PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959627

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959627

3D NAND Flash Memory Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

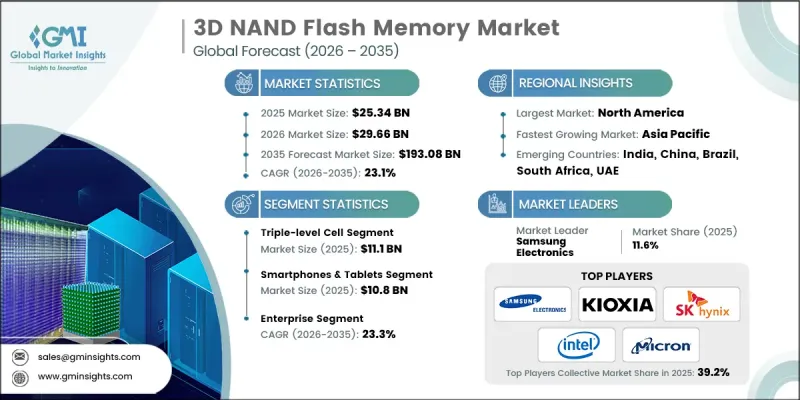

The Global 3D NAND Flash Memory Market was valued at USD 25.34 billion in 2025 and is estimated to grow at a CAGR of 23.1% to reach USD 193.08 billion by 2035.

Market momentum is driven by accelerating demand for high-capacity storage solutions across consumer electronics, rapid expansion of data centers and cloud computing infrastructure, and the growing influence of artificial intelligence, big data, and machine learning workloads. The increasing deployment of solid-state drives in enterprise and automotive environments is further strengthening market growth. Rising adoption of smartphones, IoT-enabled devices, and interconnected digital ecosystems continues to generate significant data volumes, reinforcing the need for scalable and high-density memory technologies. As digital transformation initiatives advance worldwide, storage infrastructure is becoming a strategic priority for governments and enterprises seeking to enhance economic development, digital sovereignty, and service efficiency. Investments in advanced data infrastructure and connected technologies are creating sustained demand for reliable, energy-efficient, and high-performance 3D NAND flash memory solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.34 Billion |

| Forecast Value | $193.08 Billion |

| CAGR | 23.1% |

Cloud infrastructure and data center development play a central role in supporting economic modernization and public digital services. Across Europe, including France, national digital strategies emphasize cloud adoption as a foundation for modern service delivery and secure data management. Government-backed initiatives highlight the strategic importance of data center deployment in strengthening digital ecosystems and supporting connected technologies. The continued expansion of IoT-enabled systems within national digital frameworks further increases demand for scalable and resilient flash memory solutions capable of handling rising data workloads.

The triple-level cell segment reached USD 11.1 billion in 2025. Triple-level cell technology enables high storage density at a comparatively lower cost, making it highly attractive for large-scale storage applications. Growing digital content consumption and data-intensive workloads are accelerating demand for TLC NAND solutions due to their scalability and cost efficiency. Manufacturers are expected to prioritize high-volume TLC production while incorporating advanced error correction and endurance optimization techniques to enhance reliability and long-term performance.

The smartphones and tablets segment generated USD 10.8 billion in 2025. Rising consumer demand for high-performance mobile devices capable of supporting advanced multimedia and data-intensive applications continues to increase the need for efficient and high-density NAND flash memory. Expanding mobile connectivity and digital service initiatives in developing economies are contributing to sustained device shipments, thereby driving demand for compact, power-efficient TLC and QLC NAND solutions optimized for mobile platforms.

North America 3D NAND Flash Memory Market accounted for 36.6% share in 2025. The region's leadership is supported by strong cloud adoption rates, ongoing data center expansion, and rising enterprise storage requirements. Artificial intelligence workloads and enterprise computing applications are generating significant demand for high-density NAND memory. Public sector digital transformation programs are also increasing storage infrastructure investments. A strong research and development ecosystem in semiconductor innovation hubs across the United States and Canada accelerates technological advancements. Growth in edge computing and industrial IoT deployments further reinforces the need for high-performance, energy-efficient NAND flash solutions tailored to enterprise and government applications.

Key companies operating in the Global 3D NAND Flash Memory Market include Samsung Electronics, SK Hynix, Micron Technology, Intel Corporation, Kioxia Corporation (formerly Toshiba Memory Corporation), Western Digital Corporation, SanDisk (a division of Western Digital), Nanya Technology Corporation, Powerchip Technology Corporation, YMTC (Yangtze Memory Technologies Co., Ltd.), Intel-Micron Flash Technologies (IMFT), XMC (Xiamen Xinxin Semiconductor Manufacturing Corporation), Macronix International, Transcend Information, ADATA Technology, Phison Electronics Corporation, Silicon Motion Technology Corporation, Netlist, Inc., SK Hynix System IC, Inc., and GigaDevice Semiconductor (Beijing) Inc. Companies in the Global 3D NAND Flash Memory Market are strengthening their competitive positioning through continuous technological innovation, capacity expansion, and strategic collaborations. Leading players are investing heavily in advanced node development and higher-layer NAND architectures to improve storage density and cost efficiency. Partnerships with cloud service providers and enterprise hardware manufacturers are helping secure long-term supply agreements. Firms are also expanding fabrication capabilities to address rising global demand while improving production yields. Research and development efforts focus on enhancing endurance, speed, and power efficiency to support data-intensive applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-capacity storage in consumer electronics

- 3.2.1.2 Expansion of data centers and cloud computing infrastructure

- 3.2.1.3 Growth of artificial intelligence, big data, and machine learning workloads

- 3.2.1.4 Increasing adoption of solid-state drives in enterprise and automotive applications

- 3.2.1.5 Growth in smartphones, IoT devices, and connected ecosystems

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High manufacturing complexity and capital-intensive fabrication processes

- 3.2.2.2 Yield management and reliability issues at higher layer counts

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Single-level cell

- 5.3 Multi-level cell

- 5.4 Triple-level cell

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Camera

- 6.3 Laptops and PCs

- 6.4 Smartphones & tablets

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Automotive

- 7.3 Consumer electronics

- 7.4 Enterprise

- 7.5 Healthcare

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Samsung Electronics

- 9.1.2 SK Hynix

- 9.1.3 Micron Technology

- 9.1.4 Intel Corporation

- 9.1.5 Kioxia Corporation

- 9.1.6 Western Digital Corporation

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 SanDisk (a division of Western Digital)

- 9.2.1.2 Intel-Micron Flash Technologies (IMFT)

- 9.2.1.3 Netlist, Inc.

- 9.2.2 Asia Pacific

- 9.2.2.1 Nanya Technology Corporation

- 9.2.2.2 Powerchip Technology Corporation

- 9.2.2.3 YMTC (Yangtze Memory Technologies Co., Ltd.)

- 9.2.2.4 XMC (Xiamen Xinxin Semiconductor Manufacturing Corporation)

- 9.2.2.5 Macronix International

- 9.2.2.6 Transcend Information

- 9.2.2.7 ADATA Technology

- 9.2.2.8 Phison Electronics Corporation

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Silicon Motion Technology Corporation

- 9.3.2 SK Hynix System IC, Inc.

- 9.3.3 GigaDevice Semiconductor (Beijing) Inc.