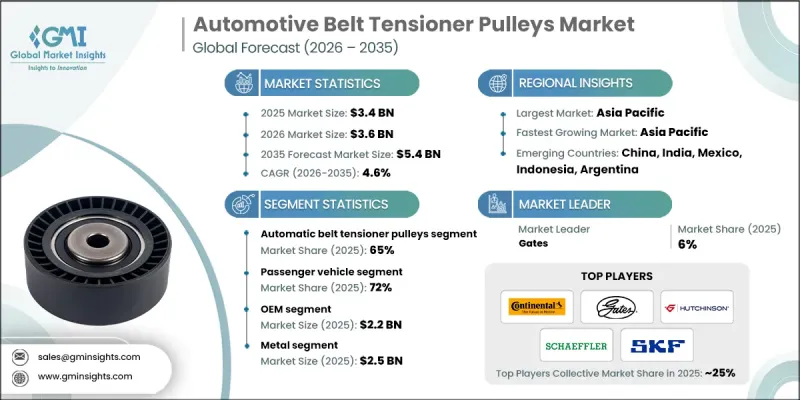

The Global Automotive Belt Tensioner Pulleys Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 5.4 billion by 2035.

Market growth remains tied to the continued dominance of internal combustion engines and hybrid vehicles, which together represent many vehicles in operation worldwide over the medium term. These vehicle platforms depend on belt-driven systems for consistent mechanical performance, making belt tensioner pulleys a critical component for reliability and efficiency. While electric vehicles continue to expand their presence, hybrid platforms retain conventional belt architectures, helping stabilize overall demand. The market benefits from long vehicle life cycles, steady replacement requirements, and ongoing engineering refinements that improve durability and performance. Growing mechanical complexity within modern powertrains places higher operational stress on belt systems, increasing the need for accurately engineered tensioning solutions. As a result, the market continues to show steady expansion supported by both original equipment demand and a resilient replacement cycle, even as vehicle production volumes fluctuate across regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.4 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 4.6% |

Automotive belt tensioner pulleys experience gradual mechanical degradation due to constant operational stress, making replacement essential over a vehicle's lifetime. An expanding global vehicle population, particularly aging fleets in developed and emerging regions, continues to support consistent aftermarket demand. This replacement-driven consumption provides revenue stability and offsets short-term variations in new vehicle output, reinforcing the long-term growth outlook.

The automatic belt tensioner pulleys segment accounted for 65% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. These systems have become standard across modern internal combustion and hybrid vehicles due to their ability to maintain optimal belt force automatically, reducing operational risk and extending component lifespan while improving overall system reliability.

The OEM segment reached USD 2.2 billion in 2025. OEM demand remains aligned with global production of internal combustion and hybrid vehicles, supported by long-term supplier agreements that emphasize engineering collaboration, cost efficiency, quality compliance, and early-stage integration into vehicle development programs.

United States Automotive Belt Tensioner Pulleys Market generated USD 793.1 million in 2025. Demand is supported by vehicles operating under higher mechanical loads, which increases requirements for advanced tensioner designs and higher-value components. A well-developed aftermarket infrastructure further strengthens replacement demand and enhances market stability nationwide.

Key companies operating in the Global Automotive Belt Tensioner Pulleys Market include Schaeffler, Gates, Continental, SKF, NTN, Dayco Products, Hutchinson, Aisin Seiki, Litens Automotive, and NSK Automation. Companies in the automotive belt tensioner pulleys market are reinforcing their market position through product innovation, material advancements, and close collaboration with vehicle manufacturers. Many suppliers are investing in next-generation designs that enhance durability, reduce noise, and improve thermal performance. Expansion of manufacturing capacity in key automotive regions is helping companies optimize costs and ensure supply reliability. Firms are also strengthening aftermarket distribution networks to capture recurring replacement demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022-2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Material

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Manufacturers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Service providers

- 3.1.1.4 Distributors

- 3.1.1.5 End-users

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Continued dominance of ICE and hybrid vehicle parcels

