PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982296

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982296

Automotive Brake Pads Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

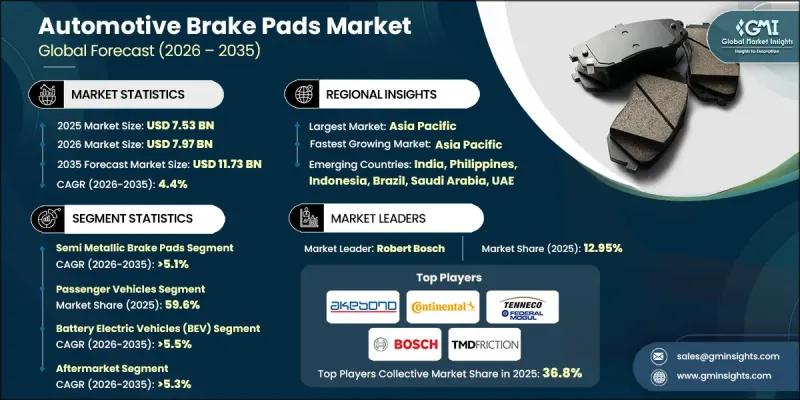

The Global Automotive Brake Pads Market was valued at USD 7.53 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 11.73 billion by 2035.

The ongoing evolution of vehicle manufacturing, tightening safety mandates, and rapid electrification trends are redefining brake pads from basic replacement parts into essential safety and performance components. Brake pads are now closely aligned with vehicle efficiency standards, emission control targets, and advanced braking technologies across passenger cars, commercial fleets, and electric vehicles. A growing global vehicle fleet, rising average vehicle age, and longer ownership cycles are reinforcing consistent aftermarket demand. Consumers and fleet managers are increasingly prioritizing durability, reduced noise levels, lower brake dust emissions, and compatibility with electronic braking architectures. This shift reflects a lifecycle-focused maintenance approach that emphasizes braking reliability, safety assurance, and optimized total cost of ownership rather than solely initial purchase price. At the same time, advancements in friction material engineering are reshaping product differentiation and long-term competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.53 Billion |

| Forecast Value | $11.73 Billion |

| CAGR | 4.4% |

Innovation in friction materials continues to transform the automotive brake pads industry. Semi-metallic, low-metallic NAO, ceramic, and copper-free formulations are gaining wider adoption as environmental policies become more stringent, particularly across developed economies. Manufacturers are investing in lightweight composite structures, enhanced thermal stability compounds, and low-emission friction technologies to comply with regulatory standards while sustaining braking performance under demanding operating conditions. As a result, brake pads are increasingly engineered as high-performance components rather than standardized wear items.

The semi-metallic brake pads segment held 36.4% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. Their strong market position is supported by superior durability, efficient heat dissipation, and consistent braking output under high-load and high-speed environments. These pads, manufactured using blended metallic content combined with friction modifiers, deliver reliable stopping power and cost efficiency, making them suitable across a broad range of vehicle categories operating in intensive driving conditions.

The passenger vehicles segment accounted for 59.6% share in 2025 and is expected to grow at a CAGR of 3.9% between 2026 and 2035. The dominance of this segment is driven by the scale of global passenger car ownership and recurring replacement cycles linked to routine maintenance. High vehicle utilization rates, urban traffic congestion, and extended commuting distances contribute to accelerated brake wear, sustaining both OEM and aftermarket demand. Growing disposable incomes and expanding vehicle ownership across emerging economies are further strengthening long-term growth prospects.

China Automotive Brake Pads Market held 65.52% share, generating USD 2.1 billion in 2025. The country's strong performance is supported by its extensive vehicle base and consistent automotive production output. Expanding urban infrastructure, rising middle-income households, and increasing freight movement are elevating vehicle usage intensity, which shortens brake replacement intervals. As a leading global automotive manufacturing center, China also drives substantial OEM demand for friction components. Domestic producers benefit from integrated supply networks, competitive production costs, and robust export capabilities, enabling strong participation in both domestic and international markets.

Key companies operating in the Global Automotive Brake Pads Market include Brembo, Robert Bosch, Akebono Brake Industry, ZF Friedrichshafen, Continental, Tenneco, Hitachi Astemo, TMD Friction, Delphi Technologies, and Knorr-Bremse. Companies in the automotive brake pads market are reinforcing their competitive position through material innovation, strategic OEM partnerships, and global distribution expansion. Manufacturers are investing in advanced friction formulations, lightweight designs, and environmentally compliant compounds to meet evolving emission and safety standards. Strengthening long-term supply agreements with automakers ensures stable revenue streams and early integration into new vehicle platforms. Many players are expanding aftermarket networks to capture recurring replacement demand while enhancing brand visibility. Capacity expansion in high-growth regions improves cost efficiency and supply responsiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Vehicle

- 2.2.4 Sales Channel

- 2.2.5 Propulsion

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global vehicle parc and aging passenger car fleet

