PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959616

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959616

North America Automotive Aluminum Wheels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

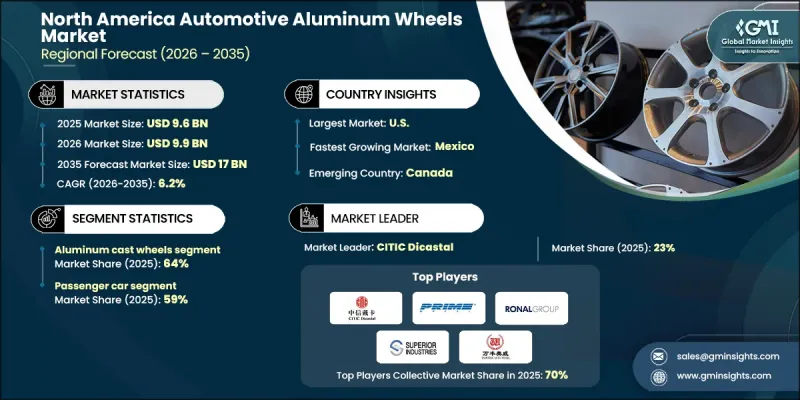

North America Automotive Aluminum Wheels Market was valued at USD 9.6 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 17 billion by 2035.

Market expansion is fueled by accelerating electric vehicle adoption across the region, as automakers prioritize lightweight materials to offset heavy battery systems. Aluminum wheels play a vital role in reducing unsprung weight, extending driving range, and improving thermal efficiency, making them a preferred OEM fitment in electric and hybrid vehicles. Growing consumer demand for performance-oriented vehicles and visually distinctive designs is also reinforcing adoption. Aluminum wheels are increasingly positioned as standard equipment across passenger vehicles and light trucks, structurally strengthening overall market penetration. In addition, automakers are leveraging wheel design as a differentiation strategy across trims and model variants, integrating advanced finishes and aerodynamic structures into mainstream offerings. As electrification reshapes product development strategies and consumer expectations evolve toward efficiency and design appeal, aluminum wheels continue to gain prominence across the North American automotive ecosystem through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.6 Billion |

| Forecast Value | $17 Billion |

| CAGR | 6.2% |

The United States Automotive Aluminum Wheels Market is witnessing strong growth, supported by the ongoing transition toward electric mobility that requires lightweight, high-performance wheel solutions. Larger vehicle categories continue to command significant sales share across the region, particularly in the United States and Canada. These vehicles are increasingly equipped with larger-diameter aluminum wheels ranging from 18 to 22 inches, enhancing durability, road presence, and styling. The higher aluminum wheel content per vehicle in these categories directly elevates average revenue per unit and strengthens total market value. Manufacturers are positioning aluminum wheel designs as a key visual and functional differentiator, offering machined, multi-spoke, and aerodynamic configurations across standard and mid-level trims. This strategic shift is accelerating aluminum wheel adoption beyond premium segments and into broader consumer markets.

The aluminum cast wheels segment held 64% share in 2025 and is anticipated to grow at a CAGR of 5.5% through 2035. OEM preference for cast aluminum wheels stems from their balanced combination of cost efficiency, weight savings, and design versatility. Compared to forged alternatives, cast wheels enable scalable manufacturing at lower production costs, making them well-suited for high-volume passenger vehicles and light-duty platforms across the region. Broader standardization of aluminum cast wheels across mid-range vehicle trims is further expanding their market penetration.

The passenger cars segment accounted for 59% share in 2025 and is projected to grow at a CAGR of 6% between 2026 and 2035. The increasing electrification of passenger vehicles in North America is accelerating the shift toward aluminum wheels, as automakers seek lightweight solutions to enhance driving range and overall efficiency. Aluminum wheels help offset battery weight while improving heat dissipation, making them an attractive option for mass-market electric sedans and compact vehicles. Consumer preference for enhanced aesthetics, ride quality, and performance is also driving aluminum wheels to become a standard feature in passenger cars.

