PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959657

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959657

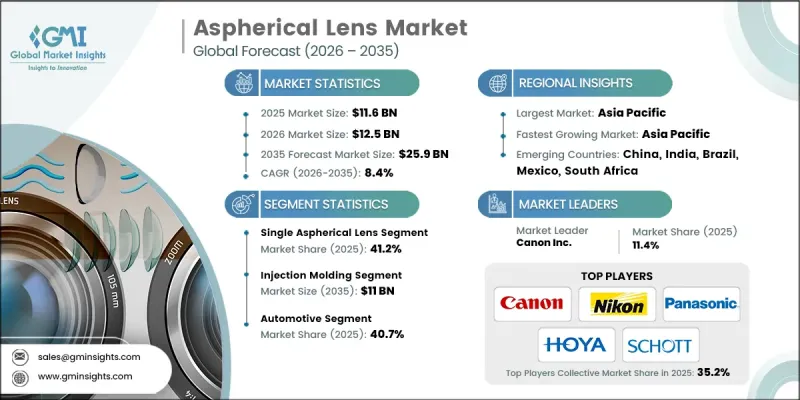

Aspherical Lens Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Aspherical Lens Market was valued at USD 11.6 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 25.9 billion by 2035.

Growth in this market is fueled by strategic partnerships, which allow companies to access new technologies, distribution networks, and customer segments, particularly in emerging areas such as automotive cameras and extended reality devices. Rising government initiatives to boost semiconductor manufacturing are also driving market expansion, with national subsidies, incentive programs, and fab expansion policies accelerating wafer consumption and promoting cost-efficient manufacturing practices like wafer reuse. The adoption of advanced driver assistance systems (ADAS) and LiDAR in vehicles is a critical driver, as high-precision aspherical lenses enhance camera and sensor performance by accurately focusing light and reducing optical distortions. Demand for intelligent, safe vehicles, coupled with regulatory support for ADAS, is further encouraging the adoption of advanced optical components in automotive applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.6 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 8.4% |

The single aspherical lens segment accounted for 41.2% share in 2025, reflecting its popularity due to low cost, simplicity, and ease of integration. Single lenses are widely used in consumer electronics, smartphones, compact cameras, and small optical devices where lightweight, precision optics are essential. Their compact design and performance advantages make them ideal for applications requiring high-resolution imaging in a small form factor.

The polishing & grinding segment was valued at USD 3.8 billion in 2025 and is expected to grow at a CAGR of 7.4% during 2026-2035. These processes are crucial for producing high-precision lenses used in demanding applications such as medical devices, scientific instruments, and aerospace systems. Technological advancements in automated polishing and computer-controlled grinding are enhancing lens quality, precision, and production efficiency, enabling manufacturers to meet the rising demand for premium optics.

North America Aspherical Lens Market held a 27.6% share in 2025, driven by robust adoption of aspherical lenses across consumer electronics, automotive, medical, and industrial applications. Early adoption of high-precision optics, coupled with technological innovation, is enabling companies to develop advanced coatings, miniaturized lenses, and compact optical systems. The growing use of cameras, image sensors, and optical devices in vehicles is further fueling demand for aspherical lenses in the region, making North America a key growth hub.

Leading companies operating in the Global Aspherical Lens Market include AGC Inc., ALPS ALPINE CO., LTD., Asahi Lite Optical Co., Ltd., Asia Optical Co., Inc., Asphericon GmbH, Avantier Inc., Calin Technology Co., Ltd., Canon Inc., Carl Zeiss AG, Edmund Optics India Private Limited, FUJIFILM Corporation, and Hoya Corporation. Key strategies adopted by companies to strengthen their Aspherical Lens Market presence include forming strategic alliances and partnerships to access emerging markets, advanced manufacturing technologies, and distribution channels. Companies are investing in R&D to improve lens quality, optical performance, miniaturization, and coating technologies. Expansion of production capacity, particularly for high-precision lenses used in automotive and industrial applications, is a priority. Firms are leveraging government incentives and subsidies to scale operations cost-effectively. Additionally, companies are focusing on product portfolio diversification, targeting new applications in automotive cameras, AR/VR devices, and scientific instruments, and collaborating with technology providers to integrate lenses into complex optical systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Lens type trends

- 2.2.2 Material type trends

- 2.2.3 Manufacturing technology trends

- 2.2.4 Wavelength range trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for compact and lightweight optical devices

- 3.2.1.2 Strategic collaborations and partnerships to expand market presence

- 3.2.1.3 Expansion of automotive ADAS and LiDAR systems

- 3.2.1.4 Rising demand for high-performance optical systems in industrial applications

- 3.2.1.5 Growth in surveillance and security systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and production costs

- 3.2.2.2 Limited availability of high-quality raw materials

- 3.2.3 Market opportunities

- 3.2.3.1 Advancements in miniaturized and high-precision optical components

- 3.2.3.2 Expansion in medical imaging and diagnostic equipment

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Lens Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Single aspherical lens

- 5.3 Bi-aspherical lens

- 5.4 Multi aspherical lens

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Glass

- 6.3 Plastic

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Manufacturing Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Injection molding

- 7.3 Polishing & grinding

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Wavelength Range, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Ultraviolet (<400 nm)

- 8.3 Visible (400-700 nm)

- 8.4 Near-infrared (700-1400 nm)

- 8.5 Shortwave/mid infrared (>1,400 nm)

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Consumer electronics

- 9.3.1 Digital cameras

- 9.3.2 Smartphones

- 9.3.3 Others

- 9.4 Healthcare & medical

- 9.5 Ophthalmic optics

- 9.6 Industrial & metrology

- 9.7 Aerospace & defense

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Canon Inc.

- 11.1.2 Nikon Corporation

- 11.1.3 Panasonic Holdings Corporation

- 11.1.4 Hoya Corporation

- 11.1.5 SCHOTT

- 11.1.6 Carl Zeiss AG

- 11.1.7 FUJIFILM Corporation

- 11.1.8 Konica Minolta, Inc.

- 11.1.9 KYOCERA Corporation

- 11.2 Regional Key Players

- 11.2.1 AGC Inc.

- 11.2.2 ALPS ALPINE CO., LTD.

- 11.2.3 Asahi Lite Optical Co., Ltd.

- 11.2.4 Asia Optical Co., Inc.

- 11.2.5 Shanghai Optics

- 11.2.6 SUMITA OPTICAL GLASS, Inc.

- 11.2.7 Tokai Optical Co. Ltd.

- 11.2.8 Edmund Optics India Private Limited

- 11.3 Niche Players / Disruptors

- 11.3.1 Asphericon GmbH

- 11.3.2 Avantier Inc.

- 11.3.3 Calin Technology Co. Ltd.

- 11.3.4 Hyperion Optics

- 11.3.5 Jenoptik AG

- 11.3.6 Knight Optical