PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982275

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982275

Commercial Vehicle and Fleet Digital Twin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

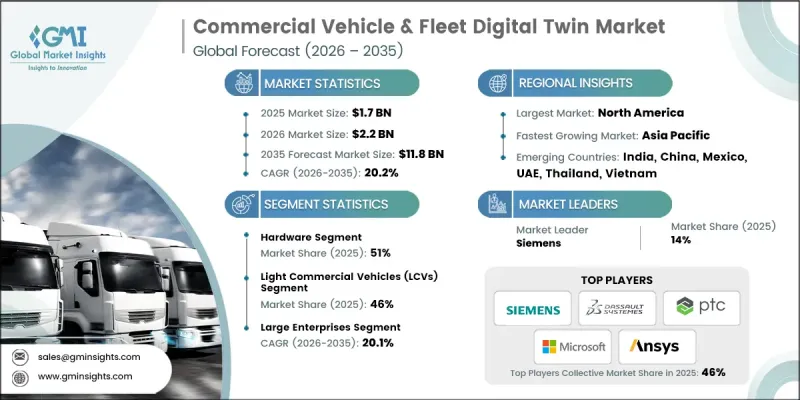

The Global Commercial Vehicle & Fleet Digital Twin Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 20.2% to reach USD 11.8 billion by 2035.

The market focuses on creating dynamic virtual replicas of commercial vehicles and entire fleet ecosystems, powered by connected sensors, artificial intelligence, advanced analytics, and scalable cloud environments. These digital frameworks allow OEMs, fleet owners, and transportation companies to monitor asset health in real time, improve lifecycle performance, and streamline operational efficiency. What began as simple vehicle data monitoring platforms has transformed into intelligent, simulation-driven systems capable of supporting predictive maintenance, utilization forecasting, and cost control strategies. Growing demand is being fueled by increasing digitization across logistics networks, stronger compliance requirements, and the rising complexity of fleet operations. Companies are investing heavily in cloud-based architecture to gain centralized visibility, minimize downtime, and enhance asset reliability. As fleets modernize and incorporate advanced technologies, digital twin platforms are becoming essential tools for risk mitigation, sustainability measurement, and long-term capital planning across global transportation networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 20.2% |

Modern digital twin platforms now extend far beyond basic monitoring capabilities, offering AI-enabled modeling environments that simulate large-scale operational conditions and performance variables. Fleet operators use these systems to evaluate efficiency strategies, asset utilization patterns, long-term maintenance forecasting, and total cost comparisons across diverse powertrain configurations. Advanced analytics engines also enable scenario-based route optimization, load distribution modeling, emissions analysis, and regulatory documentation management. Integration with connected vehicle technologies further strengthens safety validation processes and performance benchmarking under varied operating conditions. Market adoption continues to accelerate due to evolving regulatory frameworks and heightened expectations around operational transparency. The National Highway Traffic Safety Administration has expanded safety oversight and data reporting standards for commercial fleets deploying advanced technologies, prompting increased investment in digital infrastructure that supports real-time compliance tracking, vehicle diagnostics, and operational risk assessment.

The light commercial vehicles segment accounted for 46% share in 2025 and is forecast to grow at a CAGR of 20.2%. Vehicles within the gross weight range of 3.5 to 7.5 metric tons led adoption due to their high utilization rates and operational intensity. Demand within this segment is expanding rapidly as fleet operators seek enhanced scheduling precision, delivery performance tracking, driver analytics, and optimized asset deployment strategies. Digital twin solutions enable improved coordination, reduced downtime, and higher route efficiency within dense distribution environments.

The large enterprises segment held 66% share in 2025 and is projected to grow at a CAGR of 20.1% from 2026 to 2035. Major corporations are deploying digital twin ecosystems across extensive fleets while integrating them with enterprise platforms for resource planning, transportation management, warehouse coordination, and workforce administration. Hybrid cloud and edge computing models support advanced analytics processing, while centralized operational frameworks provide standardized visibility across geographically dispersed networks. These organizations rely on predictive intelligence for network optimization, regulatory reporting, and sustainability measurement initiatives aimed at reducing carbon intensity and strengthening environmental accountability.

United States Commercial Vehicle & Fleet Digital Twin Market generated USD 470 million in 2025 and is expected to grow at a CAGR of 19.5% between 2026 and 2035. The country maintains global leadership due to stringent emissions policies, accelerating fleet modernization programs, and widespread adoption of AI-driven fleet analytics. Long-haul transportation demand and infrastructure modernization are encouraging operators and OEMs to deploy advanced digital twin systems for continuous performance monitoring and predictive servicing. States such as Texas and Arizona are emerging as innovation corridors supported by expanding connected vehicle infrastructure, pilot-friendly regulatory frameworks, and concentrated engineering investments.

