PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959642

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959642

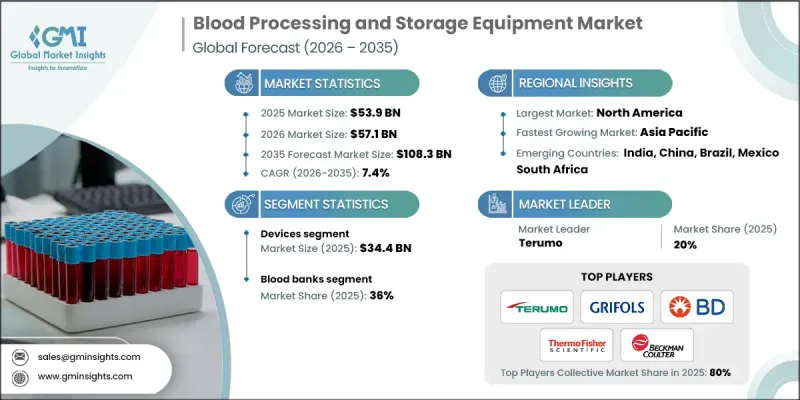

Blood Processing and Storage Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Blood Processing and Storage Equipment Market was valued at USD 53.9 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 108.3 billion by 2035.

Market expansion is supported by the growing burden of chronic diseases, continuous technological progress in blood management systems, and a rising number of trauma-related emergencies requiring transfusions. Increasing awareness surrounding voluntary blood donation is also playing a critical role in shaping industry growth. Government-led initiatives, healthcare campaigns, and nonprofit programs are strengthening donation networks worldwide, resulting in higher blood collection volumes. This surge in collection requires reliable infrastructure, including advanced refrigeration systems, plasma storage units, ultralow temperature freezers, and supporting consumables to maintain product integrity. Modern equipment enables healthcare facilities to preserve blood quality, streamline inventory management, and minimize product loss. As global healthcare systems prioritize transfusion safety and operational efficiency, investments in advanced blood processing and storage technologies are accelerating, reinforcing the development of scalable and compliant blood management frameworks across hospitals and collection centers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.9 Billion |

| Forecast Value | $108.3 Billion |

| CAGR | 7.4% |

Blood processing and storage equipment comprises specialized medical technologies designed to collect, separate, analyze, preserve, and manage blood and its components under tightly regulated temperature and safety parameters. These systems include centrifugation units, controlled refrigeration systems, deep freezers, filtration platforms, and related handling technologies that ensure sterility, prevent contamination, and maintain product viability for transfusion purposes. Precision temperature control and monitoring capabilities are essential to uphold clinical standards and extend shelf life while meeting regulatory compliance requirements.

The devices segment generated USD 34.4 billion in 2025, accounting for a 63.8% share. This category includes high-performance systems engineered for blood collection, separation, preservation, and monitoring. Equipment such as plasma storage units, blood bank refrigeration systems, laboratory-grade freezers, ultralow temperature systems, shock freezing units, blood grouping analyzers, warming systems, hematocrit centrifuges, and automated cell processors form the backbone of transfusion services. These devices safeguard blood quality throughout processing and storage cycles while meeting stringent safety benchmarks. Growing demand from hospitals, diagnostic laboratories, and blood collection centers continues to drive investments in technologically advanced and energy-efficient device platforms.

The blood banks segment held a 36% share in 2025, reflecting its central role in transfusion medicine. Blood banks function as primary hubs for the collection, testing, processing, storage, and distribution of blood products. To ensure safety and compliance, these facilities depend on advanced refrigeration systems, plasma preservation units, ultralow temperature storage solutions, and specialized centrifugation technologies. Rising surgical volumes, emergency care requirements, and chronic disease management programs are increasing demand for blood components, prompting blood banks to expand infrastructure and adopt next-generation storage systems capable of maintaining strict environmental control standards.

North America Blood Processing and Storage Equipment Market held 40.5% share in 2025, supported by its advanced healthcare infrastructure and rapid technology adoption. The region benefits from strong regulatory frameworks, well-established transfusion networks, and sustained investment in medical innovation. Continuous demand for transfusion therapies and chronic disease management programs requires dependable storage and processing systems. High-performance refrigeration units, ultralow temperature freezers, cell processing technologies, and supporting consumables are essential to maintain compliance and ensure patient safety across healthcare institutions.

Key companies operating in the Global Blood Processing and Storage Equipment Market include Thermo Fisher Scientific, Inc., Beckman Coulter, Inc., Grifols, Abbott Laboratories, Becton, Dickinson and Company, Terumo, F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories, Inc., Maco Pharma International GmbH, Thermogenesis Holdings, Inc., Immucor, Inc., Sigma Laborzentrifugen, Poly Medicure Ltd, and Biomerieux. Companies in the Blood Processing and Storage Equipment Market are strengthening their competitive positioning through innovation, regulatory compliance, and global expansion strategies. Leading manufacturers are investing in energy-efficient refrigeration systems, automated processing platforms, and digital monitoring solutions that enhance traceability and quality control. Strategic partnerships with hospitals and blood collection networks help expand distribution reach and ensure recurring demand. Firms are also prioritizing research and development to introduce advanced temperature monitoring technologies and integrated data management systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancement in blood processing and storage equipment

- 3.2.1.3 Surge in the number of road traffic accidents

- 3.2.1.4 Growing awareness regarding blood donation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with blood processing devices

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Increased applications in biotherapy and regenerative medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Devices

- 5.2.1 Plasma freezers

- 5.2.2 Blood bank refrigerators

- 5.2.3 Lab refrigerators

- 5.2.4 Lab freezers

- 5.2.5 Ultralow temperature freezers

- 5.2.6 Shock freezers

- 5.2.7 Grouping analyzers

- 5.2.8 Warmers

- 5.2.9 Hematocrit centrifuges

- 5.2.10 Cell processors

- 5.3 Consumables

- 5.3.1 Blood administration sets

- 5.3.2 Blood bags

- 5.3.3 Blood collection needles

- 5.3.4 Blood collection tube

- 5.3.5 Blood filters

- 5.3.6 Blood lancets

- 5.3.7 Blood grouping reagents

- 5.3.8 Blood coagulation reagents

- 5.3.9 Hematology reagents

- 5.3.10 Other consumables

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Blood banks

- 6.3 Diagnostic laboratories

- 6.4 Hospitals & clinics

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Beckman Coulter, Inc.

- 8.2 Thermogenesis Holdings, Inc.

- 8.3 Maco Pharma International GmbH

- 8.4 Immucor, Inc.

- 8.5 Becton, Dickinson and Company

- 8.6 Bio-Rad Laboratories, Inc.

- 8.7 Grifols, S.A.

- 8.8 Abbott Laboratories

- 8.9 Sigma Laborzentrifugen GmbH

- 8.10 Terumo BCT, Inc.

- 8.11 Poly Medicure Ltd

- 8.12 Thermo Fisher Scientific, Inc.

- 8.13 Biomerieux

- 8.14 F. Hoffmann-La Roche Ltd