PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982269

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982269

Shipment Tracking Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

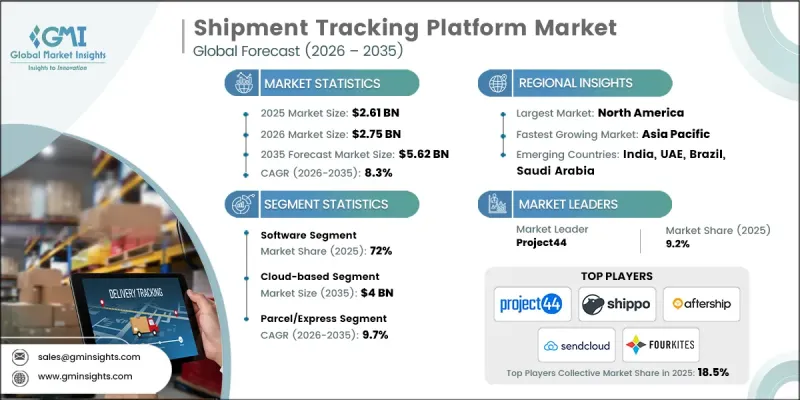

The Global Shipment Tracking Platform Market was valued at USD 2.61 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 5.62 billion by 2035.

The logistics sector is undergoing rapid digital transformation as advanced technologies redefine shipment visibility and operational efficiency. Modern tracking platforms are enabling real-time shipment monitoring, enhancing transparency across supply chains. Widespread adoption of IoT integration, cloud-based infrastructure, and real-time analytics is strengthening platform capabilities and improving service reliability. Logistics providers are increasingly deploying solutions that monitor not only shipment location but also environmental conditions such as temperature, humidity, and physical impact to mitigate risks and protect cargo integrity. GPS-enabled systems remain central to live tracking due to their precision and seamless compatibility with mobile interfaces. Advanced tracking tools are gaining traction across industries that require high levels of shipment oversight and operational accountability. The integration of predictive analytics and automated alerts is helping businesses streamline workflows and proactively address disruptions. Growing investor interest and continued capital inflows into tracking technology providers further underscore confidence in the long-term growth potential of the shipment tracking platform market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.61 Billion |

| Forecast Value | $5.62 Billion |

| CAGR | 8.3% |

In 2025, the software segment accounted for 72% share. Revenue generation is primarily driven by subscription-based SaaS models, API-driven pricing structures, and modular service tiers. These flexible modules support predictive estimated arrival insights, sustainability metrics, and collaborative supply chain tools, enabling customers to tailor solutions without introducing operational complexity.

The parcel and express segment is forecast to grow at a CAGR of 9.7% between 2026 and 2035. Strong expansion in global online retail and direct-to-consumer distribution channels is accelerating demand within this segment. High shipment volumes, compressed delivery timelines, and the need for frequent status updates have made real-time tracking a critical operational component. Advanced tracking platforms now play a central role in last-mile fulfillment and customer engagement strategies, as accurate delivery communication enhances buyer satisfaction, streamlines returns management and improves overall retailer performance.

U.S. Shipment Tracking Platform Market reached USD 837.9 million in 2025. Shipment visibility solutions have become essential across enterprises of all sizes. Large organizations remain primary adopters, while small and medium-sized businesses are rapidly transitioning toward cloud-based tracking platforms due to faster deployment timelines and lower infrastructure requirements. The ability to consolidate multiple carrier services into a unified system is improving operational coordination and strengthening the end-customer experience across the U.S. logistics landscape.

Key companies operating in the Global Shipment Tracking Platform Market include Project44, FourKites, AfterShip, ShipStation, Shippo, Narvar, Parcel Perform, Shippeo, ClickPost, and Sendcloud. Companies in the Shipment Tracking Platform Market are reinforcing their competitive position through continuous product innovation and strategic expansion. Providers are investing in AI-powered analytics, predictive delivery intelligence, and advanced API integrations to enhance platform functionality and scalability. Strategic partnerships with carriers, e-commerce marketplaces, and enterprise retailers are strengthening ecosystem connectivity and long-term contract pipelines. Firms are also expanding globally to capture emerging logistics markets while enhancing multilingual and multi-carrier capabilities. Subscription-based pricing models and modular platform architectures enable flexible adoption across business sizes.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Transportation Mode

- 2.2.5 Organization Size

- 2.2.6 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising e-commerce and online retail growth

- 3.2.1.2 Increasing demand for real-time shipment visibility

- 3.2.1.3 Growing adoption of IoT and smart logistics solutions

- 3.2.1.4 Need for supply chain optimization and efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data security and privacy concerns

- 3.2.2.2 Lack of standardized tracking protocols

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets with growing e-commerce penetration

