PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959624

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959624

Military Tent and Shelter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

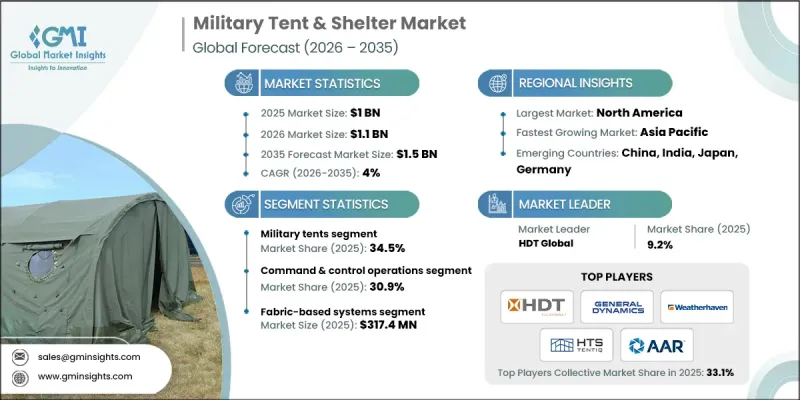

The Global Military Tent & Shelter Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 1.5 billion in 2035.

Market growth is driven by rising global defense budgets, which are increasing the procurement of military shelters. The demand for rapidly deployable solutions for expeditionary missions and technological advances in modular and smart shelters is further accelerating adoption. Additionally, there is growing interest in shelters that serve dual purposes for military operations and emergency response, broadening the market scope. Military forces and governments are increasingly prioritizing flexible, energy-efficient, and quick-deployment infrastructure to support operational readiness and humanitarian missions. The focus on dual-use scenarios emerged strongly around 2020 and continues to shape procurement strategies through 2030, as military and disaster-response agencies integrate logistics planning to improve operational resilience and crisis response capabilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $1.5 Billion |

| CAGR | 4% |

Military expenditure growth is fueling the demand for shelters, as governments allocate budgets to mobile infrastructure to support field operations and disaster relief. Advances in modular and smart shelter designs are enabling energy-efficient, rapid-deployment solutions for military missions, while dual-use applications for emergency response and humanitarian aid are expanding market potential. Containerized and medical shelters are gaining traction for their durability, adaptability, and ability to integrate systems such as communications, command centers, and healthcare infrastructure. These solutions allow for forward-deployed operations, semi-permanent bases, and advanced medical support in remote or conflict-affected areas, enhancing mission effectiveness and rapid-response capabilities.

The containerized shelters segment is expected to grow at a CAGR of 5.1% during 2026-2035. The increasing need for robust, long-lasting, and protective infrastructure for modern military operations is driving adoption. Containerized shelters offer superior insulation, durability, and the ability to integrate systems such as command centers, medical facilities, and communication networks. Their adaptability to harsh environments and suitability for semi-permanent and permanent use are supporting sustained market growth.

The medical and field hospital shelters segment is projected to grow at a CAGR of 5.3% through 2035. Rising investments in forward-deployed medical units, disaster response, and military healthcare readiness are fueling demand. These shelters are designed for emergency treatment, isolation wards, and surgical units in remote or high-risk locations. Humanitarian missions and rapid-response healthcare requirements are accelerating adoption, as these solutions provide quickly deployable and technologically advanced medical infrastructure for military and emergency use.

North America Military Tent & Shelter Market held a 39.9% share in 2025. Growth in the region is driven by rising defense budgets and the U.S. and Canadian militaries' emphasis on expeditionary infrastructure development. Modular and smart shelter systems offering climate control, power, and rapid-deployment capabilities are gaining traction. Investments by governments and defense contractors in next-generation deployable shelters for both military and relief operations continue to drive technological advancement. North America remains at the forefront of innovation, with military modernization projects, joint exercises, and operational needs sustaining market growth through 2035.

