PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959632

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959632

Flow Meters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

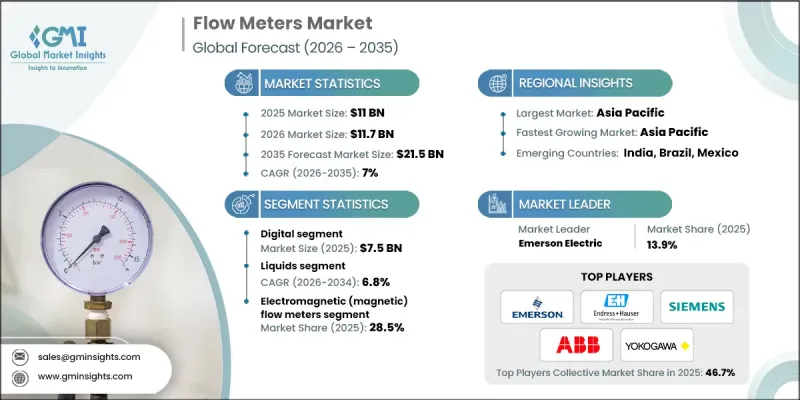

The Global Flow Meters Market was valued at USD 11 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 21.5 billion by 2035.

Market growth is driven by the steady expansion of process industries, rising infrastructure development investments, and increasing digital transformation across industrial operations. Growing global capacity in water and wastewater treatment facilities, along with rising demand for high-precision flow measurement in energy and chemical processing, continues to accelerate adoption. As industrial facilities modernize, accurate monitoring and process optimization have become operational priorities. Flow meters play a central role in ensuring compliance, efficiency, and safety across complex production environments. Increasing automation and the integration of intelligent monitoring systems are strengthening demand for advanced measurement technologies capable of delivering reliable real-time performance data across diverse industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11 Billion |

| Forecast Value | $21.5 Billion |

| CAGR | 7% |

The expansion of core sectors, including chemicals, energy, water management, and manufacturing, is significantly contributing to demand for flow metering solutions. Rising industrial output, new plant installations, and facility upgrades are creating consistent opportunities for measurement equipment deployment. The rapid increase in global industrial activity is leading to higher installation rates of flow meters to support monitoring, regulatory compliance, and process control. Urbanization, industrial growth, and stricter environmental standards are further driving investment in water and wastewater treatment infrastructure. Flow meters remain essential in maintaining operational accuracy and ensuring quality standards in these facilities. Additionally, industrial operators are increasingly adopting smart, IoT-enabled flow meters that enable predictive maintenance, cloud integration, SCADA connectivity, and digital twin system compatibility.

The digital segment reached USD 7.5 billion in 2025. The growing shift toward connected and automated industrial systems has strengthened demand for digital flow meters that provide precise, real-time measurement capabilities. Enhanced reliability, reduced maintenance requirements, and seamless integration with IoT platforms are major factors supporting segment dominance. Digital solutions enable advanced diagnostics and improved operational visibility, making them increasingly preferred across modern industrial environments.

The liquids segment is projected to grow at a CAGR of 6.8% during 2026-2035, supported by rising demand in water treatment, chemical processing, and food production industries. Accurate liquid flow measurement is critical for maintaining efficiency standards, process optimization, and regulatory compliance. The adoption of intelligent and IoT-enabled liquid flow meters is further contributing to segment growth by enhancing monitoring capabilities and operational transparency.

North America Flow Meters Market accounted for 26.8% share in 2025, supported by modernization initiatives targeting aging infrastructure across water management, energy, and power generation sectors. Increased deployment of smart and digital flow meters is helping organizations improve efficiency, meet regulatory standards, and optimize maintenance practices. Retrofit projects across established industrial facilities are contributing to rising demand. Broader adoption of IoT and cloud-based monitoring platforms is enhancing real-time data accessibility across multiple industries. Continued investment in industrial automation, particularly in high-precision manufacturing sectors, is strengthening demand for advanced flow measurement technologies such as Coriolis and ultrasonic systems, creating sustained opportunities across industrial and municipal markets.

