PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959665

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959665

Space Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

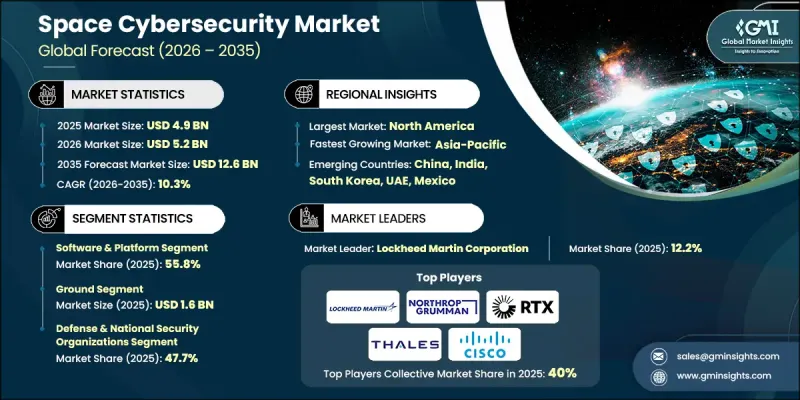

The Global Space Cybersecurity Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 12.6 billion by 2035.

Market expansion is driven by the growing number of cyberattacks targeting satellite command-and-control systems and the increasing reliance of defense organizations on space-based intelligence, surveillance, and reconnaissance capabilities. The transition toward software-defined satellites and cloud-enabled ground infrastructure is significantly elevating cybersecurity requirements across commercial, civil, and military space programs. As orbital assets become more interconnected and data-intensive, protecting mission-critical systems from intrusion, disruption, and data manipulation has become a strategic priority. The rapid deployment of low-earth orbit satellite constellations is reshaping security frameworks, as regulators and operators recognize heightened risks associated with network congestion and signal interference. Strengthening cybersecurity across the space supply chain is also transforming procurement models, particularly as outsourcing of satellite software, semiconductor components, and subsystems increases. Enhanced compliance standards and stricter oversight are improving trust, minimizing third-party vulnerabilities, and reinforcing system resilience against emerging digital threats.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 10.3% |

The software and platform segment accounted for 55.8% share in 2025, reflecting its central role in safeguarding satellite missions and ground-based infrastructure. Advanced cybersecurity platforms support encryption management, access authentication, anomaly detection, and continuous monitoring of orbital and terrestrial systems. Their scalability and compatibility with cloud-based architectures and software-defined satellites make them indispensable for proactive risk mitigation. As operators prioritize real-time threat intelligence and automated response mechanisms, investment in secure digital platforms continues to rise.

The communication link security segment is projected to grow at a CAGR of 11.3% during 2026-2035, fueled by increasing risks of signal interception, spoofing, and jamming across satellite-to-ground and inter-satellite connections. Expanding satellite bandwidth capabilities and dense orbital deployments are intensifying the need for advanced encryption protocols, multi-layer authentication, and anti-interference technologies. Ensuring secure data transmission across complex space communication networks has become a high-growth focus area for both government and commercial stakeholders.

North America Space Cybersecurity Market held a 48.3% share in 2025. Regional growth is supported by rising threats to satellite infrastructure, expanding dependence on space-based communications, and rapid deployment of advanced satellite constellations for defense and commercial purposes. Strong adoption of software-defined satellite systems and cloud-integrated ground stations is increasing exposure to cyber risks, prompting investment in zero-trust architectures, AI-driven threat analytics, and hardened satellite designs. Public and private sector collaboration in cybersecurity innovation further reinforces the region's leadership in this evolving market.

Key companies operating in the Global Space Cybersecurity Market include Lockheed Martin Corporation, Thales Group, Northrop Grumman Corporation, Airbus SE, L3Harris Technologies, Inc., RTX Corporation, Leonardo S.p.A., Booz Allen Hamilton, General Dynamics Corporation, Leidos Holdings, Inc., BAE Systems Plc, Cisco Systems, Inc., Fortinet, Inc., Check Point Software Technologies, CrowdStrike Holdings, Inc., CGI Group, Anduril Industries, Inc., Xage Security, Inc., and Nightwing Technologies. Companies in the Space Cybersecurity Market are strengthening their competitive positions by investing heavily in advanced encryption technologies, AI-powered threat detection, and post-quantum cryptography research to address future risks. Strategic partnerships with satellite manufacturers, defense agencies, and cloud service providers enable integrated security frameworks across orbital and ground systems. Firms are expanding managed security services and offering end-to-end cybersecurity platforms tailored for space missions. They are also focusing on compliance-driven solutions aligned with evolving regulatory mandates, while enhancing supply chain transparency to mitigate third-party risks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering type trends

- 2.2.2 Deployment trends

- 2.2.3 Application trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cyberattacks on satellite command-and-control systems

- 3.2.1.2 Proliferation of LEO satellite mega-constellations

- 3.2.1.3 Increased military reliance on space-based ISR assets

- 3.2.1.4 Integration of cloud-based ground station architectures

- 3.2.1.5 Commercialization of satellite communications and data services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited cybersecurity standards specific to space systems

- 3.2.2.2 Legacy satellites lacking onboard security upgrade capabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Zero-trust architectures for satellite-ground communications

- 3.2.3.2 AI-driven anomaly detection for space mission networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cryptographic modules

- 5.2.2 Secure boot & trusted execution

- 5.2.3 Anti-jamming & secure communication

- 5.3 Software & platform

- 5.3.1 Encryption & cryptography

- 5.3.2 Access control & authentication

- 5.3.3 Threat detection & monitoring

- 5.3.4 Command & control (C2) security

- 5.3.5 Cyber resilience & recovery platforms

- 5.4 Services

- 5.4.1 Managed services

- 5.4.2 Professional & consulting services

Chapter 6 Market Estimates and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Space segment (on-orbit) security

- 6.3 Ground segment security

- 6.4 Link segment (communication) security

- 6.5 User segment security

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Satellite communications

- 7.3 Earth observation & remote sensing

- 7.4 Navigation & positioning (PNT)

- 7.5 Space exploration & scientific missions

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Defense & national security organizations

- 8.3 Civil government space agencies & research institutions

- 8.4 Commercial space asset operators

- 8.5 Downstream service providers & system integrators

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Airbus SE

- 10.1.2 RTX Corporation

- 10.1.3 BAE Systems Plc

- 10.1.4 Lockheed Martin Corporation

- 10.1.5 Northrop Grumman Corporation

- 10.1.6 Thales Group

- 10.1.7 Leonardo S.p.A.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Booz Allen Hamilton

- 10.2.1.2 General Dynamics Corporation

- 10.2.1.3 L3Harris Technologies, Inc.

- 10.2.1.4 Leidos Holdings, Inc.

- 10.2.1.5 CGI Group

- 10.2.2 Asia Pacific

- 10.2.2.1 Cisco Systems, Inc.

- 10.2.3 Europe

- 10.2.3.1 Check Point Software Technologies

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Anduril Industries, Inc.

- 10.3.2 CrowdStrike Holdings, Inc.

- 10.3.3 Fortinet, Inc.

- 10.3.4 Nightwing Technologies

- 10.3.5 Xage Security, Inc.