Key companies operating in the Global Military Tent & Shelter Market include HDT Global, Shelter Structures, Celina Military Shelters (Celina Tent, Inc.), Rekord Structures Company (RDS), UTS Systems LLC, AAR Mobility Systems, ADS Inc. (Advanced Deployable Systems), Losberger De Boer, Tentora / New Tents Manufacturing, ZTS TENTIQ GmbH, Weatherhaven, Outdoor Venture Corp, M. Schall, Veldeman, and other prominent players. Companies in the Military Tent & Shelter Market are strengthening their foothold through innovation, product diversification, and strategic collaborations. They are developing modular, smart, and energy-efficient shelters that cater to both military and dual-use applications. Partnerships with governments and defense contractors ensure early adoption and long-term contracts. Investments in rapid-deployment technologies, climate-controlled solutions, and integrated communication systems enhance operational relevance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Deployment type trends

- 2.2.3 Protection level trends

- 2.2.4 Material type trends

- 2.2.5 Mobility platform trends

- 2.2.6 Application trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global defense budgets increasing shelter procurements

- 3.2.1.2 Need for rapid deployment infrastructure in expeditionary missions

- 3.2.1.3 Technological advancements in modular and smart shelters

- 3.2.1.4 Dual-use shelters for military and emergency applications

- 3.2.1.5 Interoperability demand from joint/coalition military forces

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procurement, maintenance and lifecycle costs

- 3.2.2.2 Complex logistics in remote or harsh environments

- 3.2.3 Market opportunities

- 3.2.3.1 Custom modular designs for mission-specific needs

- 3.2.3.2 Integration of renewable energy systems into shelters

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Military tents

- 5.2.1 Troop accommodation tents

- 5.2.2 Lightweight combat tents

- 5.2.3 Rapid-deployment & inflatable tents

- 5.3 Soft-wall modular shelters

- 5.3.1 Frame-supported fabric shelters

- 5.3.2 Expandable soft-wall systems

- 5.4 Hard-wall deployable shelters

- 5.4.1 Rigid panel shelters

- 5.4.2 Insulated hard-wall shelters

- 5.5 Containerized shelters

- 5.5.1 ISO container shelters (20-ft / 40-ft)

- 5.5.2 Expandable containerized shelters

- 5.6 Vehicle-mounted & trailer-mounted shelters

- 5.6.1 Mobile command shelters

- 5.6.2 Transportable mission shelters

Chapter 6 Market Estimates and Forecast, By Deployment Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rapid-deployment

- 6.3 Semi-permanent

- 6.4 Relocatable / mobile

Chapter 7 Market Estimates and Forecast, By Protection Level, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Non-protected (environmental protection only)

- 7.3 Ballistic-resistant

- 7.4 Blast-resistant

- 7.5 CBRN / NBC-protected

- 7.6 EMP / EMI-shielded

- 7.7 Signature-Reduction

Chapter 8 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fabric-based

- 8.3 Metal-frame

- 8.4 Composite-based

- 8.5 Hybrid construction

Chapter 9 Market Estimates and Forecast, By Mobility Platform, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Ground-deployable (man-portable / air-portable)

- 9.3 Vehicle-mounted

- 9.4 Trailer-mounted

- 9.5 Container-transportable

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 10.1 Troop accommodation & base camps

- 10.2 Command & control (C2) operations

- 10.3 Medical & field hospitals

- 10.4 Maintenance, repair & logistics

- 10.5 Communication, radar & surveillance

- 10.6 Ammunition & equipment storage

- 10.7 Training & simulation support

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 HDT Global

- 12.1.2 General Dynamics Mission Systems

- 12.1.3 HTS TENTIQ GmbH

- 12.1.4 Losberger De Boer

- 12.1.5 AAR Mobility Systems

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 UTS Systems LLC

- 12.2.1.2 ADS Inc. (Advanced Deployable Systems)

- 12.2.1.3 Celina Military Shelters (Celina Tent, Inc.)

- 12.2.1.4 Outdoor Venture Corp

- 12.2.2 Europe

- 12.2.2.1 M. Schall

- 12.2.2.2 Rekord Structures Company (RDS)

- 12.2.2.3 Veldeman

- 12.2.2.4 Tentora / New Tents Manufacturing

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Weatherhaven

- 12.3.2 Shelter Structures