- 3.2.3.2 Advancements in AI and predictive analytics

- 3.2.3.3 Expansion of last-mile delivery solutions

- 3.2.3.4 Strategic partnerships with logistics and courier companies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Motor Carrier Safety Administration (FMCSA)

- 3.4.1.2 U.S. Department of Transportation (USDOT)

- 3.4.1.3 Transportation Security Administration (TSA)

- 3.4.1.4 Canada Border Services Agency (CBSA)

- 3.4.1.5 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 European Union Agency for Cybersecurity (ENISA)

- 3.4.2.3 European Data Protection Board (EDPB)

- 3.4.2.4 International Road Transport Union (IRU - Europe)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Transport (China)

- 3.4.3.2 Ministry of Land, Infrastructure, Transport and Tourism (MLIT)

- 3.4.3.3 Directorate General of Civil Aviation (DGCA)

- 3.4.3.4 Australian Department of Infrastructure, Transport, Regional Development

- 3.4.4 Latin America

- 3.4.4.1 Secretariat of Infrastructure, Communications and Transport (SICT)

- 3.4.4.2 National Land Transport Agency (ANTT)

- 3.4.4.3 Ministry of Transport and Telecommunications (Chile)

- 3.4.4.4 Inter-American Committee on Ports (CIP - OAS)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council

- 3.4.5.2 Saudi Transport General Authority (TGA)

- 3.4.5.3 General Authority of Civil Aviation (GACA)

- 3.4.5.4 African Civil Aviation Commission (AFCAC)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Real-time GPS & telematics tracking

- 3.7.1.2 Cloud-based logistics platforms

- 3.7.1.3 Mobile tracking & driver apps

- 3.7.1.4 API Integration with supply chain systems

- 3.7.2 Emerging technologies

- 3.7.2.1 Internet of Things (IoT) sensor networks

- 3.7.2.2 Artificial Intelligence (AI) & Machine Learning (ML)

- 3.7.2.3 Blockchain for supply chain transparency

- 3.7.2.4 Digital Twin & predictive simulation models

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Infrastructure & implementation analysis

- 3.11.1 Connectivity infrastructure requirements

- 3.11.2 GPS & satellite technology limitations

- 3.11.3 Cloud vs. on-premise infrastructure

- 3.11.4 Implementation timelines & complexity

- 3.12 Impact of cybersecurity breaches on operations

- 3.12.1 Ransomware attacks on tracking systems

- 3.12.2 Data breach consequences & SLA impacts

- 3.12.3 OT/IT convergence vulnerabilities

- 3.12.4 IoT device security challenges

- 3.13 Last-mile delivery metrics & performance management

- 3.13.1 ETA prediction accuracy

- 3.13.2 Customer notification effectiveness

- 3.13.3 Failed delivery rate analysis

- 3.13.4 Last-mile cost per delivery

- 3.14 Case studies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Standalone tracking platforms

- 5.2.2 Integrated logistics/TMS platforms

- 5.2.3 Multi-carrier shipping platforms

- 5.2.4 Post-purchase experience platforms

- 5.2.5 Real-time transportation visibility platforms (RTTVP)

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment mode, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 Hybrid

- 6.4 On-premises

Chapter 7 Market Estimates & Forecast, By Transportation mode, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Multimodal

- 7.3 Road/ground transportation

- 7.3.1 FTL (Full Truckload) tracking

- 7.3.2 LTL (Less Than Truckload) tracking

- 7.3.3 Last-mile delivery tracking

- 7.4 Ocean/maritime

- 7.5 Air freight

- 7.6 Parcel/express

Chapter 8 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 SMEs

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Retail & e-commerce

- 9.3 Third-Party Logistics (3PL) & contract logistics

- 9.4 Manufacturing

- 9.5 Healthcare & pharmaceuticals

- 9.6 Automotive

- 9.7 Freight forwarding & shipping

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Czech Republic

- 10.3.7 Belgium

- 10.3.8 Russia

- 10.3.9 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 project44

- 11.1.2 FourKites

- 11.1.3 Shippeo

- 11.1.4 Oracle

- 11.1.5 SAP

- 11.1.6 Descartes Systems

- 11.1.7 Freightos

- 11.1.8 Trimble

- 11.2 Regional players

- 11.2.1 Shippo

- 11.2.2 LogiNext

- 11.2.3 Magaya

- 11.2.4 FreightPOP

- 11.2.5 Narvar

- 11.2.6 Easyship

- 11.2.7 AfterShip

- 11.2.8 ParcelLab

- 11.3 Emerging players

- 11.3.1 GPX

- 11.3.2 Shipup

- 11.3.3 ClickPost

- 11.3.4 Freightify