United States Automotive Aluminum Wheels Market held 67% share, generating USD 6.5 billion in 2025. Strong consumer preference for larger vehicles significantly supports aluminum wheel demand, as these vehicles represent a substantial portion of new vehicle sales and are commonly equipped with aluminum wheels as standard equipment, particularly in mid- and higher-level trims. Rapid growth in US electric vehicle adoption is further amplifying demand for lightweight aluminum wheel solutions. Automakers increasingly rely on aluminum wheels to counterbalance battery mass, extend range, and optimize aerodynamic performance, solidifying their role as a default OEM choice across expanding electric passenger and light truck platforms.

Key companies operating in the North America Automotive Aluminum Wheels Market include Maxion Wheels, Superior Industries International, CITIC Dicastal, Alcoa Wheels, Ronal, Wanfeng, Central Motor Wheel of America, Lizhong, Prime Wheel, and Hands. Companies in the North America Automotive Aluminum Wheels Market are reinforcing their competitive position through capacity expansion, lightweight material innovation, and advanced manufacturing technologies. Leading manufacturers are investing in automation and precision casting processes to enhance efficiency and reduce production costs. Strategic partnerships with OEMs enable long-term supply agreements and integration into new electric vehicle platforms. Firms are also developing aerodynamic and design-focused wheel solutions to align with evolving consumer preferences. Portfolio diversification across cast and performance-oriented products strengthens market reach.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Sales channel

- 2.2.4 Vehicle

- 2.2.5 Rim size

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification-driven lightweighting

- 3.2.1.2 Rising SUV and pickup truck sales

- 3.2.1.3 Premiumization across mass-market vehicles

- 3.2.1.4 Growth of aftermarket customization

- 3.2.1.5 Advanced manufacturing technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in aluminum prices

- 3.2.2.2 Competition from steel and composite wheels

- 3.2.3 Market opportunities

- 3.2.3.1 EV platform expansion

- 3.2.3.2 Growth in Mexico-based manufacturing

- 3.2.3.3 Aftermarket premium wheel demand

- 3.2.3.4 Sustainable and recycled aluminum adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 US

- 3.4.1.1 Corporate Average Fuel Economy (CAFE) Standards

- 3.4.1.2 EPA Vehicle Emissions Regulations

- 3.4.1.3 U.S. Department of Transportation

- 3.4.2 Canada

- 3.4.2.1 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.2.2 Greenhouse Gas (GHG) Emissions standards for light-duty vehicles

- 3.4.2.3 Incentives for lightweight & fuel-efficient components

- 3.4.3 Mexico

- 3.4.3.1 NOM standards for vehicle components

- 3.4.3.2 Federal Environmental Protection Agency (PROFEPA) compliance

- 3.4.3.3 NAFTA / USMCA rules of origin for automotive parts

- 3.4.1 US

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.1.1 Standard aluminum alloys (A356, A357) vs. advanced alloys

- 3.6.1.2 Lightweighting alloy development

- 3.6.1.3 Aluminum-magnesium hybrid experimentation

- 3.6.2 Emerging technologies

- 3.6.2.1 Carbon-fiber wheels

- 3.6.2.2 3D printing/additive manufacturing for prototyping

- 3.6.2.3 Smart wheels (tire pressure sensors, embedded electronics)

- 3.6.1 Current technological trends

- 3.7 Pricing Dynamics & Trends, 2021-2035

- 3.7.1 Pricing Landscape Overview

- 3.7.1.1 By region

- 3.7.1.2 By product

- 3.7.2 OEM Channel Pricing Dynamics

- 3.7.2.1 OEM Price Pressure Trends

- 3.7.2.2 Cost Pass-Through Mechanisms

- 3.7.2.3 Premium vs. Volume OEM Pricing

- 3.7.2.4 Flow-Formed Premium

- 3.7.2.5 Regional Pricing Differences (OEM)

- 3.7.3 Aftermarket Channel Pricing Dynamics

- 3.7.3.1 Aftermarket Pricing Power

- 3.7.3.2 E-Commerce Impact on Pricing

- 3.7.3.3 Replacement vs. Upgrade Pricing

- 3.7.3.4 Regional Pricing Differences (Aftermarket)

- 3.7.1 Pricing Landscape Overview

- 3.8 Patent analysis

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Pricing Analysis

- 3.10.1 By region

- 3.10.2 By Product

- 3.11 Cost analysis & total cost of ownership (TCO)

- 3.11.1 CapEx & OpEx comparison (Diesel vs Electric)

