PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959611

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959611

Intelligent Power Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

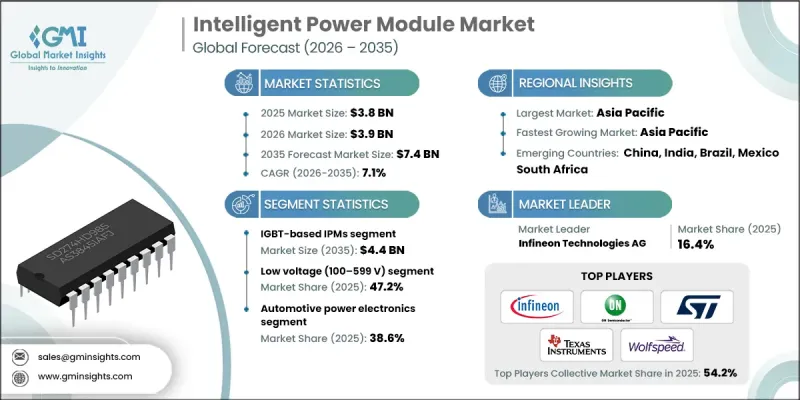

The Global Intelligent Power Module Market was valued at USD 3.8 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 7.4 billion by 2035.

The market growth is driven by continuous advancements in Silicon Carbide (SiC) power module technologies, which enhance efficiency, operational reliability, and power density in electric mobility solutions. There is a growing trend toward higher functional integration, with IPMs now combining power devices, gate drivers, protection circuits, and sensing functions within compact packages. This integration simplifies system design, reduces development time for OEMs, and improves overall system performance. Rising government regulations to curb greenhouse gas emissions, especially CO2, are boosting the adoption of renewable energy and energy conversion systems that rely on high-performance IPMs. Advanced packaging techniques, including double-sided cooling, low-inductance connections, and transfer-molded modules, are enabling improved thermal management, higher switching frequencies, and lower losses. The market is also witnessing increased integration of digital monitoring and diagnostic tools, providing predictive maintenance capabilities and optimizing performance across application-specific modules for traction inverters, HVAC systems, and renewable energy converters.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.8 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 7.1% |

The IGBT-based IPM segment is forecasted to reach USD 4.4 billion by 2035. IGBT-based modules continue to dominate traditional industrial and automotive applications due to their reliability, cost-effectiveness, and performance at medium-voltage levels. There is a noticeable push toward higher switching frequencies, enhanced thermal management, and the addition of digital diagnostic capabilities to improve control and efficiency in motor drives, traction inverters, and industrial automation equipment.

The automotive power electronics segment accounted for 38.6% share in 2025. In automotive applications, IPMs are trending toward high integration with electric vehicle inverters, onboard chargers, and DC-DC converters. Key growth drivers include SiC adoption, improved thermal management, compact high-power-density designs, and advanced diagnostic features that support EV range, efficiency, and performance requirements.

North America Intelligent Power Module Market held a share of 29.5% in 2025. Market expansion in this region is driven by robust industrial automation initiatives, increasing adoption of electric mobility solutions, and government policies promoting energy efficiency. The United States represents the largest regional consumer, with growing traction for renewable energy converters, traction inverters, and high-end industrial power electronics platforms, supported by federal incentives to optimize power conversion and minimize system losses.

Key players in the Global Intelligent Power Module Market include Littelfuse, Inc., Infineon Technologies AG, STMicroelectronics N.V., Renesas Electronics Corporation, Alpha & Omega Semiconductor Ltd. (AOS), Sanken Electric Co., Ltd., Fuji Electric Co., Ltd., Mitsubishi Electric Corporation, Powerex Inc., ROHM Co., Ltd., Hitachi Power Semiconductor Device Ltd., Microchip Technology Inc. (including Microsemi), Silan Semiconductor / Hangzhou Silan Microelectronics, ON Semiconductor Corporation (onsemi), and Semikron Danfoss GmbH & Co. KG. Companies in the intelligent power module market are pursuing multiple strategies to strengthen their market foothold. R&D investment is prioritized to develop higher efficiency, SiC-based, and multi-functional IPMs with integrated diagnostic and thermal management features. Strategic partnerships with OEMs, renewable energy developers, and EV manufacturers help expand adoption across applications. Firms are offering modular, application-specific solutions to reduce design complexity and enhance system performance. Geographic expansion into emerging markets, alongside local manufacturing and service capabilities, allows companies to capture regional demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Device technology type trends

- 2.2.2 Voltage class trends

- 2.2.3 Power rating trends

- 2.2.4 Current rating trends

- 2.2.5 Application trends

- 2.2.6 End-user industry trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification of transportation and electric vehicle adoption

- 3.2.1.2 Rapid expansion of renewable energy and smart grid infrastructure

- 3.2.1.3 Advancements in silicon carbide power module technology for e-mobility applications

- 3.2.1.4 Supportive government policies for energy efficiency and electrification

- 3.2.1.5 Miniaturization and high-power density requirements in electronics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced power semiconductor materials

- 3.2.2.2 Complex thermal management and packaging challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Accelerated adoption of electric and hybrid vehicles

- 3.2.3.2 Rising demand for industrial automation and smart manufacturing

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Device Technology Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 IGBT-based IPMs

- 5.3 MOSFET-based IPMs

- 5.4 Silicon Carbide (SiC) IPMs

- 5.5 Gallium Nitride (GaN) IPMs

Chapter 6 Market Estimates and Forecast, By Voltage Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Low voltage (100-599 V)

- 6.3 Medium voltage (600-1699 V)

- 6.4 High voltage (1700 V and above)

Chapter 7 Market Estimates and Forecast, By Power Rating, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Low power (<1 kW)

- 7.3 Medium power (1-10 kW)

- 7.4 High power (>10 kW)

Chapter 8 Market Estimates and Forecast, By Current Rating, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Ultra-low current (2-9 A)

- 8.3 Low current (10-49 A)

- 8.4 Medium current (50-149 A)

- 8.5 High current (150-450 A)

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Automotive power electronics

- 9.3 Renewable energy systems

- 9.4 Consumer appliances

- 9.5 Industrial automation

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Automotive & transportation

- 10.3 Consumer electronics & appliances

- 10.4 Renewable energy & power generation

- 10.5 Data centers & it infrastructure

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Infineon Technologies AG

- 12.1.2 Mitsubishi Electric Corporation

- 12.1.3 STMicroelectronics N.V.

- 12.1.4 Texas Instruments Inc.

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 ON Semiconductor Corporation (onsemi)

- 12.2.1.2 Microchip Technology Inc. (incl. Microsemi)

- 12.2.1.3 Wolfspeed, Inc.

- 12.2.2 Europe

- 12.2.2.1 Semikron Danfoss GmbH & Co. KG

- 12.2.2.2 Vincotech GmbH

- 12.2.2.3 Vishay Intertechnology Inc.

- 12.2.3 APAC

- 12.2.3.1 Fuji Electric Co., Ltd.

- 12.2.3.2 Renesas Electronics Corporation

- 12.2.3.3 ROHM Co., Ltd.

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 Alpha & Omega Semiconductor Ltd. (AOS)

- 12.3.2 Hitachi Power Semiconductor Device Ltd.

- 12.3.3 Littelfuse, Inc.

- 12.3.4 Powerex Inc.

- 12.3.5 Sanken Electric Co., Ltd.

- 12.3.6 Silan Semiconductor / Hangzhou Silan Microelectronics

- 12.3.7 Toshiba Electronic Devices & Storage Corp.