Key companies operating in the Global Flow Meters Market include Emerson Electric Co, Endress+Hauser Group, ABB Ltd, Siemens AG, Honeywell International Inc, Yokogawa Electric Corporation, KROHNE Group, SICK AG, Badger Meter Inc, Brooks Instrument, Bronkhorst, Azbil Corporation, Hitachi High-Tech Corporation, OMEGA Engineering Inc., Sierra Instruments Inc, McCrometer Inc, McMillan Flow Products, Alicat Scientific Inc, Hontzsch GmbH and Co. KG, and Christian Burkert GmbH and Co. KG. Companies in the flow meters market are strengthening their competitive position through technological innovation, product diversification, and strategic partnerships. Many manufacturers are investing in smart sensor development, IoT-enabled platforms, and advanced diagnostics to enhance measurement accuracy and predictive maintenance capabilities. Expanding digital product portfolios allows vendors to meet evolving automation requirements. Firms are also focusing on customized solutions for sector-specific applications to strengthen customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Technology trends

- 2.2.3 Fluid type trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of process industries and infrastructure investments

- 3.2.1.2 Increasing automation and digitalization of industrial operations

- 3.2.1.3 Stringent regulatory requirements for custody transfer, safety, and emissions monitoring

- 3.2.1.4 Growing water and wastewater treatment capacity worldwide

- 3.2.1.5 Rising demand for high-accuracy measurement in energy and chemical processing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced flow meter technologies

- 3.2.2.2 Complex installation and calibration requirements in legacy and harsh operating environments

- 3.2.3 Market opportunities

- 3.2.3.1 Replacement of aging installed base with smart and digital flow meters

- 3.2.3.2 Rapid capacity expansion in semiconductor, LNG, and hydrogen infrastructure

- 3.2.3.3 Adoption of IoT-enabled and predictive maintenance-ready metering systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million and Units)

- 5.1 Key trends

- 5.2 Electromagnetic (magnetic) flow meters

- 5.3 Coriolis flow meters

- 5.4 Ultrasonic flow meters

- 5.5 Vortex flow meters

- 5.6 Differential pressure flow meters

- 5.7 Thermal mass flow meters

- 5.8 Turbine flow meters

- 5.9 Positive displacement flow meters

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million and Units)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital

Chapter 7 Market Estimates and Forecast, By Fluid Type, 2022 - 2035 (USD Million and Units)

- 7.1 Key trends

- 7.2 Liquids

- 7.3 Gases

- 7.4 Steam

- 7.5 Multiphase/slurry

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million and Units)

- 8.1 Key trends

- 8.2 Oil and gas

- 8.3 Chemical and petrochemical

- 8.4 Water and wastewater

- 8.5 Power generation and energy

- 8.6 Food and beverage

- 8.7 Pharmaceutical and biotechnology

- 8.8 Semiconductor and electronics manufacturing

- 8.9 Mining, minerals and metals

- 8.10 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 ABB Ltd

- 10.1.2 Emerson Electric Co

- 10.1.3 Honeywell International Inc

- 10.1.4 Siemens AG

- 10.1.5 Endress+Hauser Group

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Alicat Scientific Inc

- 10.2.1.2 Badger Meter Inc

- 10.2.1.3 McCrometer Inc

- 10.2.2 Asia Pacific

- 10.2.2.1 Azbil Corporation

- 10.2.2.2 Hitachi High-Tech Corporation

- 10.2.2.3 Yokogawa Electric Corporation

- 10.2.3 Europe

- 10.2.3.1 Christian Burkert GmbH and Co. KG

- 10.2.3.2 KROHNE Group

- 10.2.3.3 SICK AG

- 10.2.3.4 Hontzsch GmbH and Co. KG

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Brooks Instrument

- 10.3.2 McMillan Flow Products

- 10.3.3 OMEGA Engineering Inc.

- 10.3.4 Sierra Instruments Inc

- 10.3.5 Bronkhorst