PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959615

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959615

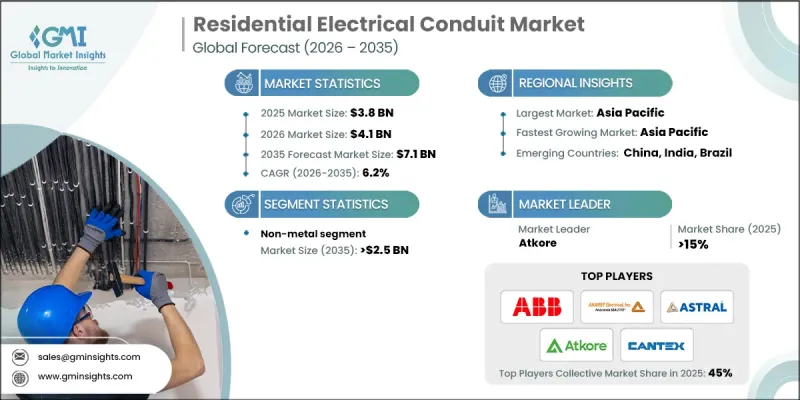

Residential Electrical Conduit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Residential Electrical Conduit Market was valued at USD 3.8 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 7.1 billion by 2035.

The growth is driven by the electrification of homes, increased adoption of at-home EV charging, and rising deployment of low-voltage circuits and protective raceways in residential properties. The proliferation of private EV chargers is fueling demand for additional branch circuits, conduits, and code-compliant installations in garages, driveways, and rooftops. Energy-efficient home upgrades, including heat pumps, induction appliances, and improved insulation, are further boosting conduit and cable management requirements. Distributed rooftop solar and behind-the-meter energy storage systems are creating additional pathways for residential wiring, increasing the need for durable conduit and fittings. Stricter building policies in Europe, retrofitting mandates in Canada, and initiatives to decarbonize social housing in the UK are further accelerating market adoption. As homeowners and builders prioritize safety, energy efficiency, and future-ready electrical infrastructure, demand for high-quality residential conduits, elbows, and expansion fittings continues to rise globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.8 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 6.2% |

The non-metallic segment captured a 34.6% share in 2025 and is expected to reach USD 2.5 billion by 2035. Non-metallic conduits, such as PVC and listed polymer systems, are preferred for their corrosion resistance, lightweight design, and cost efficiency, particularly in moisture-prone or coastal regions. These conduits simplify installation with easy cutting, solvent welding, and long-sweep runs, reducing labor costs while providing a clean aesthetic for modern residential designs. Their dielectric and thermal properties support outdoor circuits for rooftop PV, pool systems, and irrigation. Rising demand for accessories such as UV-stabilized fittings, adhesives, and bushings ensures consistent revenue streams for distributors and contractors.

The electrification projects are increasingly driving demand for 11/4-2 inch conduits, as Level 2 EV chargers, heat pumps, and induction appliances require higher ampacity conductors, enhanced heat dissipation, and future-ready pathways. Installers are upsizing runs in garages, rooftops, and exterior pads to accommodate spares, load management hardware, and potential energy storage, optimizing fill, thermal performance, and labor productivity. This practice also boosts conduit footage per project, increases fitting counts, and standardizes components like elbows and LB bodies, strengthening mid-size conduit pull-through for wholesalers and contractors.

U.S. Residential Electrical Conduit Market was valued at USD 561.4 million in 2025. Market expansion is largely fueled by electrification retrofits, EV charger installations, heat pump deployment, rooftop PV systems, and related service upgrades. These activities increase conduit footage, diameter requirements, and accessory utilization, creating opportunities for suppliers and installers to scale their operations.

Major companies in the Global Residential Electrical Conduit Market include Anamet Electrical, ABB, Astral, Atkore, Austro Pipes, CANTEX, Champion Fiberglass, Electri-Flex, Guangdong Ctube Industry, HellermannTyton, Hubbell, IPEX Electrical, JM Eagle, Legrand, Liberty Electric Products, Robroy Industries, Schneider Electric, Tubecon, Wienerberger, and Zekelman Industries. Companies in the residential electrical conduit market are strengthening their presence through several key strategies. They are investing in research and development to introduce conduits with enhanced durability, heat resistance, and corrosion protection. Expansion of distribution networks ensures timely delivery to contractors, builders, and wholesalers. Strategic partnerships with construction firms and electrical contractors enable integrated project support. Product standardization, modular fittings, and UV-stabilized accessories improve labor efficiency and adoption rates. Firms are also focusing on sustainability by developing recyclable and environmentally friendly materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Trade size trends

- 2.1.3 Classification trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of electrical conduits

- 3.8 Emerging opportunities & trends

- 3.9 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Trade Size, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 1/2 to 1

- 5.3 1 1/4 to 2

- 5.4 2 1/2 to 3

- 5.5 3 to 4

- 5.6 5 to 6

- 5.7 Others

Chapter 6 Market Size and Forecast, By Classification, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Non-metal

- 6.4 Flexible

- 6.5 Underground

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 France

- 7.3.2 Germany

- 7.3.3 Italy

- 7.3.4 UK

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Anamet Electrical

- 8.3 Astral

- 8.4 Atkore

- 8.5 Austro Pipes

- 8.6 CANTEX

- 8.7 Champion Fiberglass

- 8.8 Electri-Flex

- 8.9 Guangdong Ctube Industry

- 8.10 HellermannTyton

- 8.11 Hubbell

- 8.12 IPEX Electrical

- 8.13 JM Eagle

- 8.14 Legrand

- 8.15 Liberty Electric Products

- 8.16 Robroy Industries

- 8.17 Schneider Electric

- 8.18 Tubecon

- 8.19 Wienerberger

- 8.20 Zekelman Industries