PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982277

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982277

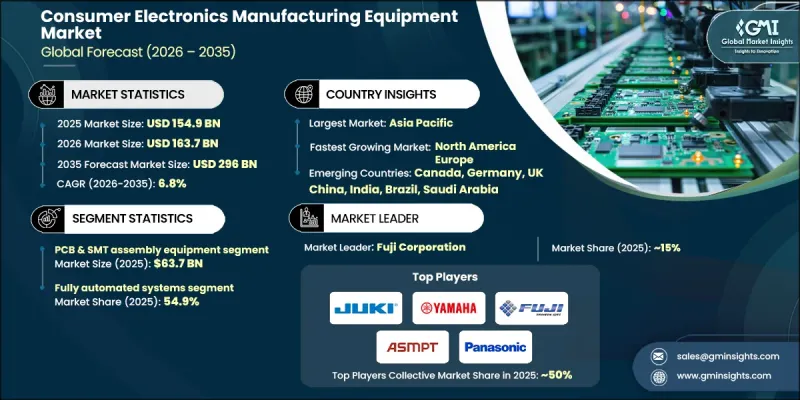

Consumer Electronics Manufacturing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Consumer Electronics Manufacturing Equipment Market was valued at USD 154.9 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 296 billion by 2035.

Market growth is driven by rising expectations for compact, high-performance electronic products that require increasingly advanced production capabilities. Device manufacturers are prioritizing precision engineering, high-density integration, and advanced fabrication processes to meet performance and design demands. This shift is accelerating investments in next-generation assembly, inspection, and semiconductor production systems capable of handling complex architectures and miniaturized components. Growing connectivity trends and next-wave communication technologies are also contributing to higher production volumes and more intricate component requirements. As electronics become more sophisticated, manufacturers are deploying high-throughput, automated solutions to maintain quality, improve efficiency, and scale output. The transition toward advanced packaging techniques and multilayer board designs further supports demand for cutting-edge production tools. Overall, the market is benefiting from continuous innovation in manufacturing processes, rising global electronics consumption, and the increasing complexity of integrated systems."

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $154.9 Billion |

| Forecast Value | $296 Billion |

| CAGR | 6.8% |

The PCB and SMT assembly equipment segment generated USD 63.7 billion in 2025 and is forecast to grow at a CAGR of 6.5% from 2026 to 2035. Equipment upgrades are being fueled by widespread adoption of automation, robotics integration, and AI-powered inspection technologies that enhance productivity and improve yield rates. Manufacturers are implementing intelligent defect recognition, predictive servicing models, live process tracking, and precision rework capabilities to reduce downtime and improve operational efficiency. These advancements are encouraging the continuous modernization of PCB and SMT production lines.

The fully automated systems segment accounted for 54.9% share in 2025 and is projected to grow at a CAGR of 7% between 2026 and 2035. Companies are embedding AI-driven analytics, robotic handling systems, IoT-enabled monitoring devices, digital simulation tools, and predictive maintenance platforms into manufacturing environments to optimize throughput and minimize errors. Increasing global competition, higher labor expenses, and the technical challenges associated with miniaturized and complex electronic assemblies are accelerating the transition toward comprehensive automation solutions.

U.S. Consumer Electronics Manufacturing Equipment Market reached USD 29.1 billion in 2025 and is expected to grow at a CAGR of 6.2% from 2026 to 2035. Domestic production capacity is expanding due to heightened demand for advanced semiconductor technologies, data infrastructure components, and AI-focused hardware systems. Public policy initiatives supporting onshore manufacturing, along with large-scale capital investments by leading chip producers, are reinforcing local supply chains. Manufacturing facilities across the country are increasingly adopting AI-enabled quality systems, robotics, smart factory frameworks, and predictive analytics platforms, thereby strengthening demand for advanced SMT, semiconductor fabrication, testing, and automation equipment.

Key companies operating in the Global Consumer Electronics Manufacturing Equipment Market include KLA Corporation, FANUC Corporation, ABB Robotics, Yaskawa Electric, KUKA AG, Yamaha Motor Corporation, JUKI Corporation, Bosch Rexroth AG, Mycronic AB, Omron Corporation, Fuji Corporation, THK Co., Ltd., The Timken Company, Nordson Corporation, NSK Ltd., Saki Corporation, and Hiwin Technologies Corporation. Companies competing in the Global Consumer Electronics Manufacturing Equipment Market are reinforcing their position through continuous innovation and strategic investment. Many firms are expanding research and development capabilities to introduce high-precision, AI-integrated, and automation-centric equipment that enhances production scalability and reliability. Strategic partnerships with semiconductor manufacturers and electronics producers are strengthening long-term supply agreements and recurring revenue streams. Organizations are also focusing on geographic expansion, particularly in regions experiencing semiconductor capacity growth. Investments in digital manufacturing ecosystems, predictive maintenance platforms, and smart factory integration are improving customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Technology

- 2.2.4 Motion component

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for miniaturized and high-performance electronic devices

- 3.2.1.2 Expansion of IoT, 5G, and connected technologies

- 3.2.1.3 Growth of automotive electronics and electrification (EVs)

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions and component shortages

- 3.2.2.2 Increasing technological complexity and faster product cycles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 PCB & SMT assembly equipment

- 5.3 Testing & inspection equipment

- 5.4 Component handling & storage systems

- 5.5 Assembly & integration systems

- 5.6 Coating & dispensing equipment

- 5.7 Cleaning & surface preparation equipment

- 5.8 Marking & labelling equipment

- 5.9 Cutting & singulation equipment

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Fully automated systems

- 6.3 Semi-automated systems

- 6.4 Manual/basic systems

Chapter 7 Market Estimates & Forecast, By Motion component, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Linear guides

- 7.3 Telescopic rails

- 7.4 Linear actuators

- 7.5 Ball screws

- 7.6 Integrated motion systems

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Consumer electronics manufacturers

- 8.3 OSAT (outsourced semiconductor assembly & test) providers

- 8.4 Telecommunications electronics

- 8.5 Automotive electronics

- 8.6 Industrial and IoT electronics

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ABB Robotics

- 11.2 Bosch Rexroth AG

- 11.3 FANUC Corporation

- 11.4 Fuji Corporation

- 11.5 Hiwin Technologies Corporation

- 11.6 JUKI Corporation

- 11.7 KLA Corporation

- 11.8 KUKA AG

- 11.9 Mycronic AB

- 11.10 Nordson Corporation

- 11.11 NSK Ltd.

- 11.12 Omron Corporation

- 11.13 Saki Corporation

- 11.14 The Timken Company

- 11.15 THK Co., Ltd.

- 11.16 Yamaha Motor Corporation

- 11.17 Yaskawa Electric