- 3.2.1.2 Surge in stringent vehicle safety and braking performance regulations

- 3.2.1.3 Increase in demand for premium ceramic and low-metallic brake pads

- 3.2.1.4 Rise in commercial vehicle utilization driven by logistics and e-commerce expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Impact of Regenerative Braking in EVs

- 3.2.2.2 Raw Material Price Volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in development of EV-specific and corrosion-resistant brake pad formulations

- 3.2.3.2 Surge in demand for copper-free and environmentally compliant brake materials

- 3.2.3.3 Increase in vehicle ownership across emerging economies

- 3.2.3.4 Rise in integration of brake systems with ADAS and electronic stability technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 North America

- 3.3.1.1 U.S.: Copper-Free Brake Pad Regulations (California, Washington)

- 3.3.1.2 Canada: Brake Friction Material Environmental Standards (Transport Canada)

- 3.3.2 Europe

- 3.3.2.1 Germany: End-of-Life Vehicle (ELV) Directive Compliance, EcoBrake Standards

- 3.3.2.2 UK: Brake Pad Material Environmental Guidelines, MOT Vehicle Safety Standards

- 3.3.2.3 France: Low Emission Brake Pad Regulations (Copper and Heavy Metals)

- 3.3.2.4 Italy: Vehicle Safety & Brake Material Compliance (PNIEC Alignment)

- 3.3.3 Asia Pacific

- 3.3.3.1 China: Brake Friction Material Environmental Standards, Heavy Metal Restrictions

- 3.3.3.2 India: FAME II Alignment with Brake Efficiency & Safety Standards

- 3.3.3.3 Japan: JIS Brake Pad Standards & Eco-Friendly Friction Material Guidelines

- 3.3.3.4 Australia: State-Level Vehicle Brake Material Safety & Environmental Compliance

- 3.3.4 Latin America

- 3.3.4.1 Brazil: National Vehicle Safety & Brake Material Regulations (CONTRAN)

- 3.3.4.2 Mexico: Environmental Guidelines for Friction Materials in Vehicles

- 3.3.4.3 Argentina: Brake Component Safety & Environmental Compliance Programs

- 3.3.5 MEA

- 3.3.5.1 UAE: Vehicle Safety and Brake Material Standards (ADDM/DEWA Alignment)

- 3.3.5.2 3.4.5.2. Saudi Arabia: Brake Component Quality and Safety Regulations (SASO Standards)

- 3.3.5.3 3.4.5.3. South Africa: Green Transport Strategy and Brake Material Environmental Guidelines

- 3.3.1 North America

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Pricing Analysis

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Key Trade corridors & tariff impact

- 3.13.1 US-china trade dynamics

- 3.13.2 EU internal market trade

- 3.13.3 Asia-pacific regional trade

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.1.1 Predictive maintenance & wear monitoring

- 3.14.1.2 Supply chain optimization

- 3.14.1.3 Quality control & defect detection

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.2.1 Material design & simulation (OEM R&D)

- 3.14.2.2 Customer service automation (aftermarket)

- 3.14.2.3 Demand forecasting & inventory management

- 3.14.3 Risks, limitations & regulatory considerations

- 3.14.3.1 Data privacy & security concerns

- 3.14.3.2 AI model reliability & validation

- 3.14.3.3 Workforce impact & skill requirements

- 3.14.1 AI-driven disruption of existing business models

- 3.15 Investment & funding analysis

- 3.15.1 Private equity & venture capital activity

- 3.15.2 M&A trends & strategic consolidations

- 3.15.3 Government funding & R&D grants

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Semi-Metallic Brake Pads

- 5.3 Non-Asbestos Organic (NAO) Brake Pads

- 5.4 Low-Metallic NAO Brake Pads

- 5.5 Ceramic Brake Pads

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.2.1 Sedan/Wagon

- 6.2.2 SUV (Sport Utility Vehicle)

- 6.2.3 Hatchback

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

- 6.4 Two-Wheeler

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Hybrid Electric Vehicles (HEV)

- 7.4 Battery Electric Vehicles (BEV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aisin

- 10.1.2 Akebono Brake Industry

- 10.1.3 Brembo

- 10.1.4 Continental

- 10.1.5 Tenneco

- 10.1.6 Hitachi Astemo

- 10.1.7 Nisshinbo

- 10.1.8 Robert Bosch

- 10.1.9 TMD Friction

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 Advics

- 10.2.2 Brake Parts (BPI)

- 10.2.3 Delphi Technologies

- 10.2.4 Fras-le

- 10.2.5 Knorr-Bremse

- 10.2.6 Miba (Friction)

- 10.2.7 MK Kashiyama

- 10.2.8 Sangsin Brake

- 10.3 Emerging players

- 10.3.1 Hardron Motor Parts

- 10.3.2 Shandong Aotai Electric

- 10.3.3 Shandong Gold Phoenix

- 10.3.4 TVS