PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959663

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959663

Military Embedded Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

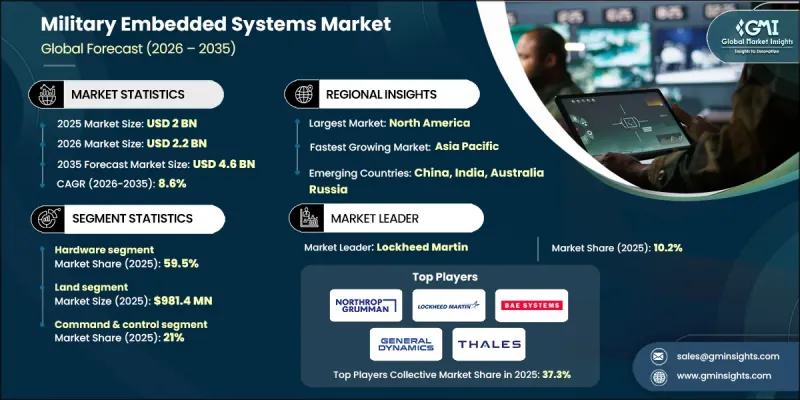

The Global Military Embedded Systems Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 4.6 billion by 2035.

Market expansion is driven by the growing requirement for rapid, real-time processing of mission-critical data in complex operational environments. Armed forces worldwide are increasingly investing in modern digital combat capabilities that rely on embedded computing for speed, accuracy, and operational resilience. Rising adoption of unmanned platforms, autonomous combat systems, and digitally integrated defense infrastructure is significantly increasing demand for advanced embedded solutions. Modernization initiatives across military forces are emphasizing data-centric warfare, artificial intelligence integration, and edge-based processing to enhance battlefield awareness and decision-making. Growing defense budgets among major military powers and allied nations are further supporting long-term investment in embedded technologies that improve responsiveness, survivability, and mission effectiveness across land, air, sea, and space domains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 8.6% |

Market momentum is reinforced by the rising need for embedded computing platforms capable of delivering fast and reliable situational awareness in dynamic combat conditions. Defense organizations are prioritizing data-driven command structures that reduce decision latency, improve sensor data integration, and enhance operational coordination. Embedded systems are becoming central to unmanned and autonomous platforms, enabling extended operational reach while minimizing personnel exposure. As militaries expand their reliance on autonomous and remotely operated systems, demand for rugged, secure, and high-performance embedded solutions continues to grow.

The software segment is expected to grow at a CAGR of 9.2% during 2026-2035. Growth is supported by increasing demand for artificial intelligence processing, edge analytics, and cybersecurity capabilities within defense systems. Software-driven embedded solutions offer adaptability, secure communications, predictive maintenance, and autonomous decision-making, making them essential to next-generation digital battlefield architectures.

The command-and-control segment accounted for 21% share in 2025, maintaining its leading position due to its strategic importance. Embedded systems play a critical role in managing operational coordination, intelligence processing, and secure communications across defense platforms. Real-time data handling and advanced analytics continue to drive sustained demand in this application area.

North America Military Embedded Systems Market held a share of 42.6% in 2025, supported by strong defense spending, advanced modernization programs, and rapid integration of intelligent processing technologies. Regional growth reflects increasing focus on autonomy, secure networks, and high-speed information processing across multi-domain military operations.

Key companies active in the Global Military Embedded Systems Market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, BAE Systems plc, Thales Group, Leonardo S.p.A., Saab AB, Rheinmetall AG, General Dynamics Corporation, Boeing Defense Space & Security, L3Harris Technologies Inc., Collins Aerospace, Elbit Systems Ltd., Curtiss-Wright Corporation, Honeywell International Inc., Intel Corporation, Renesas Corporation, Harris Corporation, and ABB Ltd. Companies operating in the Military Embedded Systems Market are strengthening their competitive position through sustained investment in research and development focused on artificial intelligence, edge computing, and secure system architectures. Many players are forming long-term defense contracts and strategic alliances to support large-scale modernization programs. Localization of production and compliance with military-grade certification standards are being prioritized to meet procurement requirements. Firms are also expanding modular and scalable embedded platforms to support multi-domain operations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Platform type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for real-time data processing in mission-critical military operations

- 3.2.1.2 Growing adoption of embedded systems in unmanned platforms and autonomous weapons

- 3.2.1.3 Increasing defense modernization and digital battlefield initiatives

- 3.2.1.4 Advancements in AI-enabled and edge-processing military electronics

- 3.2.1.5 Rising defense budgets across major military powers and allied nations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex certification and compliance requirements for military-grade embedded systems

- 3.2.2.2 Vulnerability to cyber threats and electronic warfare environments

- 3.2.3 Market opportunities

- 3.2.3.1 Growing integration of artificial intelligence in next-generation defense platforms

- 3.2.3.2 Rising adoption of embedded systems in space-based and missile defense programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense Budget Analysis

- 3.9 Global Defense Spending Trends

- 3.10 Regional Defense Budget Allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Key Defense Modernization Programs

- 3.12 Budget Forecast (2026-2035)

- 3.12.1 Impact on Industry Growth

- 3.12.2 Defense Budgets by Country

- 3.13 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.14 Risk Assessment and Management

- 3.15 Major Contract Awards (2022-2025)

- 3.16 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

Chapter 6 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Land

- 6.3 Airborne

- 6.4 Naval

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Communication & navigation

- 7.3 Command & control

- 7.4 Avionics

- 7.5 Electronic warfare

- 7.6 Radar

- 7.7 Weapon

- 7.8 Fire control systems

- 7.9 Wearable

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Chile

- 8.5.5 Columbia

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Egypt

- 8.6.5 Israel

- 8.6.6 Turkey

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 BAE Systems plc

- 9.1.2 Lockheed Martin Corporation

- 9.1.3 Northrop Grumman Corporation

- 9.1.4 Raytheon Technologies Corporation

- 9.1.5 General Dynamics Corporation

- 9.1.6 Thales Group

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Boeing Defense, Space & Security

- 9.2.1.2 L3Harris Technologies, Inc.

- 9.2.1.3 Honeywell International Inc.

- 9.2.1.4 Curtiss-Wright Corporation

- 9.2.1.5 Intel Corporation

- 9.2.2 Asia Pacific

- 9.2.2.1 Elbit Systems Ltd.

- 9.2.2.2 Renesas Corporation

- 9.2.3 Europe

- 9.2.3.1 Leonardo S.p.A.

- 9.2.3.2 Rheinmetall AG

- 9.2.3.3 Saab AB

- 9.2.1 North America