- 3.2.1.2 Large and aging global vehicle fleet driving aftermarket demand

- 3.2.1.3 Increasing accessory load and engine complexity

- 3.2.1.4 OEM focus on NVH reduction and durability

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Accelerating electrification of vehicle powertrains

- 3.2.2.2 Rapid decline of hydraulic power steering systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of hybrid vehicle production

- 3.2.3.2 Growth in aftermarket repair kits and system solutions

- 3.2.3.3 Vehicle production growth in emerging markets

- 3.2.3.4 Innovation in lightweight and low-friction pulley designs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 FMVSS (Federal Motor Vehicle Safety Standards - United States)

- 3.4.1.2 EPA Emission Regulations (United States)

- 3.4.1.3 CARB Emission Standards (California Air Resources Board)

- 3.4.2 Europe

- 3.4.2.1 EU Type Approval Framework (Regulation (EU) 2018/858)

- 3.4.2.2 Euro 6 and Euro 7 Emission Standards

- 3.4.2.3 End-of-Life Vehicles (ELV) Directive

- 3.4.2.4 REACH Regulation

- 3.4.2.5 OEM-Specific NVH and Durability Compliance Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 Bharat Stage VI (BS VI) Emission Norms - India

- 3.4.3.2 Automotive Industry Standards (AIS) - India

- 3.4.3.3 China VI Emission Standards

- 3.4.3.4 China Compulsory Certification (CCC)

- 3.4.3.5 Japan Automotive Standards and Regulations (JASO / MLIT)

- 3.4.4 Latin America

- 3.4.4.1 PROCONVE Emission Standards - Brazil

- 3.4.4.2 Inmetro Automotive Certification - Brazil

- 3.4.4.3 NOM Vehicle Safety and Emission Standards - Mexico

- 3.4.4.4 Mercosur Automotive Regulatory Framework

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) Vehicle Regulations

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.3 South African Bureau of Standards (SABS) Automotive Regulations

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Cost breakdown analysis

- 3.9.1 Vendor cost structure

- 3.9.2 Implementation of cost components

- 3.9.3 Ongoing operational costs

- 3.9.4 Indirect customer costs

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Patent analysis

- 3.12 Impact of Electrification

- 3.12.1 Reduction of belt-driven components in battery electric vehicles

- 3.12.2 Sustained demand from hybrid and mild-hybrid powertrains

- 3.12.3 Electrification of auxiliary systems reducing pulley applications

- 3.12.4 Regional variation in electrification impact

- 3.12.5 Aftermarket demand support from large ICE vehicle

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Automatic belt tensioner pulleys

- 5.3 Manual belt tensioner pulleys

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicle

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUVs

- 6.3 Commercial vehicle

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Medium commercial vehicles (MCVs)

- 6.3.3 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Metal

- 7.3 Plastic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Engine timing system

- 8.3 Alternator system

- 8.4 Power steering system

- 8.5 Air conditioning system

- 8.6 Water pump system

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Denmark

- 10.3.9 Belgium

- 10.3.10 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global leaders

- 11.1.1 Aisin Seiki

- 11.1.2 Continental

- 11.1.3 Dayco Products

- 11.1.4 Gates

- 11.1.5 Hutchinson

- 11.1.6 NSK

- 11.1.7 NTN

- 11.1.8 Schaeffler

- 11.1.9 SKF

- 11.1.10 The Timken Company

- 11.2 Regional players

- 11.2.1 Tsubaki Automotive

- 11.2.2 Bando Chemical Industries

- 11.2.3 Federal-Mogul Motorparts

- 11.2.4 Mevotech

- 11.2.5 Delphi

- 11.2.6 VDO

- 11.2.7 NTN-SNR

- 11.2.8 Marelli

- 11.2.9 Mahle

- 11.2.10 Febi Bilstein

- 11.2.11 Cloyes Gear & Products

- 11.2.12 Denso

- 11.3 Emerging players

- 11.3.1 Litens Automotive

- 11.3.2 Mubea

- 11.3.3 GMB

- 11.3.4 Roulunds Braking

- 11.3.5 Cloyes Gear & Products