PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959640

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959640

IoT Gateway Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

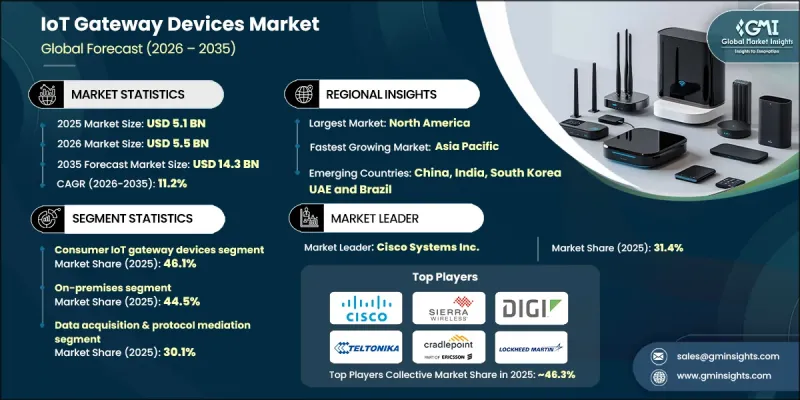

The Global IoT Gateway Devices Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 11.2% to reach USD 14.3 billion by 2035.

The market's growth is driven by the rapid increase in connected devices across industrial, commercial, and consumer applications, creating a growing demand for secure and reliable data aggregation between heterogeneous devices and cloud platforms. Organizations are increasingly focused on efficient device management, cybersecurity, and scalable IoT implementations, which further strengthens demand for gateway devices. Expansion of smart infrastructure projects such as smart cities, intelligent transportation systems, and advanced energy grids is fueling the adoption of IoT gateways. The shift toward edge computing to enable real-time analytics, low-latency decision-making, and AI-driven automation is driving gateways' role as a critical layer in urban mobility, industrial operations, and public services. Additionally, investments in 5G and LPWAN connectivity, coupled with edge AI analytics, are accelerating demand for IoT gateways capable of secure protocol translation and reliable data aggregation across distributed IoT endpoints.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 11.2% |

The consumer IoT gateway devices segment accounted for 46.1% share in 2025. Consumer gateways are highly sought after due to their cost efficiency, easy deployment, and compatibility with multiple wireless protocols, including Zigbee, Wi-Fi, Bluetooth, and Z-Wave. Growing adoption of smart homes, connected consumer electronics, and broadband penetration continues to drive the demand for these devices.

The on-premises segment held 44.5% share in 2025. Growth in this segment is largely driven by industrial users and the defense sector, where organizations require complete control over data, system access, and hardware-level security. Mission-critical applications depend on on-premises gateways for deterministic performance, data sovereignty, and low-latency processing. Companies are now focusing on designing hardened, cyber-resilient on-premises gateways capable of operating independently from external networks.

U.S. IoT Gateway Devices Market was valued at USD 1.7 billion in 2025. Market expansion is fueled by growth in smart factories, healthcare digitization, and energy grid modernization initiatives. Companies targeting the U.S. market are prioritizing edge computing capabilities, robust cybersecurity frameworks, and seamless integration with industrial automation systems to meet operational demands across diverse manufacturing and industrial sectors.

Prominent players operating in the Global IoT Gateway Devices Market include ADLINK Technology Inc., Advantech Co., Ltd., Cisco Systems, Inc., Cradlepoint, Inc. (Ericsson), Digi International Inc., Fujitsu Limited, Huawei Technologies Co., Ltd., Intel Corporation, Moxa Technologies, MultiTech Systems, Inc., Siemens AG, Sierra Wireless, Inc., Teltonika Networks, Toshiba Corporation, and Winmate, Inc. Key strategies adopted by companies in the IoT gateway devices market include continuous investment in research and development to enhance edge processing and AI capabilities, improving cybersecurity protocols to address data protection concerns, and expanding product compatibility across multiple IoT protocols. Companies are also forming strategic partnerships with cloud providers, telecom operators, and system integrators to ensure seamless device-to-cloud connectivity and secure data transmission. Geographic expansion into emerging markets, development of scalable modular gateway solutions, and offering customizable device management platforms are additional approaches to strengthen market presence and establish a competitive edge in a rapidly growing and technologically evolving industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Device Type trends

- 2.2.2 Functionality trends

- 2.2.3 Deployment Mode trends

- 2.2.4 Connectivity Technology trends

- 2.2.5 End-User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rapid expansion of IoT deployments across industries

- 3.3.1.2 Shift toward edge computing and real-time analytics

- 3.3.1.3 Government-led smart infrastructure and digital transformation initiatives

- 3.3.1.4 Advancements in connectivity technologies

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Data security & privacy concerns

- 3.3.2.2 High initial deployment and lifecycle management costs

- 3.3.3 Market opportunities

- 3.3.3.1 Integration of AI, machine learning, and advanced edge intelligence

- 3.3.3.2 Expansion of remote, rural, and non-terrestrial IoT connectivity

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Emerging Business Models

- 3.10 Compliance Requirements

- 3.11 Patent and IP analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Device Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Consumer IoT gateways

- 5.3 Commercial IoT gateways

- 5.4 Industrial IoT gateways

Chapter 6 Market Estimates and Forecast, By Functionality, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Data acquisition & protocol mediation

- 6.3 Edge processing & analytics

- 6.4 Data security/encryption

- 6.5 Device management

- 6.6 Connectivity bridging

Chapter 7 Market Estimates and Forecast, By Deployment Mode, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-Premises

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Connectivity Technology, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Wi-Fi

- 8.3 Bluetooth

- 8.4 ZigBee

- 8.5 Ethernet

- 8.6 Cellular

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Industrial & Manufacturing

- 9.3 Smart Infrastructure

- 9.3.1 Smart Cities

- 9.3.2 Smart Buildings

- 9.4 Energy & Utilities

- 9.5 Healthcare

- 9.6 Automotive & Transportation

- 9.7 Consumer Electronics

- 9.8 Retail & BFSI

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ADLINK Technology Inc.

- 11.2 Advantech Co., Ltd.

- 11.3 Cisco Systems, Inc.

- 11.4 Cradlepoint, Inc. (Ericsson)

- 11.5 Digi International Inc.

- 11.6 Fujitsu Limited

- 11.7 Huawei Technologies Co., Ltd.

- 11.8 Intel Corporation

- 11.9 Moxa Technologies

- 11.10 MultiTech Systems, Inc.

- 11.11 Siemens AG

- 11.12 Sierra Wireless, Inc.

- 11.13 Teltonika Networks

- 11.14 Toshiba Corporation

- 11.15 Winmate, Inc.