PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959609

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959609

Military and Defense Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

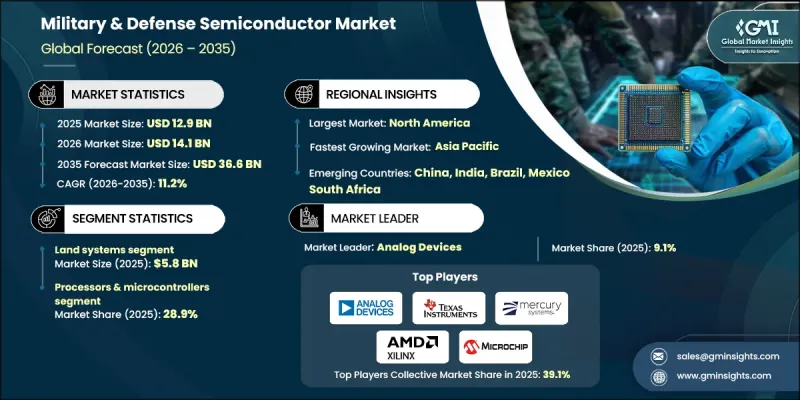

The Global Military & Defense Semiconductor Market was valued at USD 12.9 billion in 2025 and is estimated to grow at a CAGR of 11.2% to reach USD 36.6 billion by 2035.

The market is witnessing strong momentum as governments worldwide continue to increase defense spending and prioritize technological superiority. Higher budget allocations are accelerating research, development, and deployment of advanced semiconductor solutions across communication networks, intelligence systems, radar platforms, electronic warfare, and precision-guided equipment. Modern defense infrastructure increasingly depends on high-performance semiconductor components that enable faster data processing, secure connectivity, real-time analytics, and system interoperability. Semiconductors used in military and defense applications function as critical electronic materials with controlled conductivity, forming the foundation of microprocessors, integrated circuits, sensors, and power management devices. These components are central to the performance, efficiency, and reliability of advanced defense electronics. As armed forces modernize air, land, naval, and space capabilities, demand for rugged, secure, and energy-efficient semiconductor technologies continues to rise, supporting sustained long-term market expansion across global defense ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.9 Billion |

| Forecast Value | $36.6 Billion |

| CAGR | 11.2% |

At the same time, export controls and geopolitical tensions present structural challenges for the military & defense semiconductor market. Strict trade regulations and national security policies limit the cross-border transfer of sensitive technologies, restricting global supply chain flexibility. Governments are implementing protective measures to safeguard strategic semiconductor capabilities, which can slow procurement cycles and create sourcing constraints. Geopolitical uncertainties further intensify supply chain volatility, making localized production and secure sourcing increasingly important for defense applications.

The land systems segment generated USD 5.8 billion in 2025 and is expected to grow at a CAGR of 11.8% between 2026 and 2035. Semiconductor integration within ground-based platforms is expanding as defense organizations incorporate autonomous navigation, advanced sensing, and secure communication technologies into tactical systems. Real-time data processing, mission coordination, and resilient communication networks are essential requirements driving semiconductor adoption in this segment. Durable, low-power, and high-reliability components are being deployed to ensure operational continuity in demanding environments, reinforcing the importance of specialized semiconductor design for land-based military applications.

The processors & microcontrollers segment accounted for 28.9% share in 2025. Rising demand for high-performance computing in defense platforms is accelerating the adoption of advanced processing technologies. Modern defense systems require embedded intelligence, encryption capability, secure communications, and AI-enabled analytics, all supported by sophisticated processors. In addition, ruggedized and power-efficient microcontrollers are gaining traction for deployment in compact defense electronics, unmanned systems, and portable military equipment. These technologies enhance command control, automation, and operational efficiency across multiple mission-critical applications.

North America Military & Defense Semiconductor Market held a 45.1% share in 2025. Regional growth is supported by ongoing modernization programs across air, ground, naval, and space platforms. Increased emphasis on artificial intelligence, autonomous systems, cybersecurity, and advanced communications infrastructure continues to fuel demand for high-performance semiconductor technologies. Recurring upgrade cycles, system retrofitting, and maintenance programs also sustain long-term procurement activity. Furthermore, government initiatives aimed at strengthening domestic semiconductor manufacturing capacity are enhancing regional self-reliance and reducing dependence on foreign suppliers for critical defense components.

