PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959647

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959647

Aeroderivative Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

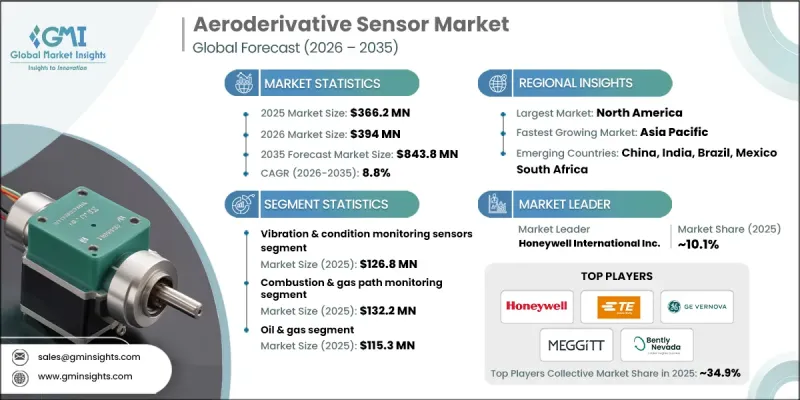

The Global Aeroderivative Sensor Market was valued at USD 366.2 million in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 843.8 million by 2035.

Market expansion is linked to the continued advancement of aerospace platforms across both defense and commercial aviation. Aeroderivative sensors are essential for monitoring, controlling, and optimizing aircraft systems, supporting safe and efficient operation under demanding conditions. As aircraft systems become more complex and performance-driven, demand is rising for sensors that deliver high accuracy, long-term reliability, and resilience in extreme operating environments. Industry focus on operational safety, performance optimization, and fuel efficiency is accelerating sensor adoption. Increased attention to regulatory compliance and automated aircraft operations is further strengthening demand. Ongoing technological progress is enabling sensors to become smaller, more precise, and more durable, supporting broader integration across next-generation aerospace platforms. These factors collectively position the aeroderivative sensor market for sustained growth as aviation systems continue to evolve toward higher efficiency and reliability standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $366.2 Million |

| Forecast Value | $843.8 Million |

| CAGR | 8.8% |

The vibration and condition monitoring sensors segment generated USD 126.8 million in 2025, representing one of the largest segments in the market. Their strong position reflects their importance in continuously assessing the health of rotating components and turbine systems. These sensors support early fault detection, minimize unplanned outages, and enhance overall system reliability while operating under high thermal and mechanical stress.

The combustion and gas path monitoring sensors segment accounted for USD 132.2 million in 2025, holding the largest share among application segments. Their importance stems from their role in tracking critical operating parameters that directly influence efficiency, output stability, fuel optimization, and emissions performance within aeroderivative systems.

North America Aeroderivative Sensor Market accounted for 39.4% share in 2025, maintaining its leading regional position. Market growth in the region is supported by rising adoption of intelligent turbine technologies, predictive maintenance practices, and digitally integrated monitoring systems. Investments in automation, operational safety, and compliance-driven monitoring continue to drive demand for advanced aeroderivative sensors.

Key companies operating in the Global Aeroderivative Sensor Market include Honeywell International Inc., GE Vernova / GE Aviation, TE Connectivity Ltd., Woodward Inc., AMETEK Inc., Meggitt SA, Bently Nevada (Baker Hughes), Kulite Semiconductor Products Inc., Kistler Instrument Corp., PCB Piezotronics Inc., Sensirion AG, Thermocoax Inc., Conax Technologies, Scanivalve Corporation, Unison LLC, Columbia Research Labs Inc., and Smith Systems Inc. Companies in the aeroderivative sensor market are reinforcing their market position through continuous investment in precision engineering, product reliability, and advanced manufacturing capabilities. Many players are focusing on developing sensors with enhanced durability and longer service life to meet stringent aerospace requirements. Strategic partnerships with aircraft and turbine system manufacturers are helping to integrate sensors at early design stages. Firms are also expanding customization capabilities to address specific operational needs. Emphasis on certification readiness, after-sales support, and lifecycle services is improving customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Sensor type trends

- 2.2.2 System Integration trends

- 2.2.3 Interface trends

- 2.2.4 Sales channel trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for advanced aerospace systems

- 3.2.1.2 Drone safety and regulations are driving demand for real-time aeroderivative sensors

- 3.2.1.3 Expansion of commercial aviation

- 3.2.1.4 Focus on maintenance and upgrades

- 3.2.1.5 Miniaturization & Advanced Sensor Technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Operating Costs and Harsh Operating Environments

- 3.2.2.2 Complex Certification, Integration, and Long Development Cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in offshore oil and gas projects

- 3.2.3.2 Rising need for fast-start and flexible power plants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Sustainability Measures

- 3.13 Consumer Sentiment Analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Sensor Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Temperature Sensor

- 5.3 Pressure Sensor

- 5.4 Vibration & Condition Monitoring Sensors

- 5.5 Speed & Position Sensors

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By System Integration Point, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Combustion & Gas Path Monitoring

- 6.3 Rotor & Shaft Monitoring

- 6.4 Fuel System Monitoring

- 6.5 Lubrication & Cooling System Monitoring

- 6.6 Emissions & Environmental Monitoring

Chapter 7 Market Estimates and Forecast, By Interface, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Analog Output Sensors

- 7.3 Digital Output Sensors

- 7.4 Wireless / Remote Sensors

Chapter 8 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Original Equipment Manufacturers (OEMs)

- 8.3 Aftermarket & MRO Service Providers

- 8.4 System Integrators

- 8.5 Direct End Users

Chapter 9 Market Estimates and Forecast, By End-use, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Power Generation

- 9.3 Oil & Gas

- 9.4 Marine & Naval Propulsion

- 9.5 Industrial & Manufacturing

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AMETEK, Inc.

- 11.2 Bently Nevada (Baker Hughes)

- 11.3 Columbia Research Labs, Inc.

- 11.4 Conax Technologies

- 11.5 GE Vernova / GE Aviation

- 11.6 Honeywell International Inc.

- 11.7 Kistler Instrument Corp.

- 11.8 Kulite Semiconductor Products, Inc.

- 11.9 Meggitt SA

- 11.10 PCB Piezotronics, Inc.

- 11.11 Scanivalve Corporation

- 11.12 Sensirion AG

- 11.13 Smith Systems, Inc.

- 11.14 TE Connectivity Ltd.

- 11.15 Thermocoax, Inc.

- 11.16 Unison LLC

- 11.17 Woodward, Inc.