Key participants shaping the Global Commercial Vehicle & Fleet Digital Twin Market include Siemens, IBM, NVIDIA, Dassault Systems, ANSYS, Microsoft, Hexagon, PTC, General Electric, and Descartes Systems. These companies compete through advanced simulation platforms, cloud-native architectures, AI acceleration technologies, and deep integration capabilities tailored for fleet-scale deployments. Companies operating in the Commercial Vehicle & Fleet Digital Twin Market are strengthening their foothold through continuous platform innovation, ecosystem partnerships, and vertical integration strategies. Providers are enhancing AI-driven predictive analytics, expanding cloud interoperability, and investing in scalable digital architectures to accommodate growing fleet complexity. Strategic alliances with OEMs, telematics providers, and logistics platforms are enabling seamless data exchange and end-to-end visibility. Many vendors are also prioritizing cybersecurity, regulatory alignment, and sustainability reporting capabilities to meet enterprise requirements. Geographic expansion, targeted acquisitions, and industry-specific solution customization further reinforce competitive positioning.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Components

- 2.2.3 Vehicles

- 2.2.4 Enterprise Size

- 2.2.5 Deployment Mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of IoT & connected vehicle technology

- 3.2.1.2 Rising demand for predictive maintenance solutions

- 3.2.1.3 Regulatory push for fleet safety & emissions reduction

- 3.2.1.4 Growing focus on fleet operational efficiency

- 3.2.1.5 Accelerating electric vehicle fleet adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation costs

- 3.2.2.2 Data privacy & security concerns

- 3.2.2.3 Lack of standardization & interoperability

- 3.2.2.4 Limited availability of skilled workforce

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Integration with autonomous vehicle development

- 3.2.3.3 Scenario planning for fleet electrification

- 3.2.3.4 Development of industry-specific solutions

- 3.2.3.5 Monetization of fleet data analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal digital twin and fleet management regulations

- 3.4.1.2 Canada - Connected and autonomous fleet safety framework (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU ITS & national digital twin initiatives

- 3.4.2.2 UK- Post-Brexit ADAS and fleet digital twin guidance

- 3.4.2.3 France- National ADAS testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging ADAS & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 IoT & sensor technology

- 3.7.1.2 Edge computing infrastructure

- 3.7.1.3 Cloud computing platforms

- 3.7.1.4 AI & machine learning algorithms

- 3.7.2 Emerging technologies

- 3.7.2.1 5G & V2X integration

- 3.7.2.2 Digital thread architecture

- 3.7.2.3 Blockchain for data integrity

- 3.7.2.4 Augmented reality interfaces

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Patent filing trends (2021-2025)

- 3.8.2 Geographic distribution of patents

- 3.8.3 Top patent holders

- 3.8.4 Key technology clusters

- 3.9 Pricing analysis

- 3.9.1 Per-vehicle subscription model

- 3.9.2 Per-feature pricing

- 3.9.3 Usage-based pricing

- 3.9.4 Enterprise license agreements

- 3.9.5 Regional price variations

- 3.9.6 Price trends & forecasts

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Digital twin maturity model

- 3.12.1 Level 1: Basic connectivity & data collection

- 3.12.2 Level 2: Real-time monitoring & visualization

- 3.12.3 Level 3: Predictive analytics & simulation

- 3.12.4 Level 4: Autonomous optimization & control

- 3.12.5 Level 5: Ecosystem integration & cognitive twins

- 3.13 Industry maturity assessment by region

- 3.13.1 Interoperability & integration challenges

- 3.13.2 Legacy system integration

- 3.13.3 Multi-vendor platform compatibility

- 3.13.4 Data standardization issues

- 3.13.5 API & middleware requirements

- 3.13.6 Interoperability standards development

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Components, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 IoT sensors & telematics devices

- 5.2.2 Onboard computing units

- 5.2.3 GPS and connectivity modules

- 5.3 Software

- 5.3.1 Digital twin platform & simulation software

- 5.3.2 Fleet management and analytics software

- 5.3.3 Predictive maintenance & operational optimization software

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Light commercial vehicles (LCVs)

- 6.3 Medium commercial vehicles (MCVs)

- 6.4 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 Small & medium enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 On premises

- 8.3 Cloud-based

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Fleet operators & logistics companies

- 9.4 Tier 1 & Tier 2 suppliers

- 9.5 Automotive software & technology providers

- 9.6 Aftermarket & service centers

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ANSYS

- 11.1.2 Dassault Systemes

- 11.1.3 General Electric (GE Digital)

- 11.1.4 Hexagon

- 11.1.5 IBM

- 11.1.6 Microsoft

- 11.1.7 PTC

- 11.1.8 Siemens

- 11.2 Regional Players

- 11.2.1 Descartes Systems

- 11.2.2 Daimler Truck

- 11.2.3 Geotab

- 11.2.4 NVIDIA

- 11.2.5 Robert Bosch

- 11.2.6 Motive (KeepTruckin)

- 11.2.7 Samsara

- 11.2.8 SAP

- 11.2.9 Tata Consultancy Services

- 11.2.10 Trimble

- 11.2.11 Volvo

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 Altair Engineering

- 11.3.2 Intangles