- 3.11.2 Purchase incentives & subsidies

- 3.11.3 Battery replacement costs

- 3.11.4 Maintenance & operational savings

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Investment & funding landscape

- 3.14.1 Public funding programs

- 3.14.2 Private investments & partnerships

- 3.14.3 Venture capital in e-truck startups

- 3.15 Fleet adoption & usage patterns

- 3.15.1 Fleet size & deployment

- 3.15.2 Urban vs long-haul usage

- 3.15.3 Fleet electrification roadmap

- 3.15.4 Total fleet cost savings

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 US

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Supplier Benchmarking, 2025

- 4.3.1 Manufacturing Footprint Comparison

- 4.3.2 Technology Capability Matrix (Casting/Flow Forming/Forging)

- 4.3.3 OEM vs. Aftermarket Revenue Mix

- 4.3.4 Capacity Utilization Rates

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New Product Launches

- 4.7.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Unit)

- 5.1 Key trends

- 5.2 Aluminum cast wheels

- 5.3 Aluminum forged wheels

- 5.4 Flow-formed aluminum wheels

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Unit)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 SUV

- 6.2.2 Sedan

- 6.2.3 Hatchback

- 6.3 Commercial vehicle

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

- 6.4 Off-road vehicle

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Unit)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Rim Size, 2022 - 2035 ($Bn, Unit)

- 8.1 Key trends

- 8.2 13-15 inches

- 8.3 16-18 inches

- 8.4 More than 19 inches

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 US

- 9.3 Northeast

- 9.3.1 Maine

- 9.3.2 Massachusetts

- 9.3.3 New Jersey

- 9.3.4 New York

- 9.3.5 Pennsylvania

- 9.4 Midwest

- 9.4.1 Illinois

- 9.4.2 Indiana

- 9.4.3 Michigan

- 9.4.4 Ohio

- 9.4.5 Wisconsin

- 9.4.6 Iowa

- 9.4.7 Kansas

- 9.4.8 Minnesota

- 9.4.9 Missouri

- 9.4.10 Nebraska

- 9.4.11 North Dakota

- 9.4.12 South Dakota

- 9.5 South

- 9.5.1 Florida

- 9.5.2 Georgia

- 9.5.3 North Carolina

- 9.5.4 South Carolina

- 9.5.5 Virginia

- 9.5.6 West Virginia

- 9.5.7 Alabama

- 9.5.8 Kentucky

- 9.5.9 Mississippi

- 9.5.10 Tennessee

- 9.5.11 Arkansas

- 9.5.12 Louisiana

- 9.5.13 Oklahoma

- 9.5.14 Texas

- 9.6 West

- 9.6.1 Arizona

- 9.6.2 Colorado

- 9.6.3 Idaho

- 9.6.4 Montana

- 9.6.5 Nevada

- 9.6.6 New Mexico

- 9.6.7 Utah

- 9.6.8 Wyoming

- 9.6.9 Alaska

- 9.6.10 California

- 9.6.11 Oregon

- 9.6.12 Washington

- 9.7 Canada

- 9.7.1 Ontario

- 9.7.2 Quebec

- 9.7.3 British Colombia

- 9.7.4 Alberta

- 9.7.5 Manitoba

- 9.7.6 Saskatchewan

- 9.7.7 Nova Scotia

- 9.7.8 New Brunswick

- 9.7.9 Newfoundland and Labrador

- 9.7.10 Prince Edward Island

- 9.8 Mexico

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Accuride

- 10.1.2 Alcoa Wheels

- 10.1.3 CITIC Dicastal

- 10.1.4 Enkei Wheels

- 10.1.5 Maxion Wheels

- 10.1.6 Ronal

- 10.1.7 Superior Industries International

- 10.1.8 Wanfeng

- 10.2 Regional Players

- 10.2.1 Central Motor Wheel of America

- 10.2.2 CM Wheels

- 10.2.3 Konig American

- 10.2.4 Prime Wheel

- 10.2.5 TSW Alloy Wheels

- 10.3 Emerging / Niche Players

- 10.3.1 Aluminum Wheels MFG

- 10.3.2 American Racing

- 10.3.3 BBS Wheels

- 10.3.4 Fuel Off-Road Wheels

- 10.3.5 Hands

- 10.3.6 Lizhong

- 10.3.7 Vision Wheel