Key companies operating in the Global Military & Defense Semiconductor Market include Texas Instruments, Lockheed Martin, Analog Devices, Northrop Grumman, Microchip Technology, Raytheon Technologies, Infineon Technologies, General Dynamics, STMicroelectronics, L3Harris Technologies, Boeing, and BAE Systems. Companies in the military & defense semiconductor market strengthen their competitive position by investing heavily in research and development focused on secure, rugged, and high-performance chip architectures. Strategic partnerships with defense contractors and government agencies help align product development with mission-specific requirements. Many firms are expanding domestic manufacturing capabilities to address supply chain security and comply with national security regulations. Portfolio diversification across processors, sensors, power devices, and communication chips enhances cross-platform integration opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing government investments in military

- 3.2.1.2 Utilization of radiation-tolerant semiconductor components

- 3.2.1.3 Increasing aircraft upgrades and modernization programs

- 3.2.1.4 Growing demand for advanced semiconductor technologies

- 3.2.1.5 Increasing use of Artificial Intelligence (AI) and Machine Learning (ML) in military operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and long development cycles

- 3.2.2.2 Export restrictions and geopolitical tensions

- 3.2.3 Market opportunities

- 3.2.3.1 Advancements in electronic warfare and communication systems

- 3.2.3.2 High-performance computing for defense simulation and command systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.14.3 Defense budget allocation by segment

- 3.14.3.1 Personnel

- 3.14.3.2 Operations and maintenance

- 3.14.3.3 Procurement

- 3.14.3.4 Research, development, test and evaluation

- 3.14.3.5 Infrastructure and construction

- 3.14.3.6 Technology and innovation

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.1.1 Processors & microcontrollers

- 5.1.2 General-purpose processors

- 5.1.3 AI/ML processors

- 5.1.4 Cryptographic processors

- 5.1.5 Digital signal processors

- 5.1.6 Microcontrollers

- 5.2 Memory devices

- 5.2.1 SRAM (static RAM)

- 5.2.2 DRAM (dynamic RAM)

- 5.2.3 Flash memory (NAND, NOR)

- 5.2.4 MRAM (magnetoresistive RAM)

- 5.2.5 EEPROM/NVRAM

- 5.3 Logic devices

- 5.3.1 ASICs (application-specific integrated circuits)

- 5.3.2 FPGAs (field-programmable gate arrays)

- 5.3.3 PLDs (programmable logic devices)

- 5.3.4 CPLDs (complex programmable logic devices)

- 5.4 RF & microwave components

- 5.4.1 MMICs (monolithic microwave ICs)

- 5.4.2 T/R modules (transmit/receive modules)

- 5.4.3 RF power amplifiers

- 5.4.4 Others

- 5.5 Power management ICs

- 5.5.1 DC-DC converters (buck, boost, buck-boost, isolated)

- 5.5.2 LDOs (low-dropout regulators)

- 5.5.3 Power MOSFETs & gate drivers

- 5.5.4 Others

- 5.6 Analog & mixed-signal ICs

- 5.6.1 Operational amplifiers

- 5.6.2 Comparators

- 5.6.3 Analog switches & multiplexers

- 5.6.4 Others

- 5.7 Data converters (ADC/DAC)

- 5.8 Optoelectronics

- 5.9 Discrete semiconductors

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Land systems

- 6.2.1 Combat vehicles (tanks, IFVs, APCs)

- 6.2.2 Tactical vehicles (HMMWVs, MRAPs, trucks)

- 6.2.3 Artillery systems

- 6.2.4 Ground-based air defense

- 6.2.5 Others

- 6.3 Naval systems

- 6.3.1 Surface combatants

- 6.3.2 Aircraft carriers

- 6.3.3 Submarines

- 6.3.4 Amphibious warfare ships

- 6.3.5 Others

- 6.4 Airborne systems

- 6.4.1 Fighter aircraft

- 6.4.2 Transport & tanker aircraft

- 6.4.3 Helicopters

- 6.4.4 UAVs

- 6.4.5 Others

- 6.5 Space systems

- 6.5.1 Military communications satellites

- 6.5.2 Reconnaissance & surveillance satellites

- 6.5.3 Navigation satellites

- 6.5.4 Missile warning satellites

- 6.5.5 Space situational awareness

- 6.5.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Global Key Players

- 8.1.1 Lockheed Martin

- 8.1.2 Raytheon Technologies

- 8.1.3 Northrop Grumman

- 8.1.4 Boeing

- 8.2 Regional Key Players

- 8.2.1 North America

- 8.2.1.1 General Dynamics

- 8.2.1.2 L3Harris Technologies

- 8.2.1.3 Analog Devices

- 8.2.2 Europe

- 8.2.2.1 BAE Systems

- 8.2.2.2 Thales Group

- 8.2.2.3 Infineon Technologies

- 8.2.1 North America

- 8.3 Niche Players / Disruptors

- 8.3.1 Microchip Technology

- 8.3.2 Texas Instruments

- 8.3.3 STMicroelectronics