PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982291

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982291

Holographic Data Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

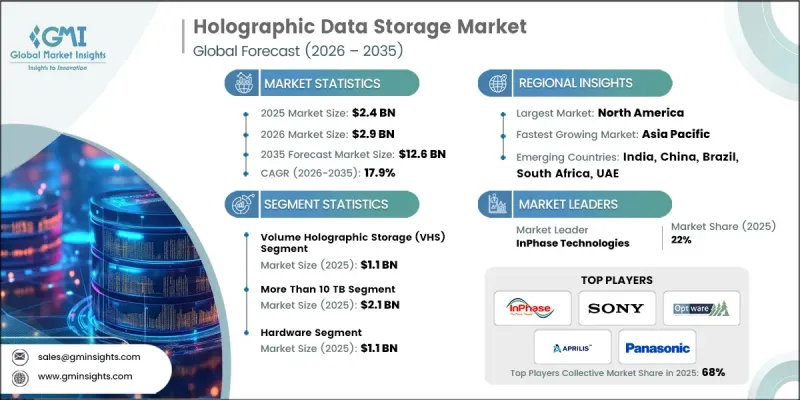

The Global Holographic Data Storage Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 17.9% to reach USD 12.6 billion by 2035.

The holographic data storage industry is gaining strong momentum as organizations seek storage technologies capable of delivering exceptional density and scalability beyond conventional systems. Growing volumes of digital information, fueled by cloud computing expansion and data-intensive applications, are accelerating the need for next-generation storage platforms. Enterprises and institutions are increasingly prioritizing secure, long-term archival solutions that ensure durability and data integrity over extended periods. Rising demand for rapid data access and high-speed processing capabilities is further strengthening market adoption. Industries requiring secure, high-capacity environments are turning to holographic systems to manage complex digital workloads. The ability of holographic storage to handle exponential data growth while supporting efficient retrieval positions as a transformative solution in modern digital infrastructure. As traditional storage technologies approach physical and performance limitations, holographic data storage is emerging as a compelling alternative for high-density, future-ready storage ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 17.9% |

A defining strength of holographic data storage lies in its capacity to record information throughout the full volume of the storage medium rather than restricting it to surface-level layers. This volumetric approach enables dramatically higher storage densities and enhances parallel data retrieval performance. Public and private research bodies are exploring advanced storage frameworks that move beyond conventional disk-based systems to support future data environments. Continuous innovation efforts highlight the technology's potential to address the scaling challenges associated with rapidly expanding digital ecosystems. As data infrastructure grows in complexity, institutions are investing in advanced storage paradigms capable of delivering endurance, efficiency, and long-term scalability.

The volume holographic storage (VHS) segment generated USD 1.1 billion in 2025. VHS technology stands out due to its capability to embed data across the entire depth of the recording material, enabling ultra-high storage density and efficient parallel data processing. Growing requirements for secure, durable, and space-efficient archival systems are accelerating VHS adoption across enterprise and institutional environments. Its ability to maintain data integrity while reducing physical storage space enhances its appeal. Manufacturers are encouraged to improve photopolymer material durability and optimize read/write precision to strengthen VHS positioning as a competitive alternative to legacy archival technologies.

The more than 10 TB capacity segment accounted for USD 2.1 billion in 2025. Demand within this segment is driven by large-scale digital infrastructures that require ultra-high-capacity solutions capable of preserving data securely over extended durations. Increasing emphasis on energy-efficient archival systems is accelerating investment in high-capacity holographic platforms that lower operational costs and minimize infrastructure footprints. Industry participants are advised to focus on scalable system architectures and strategic collaborations with large institutional stakeholders to accelerate the commercialization of mission-critical, ultra-high-capacity holographic storage solutions.

North America Holographic Data Storage Market held a 34.3% share in 2025. Regional leadership is supported by a strong research and innovation environment, advanced digital infrastructure, and early adoption of emerging storage technologies. Ongoing digital transformation initiatives and emphasis on energy-efficient archival frameworks continue to stimulate demand. As large-scale data operations expand, holographic storage is increasingly viewed as a strategic enabler for resilient and scalable digital ecosystems. Companies are encouraged to deepen research collaborations and align product development with institutional requirements to capitalize on growth opportunities within the region.

Key participants in the Global Holographic Data Storage Market include InPhase Technologies, Optware Corporation, Aprilis Inc., Akonia Holographics, Zebra Imaging, Holographic Versatile Disc (HVD) Alliance, Sony Corporation, Panasonic Holdings Corporation, Samsung Electronics, Fujifilm Holdings Corporation, Hitachi, Ltd., General Electric (GE Research), IBM Corporation, Microsoft Corporation, Toshiba Corporation, Intel Corporation, Western Digital Corporation, and Seagate Technology. Companies competing in the Holographic Data Storage Market are reinforcing their market presence through continuous innovation and strategic alliances. Industry leaders are prioritizing research investments to enhance media stability, improve data transfer speeds, and increase storage density. Partnerships with enterprise data infrastructure providers and institutional organizations are accelerating commercialization efforts. Firms are also focusing on scalable product architectures to address large-capacity storage requirements. Strengthening intellectual property portfolios and advancing material science capabilities remain central strategies for differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Storage capacity trends

- 2.2.3 Component trends

- 2.2.4 Application trends

- 2.2.5 End-user industry trends

- 2.2.6 Material trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High data storage density and capacity compared to traditional storage solutions

- 3.2.1.2 Rapid growth in cloud computing and big data applications

- 3.2.1.3 Increasing demand for secure and long-term archival storage

- 3.2.1.4 Rising need for high-speed data retrieval and processing

- 3.2.1.5 Growing adoption in defense, healthcare, and multimedia industries

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High cost of implementation and maintenance

- 3.2.2.2 Complexity of technology integration with existing IT infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Volume Holographic Storage (VHS)

- 5.3 Surface Holographic Storage (SHS)

- 5.4 Hybrid Holographic Storage

Chapter 6 Market Estimates and Forecast, By Storage Capacity, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Less than 1 TB

- 6.3 1 TB to 10 TB

- 6.4 More than 10 TB

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 8.1 Key Trends

- 8.2 Photopolymers

- 8.3 Photorefractive Crystals

- 8.4 Silicon-based Storage

- 8.5 Polymer Thin Films

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Enterprise Data Storage & Data Centers

- 9.3 Archival Storage & Backup

- 9.4 Real-Time High-Volume Data Access

- 9.5 Critical Secure Storage

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 10.1 Key Trends

- 10.2 IT & Telecommunications

- 10.3 Banking, Financial Services & Insurance (BFSI)

- 10.4 Healthcare

- 10.5 Media & Entertainment

- 10.6 Government

- 10.7 Defense & Aerospace

- 10.8 Others (Education, Research Institutions, etc.)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Sony Corporation

- 12.1.2 Panasonic Holdings Corporation

- 12.1.3 Samsung Electronics

- 12.1.4 Hitachi, Ltd.

- 12.1.5 IBM Corporation

- 12.1.6 Microsoft Corporation

- 12.1.7 Intel Corporation

- 12.1.8 Toshiba Corporation

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Western Digital Corporation

- 12.2.1.2 Seagate Technology

- 12.2.1.3 InPhase Technologies

- 12.2.1.4 Optware Corporation

- 12.2.1.5 Aprilis Inc.

- 12.2.2 Europe

- 12.2.2.1 Holographic Versatile Disc (HVD) Alliance

- 12.2.3 Asia Pacific

- 12.2.3.1 Fujifilm Holdings Corporation

- 12.2.1 North America

- 12.3 Niche / Disruptors

- 12.3.1 Akonia Holographics

- 12.3.2 Zebra Imaging