PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982298

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982298

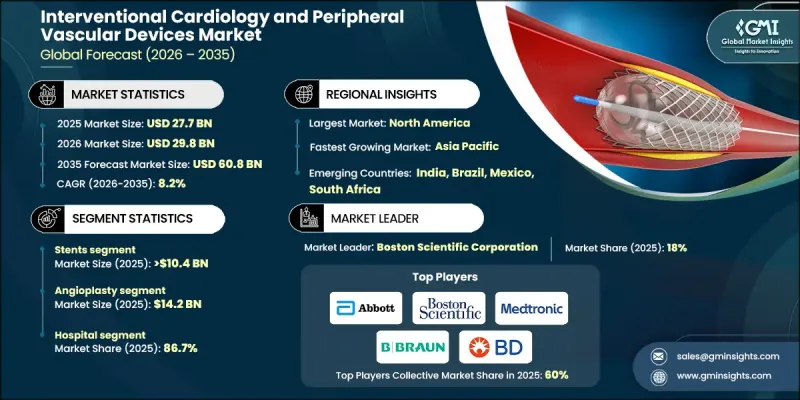

Interventional Cardiology and Peripheral Vascular Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Interventional Cardiology and Peripheral Vascular Devices Market was valued at USD 27.7 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 60.8 billion by 2035.

This growth is fueled by the rising prevalence of vascular diseases worldwide, continuous technological innovations in peripheral vascular devices, increasing adoption of minimally invasive procedures, and growing government healthcare spending to address cardiovascular disease burdens. These devices, including stents, balloons, and catheters, enable healthcare professionals to treat heart and blood vessel conditions without major surgery. Minimally invasive interventions reduce patient recovery time, lower procedural risks, and improve clinical outcomes, making them highly desirable in modern cardiovascular care. Public health initiatives and reimbursement policies further support widespread adoption, making advanced devices more accessible and cost-effective. The combination of innovative device design, regulatory support, and patient preference for safer procedures continues to drive market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.7 Billion |

| Forecast Value | $60.8 Billion |

| CAGR | 8.2% |

The stents segment generated USD 10.4 billion in 2025. Stents, small expandable mesh tubes, restore blood flow in narrowed or blocked arteries and are used in both coronary and peripheral interventions. Their clinical effectiveness, reliability, and continuous design improvements make them the preferred solution for minimally invasive treatments. Drug-eluting stents reduce restenosis and repeat procedures while shortening recovery time compared to traditional surgery, reinforcing their market dominance.

The angioplasty segment reached USD 14.2 billion in 2025 and is expected to grow at a CAGR of 8.3% during 2026-2035. Angioplasty involves inflating a balloon inside an artery to open blocked vessels, often followed by stent placement. It is widely performed for coronary and peripheral artery disease, reducing the need for open-heart surgery and promoting faster patient recovery. Its minimally invasive nature and effectiveness in treating cardiovascular conditions make angioplasty one of the most performed procedures worldwide.

North America Interventional Cardiology and Peripheral Vascular Devices Market held a 28% share in 2025. The region's market leadership is supported by a high prevalence of cardiovascular conditions, advanced healthcare infrastructure, favorable reimbursement policies, and the early adoption of minimally invasive technologies. Increasing awareness of cardiovascular disease management, technological advancements, and patient preference for less invasive procedures continue to strengthen North America's dominant market position.

Key players in the Global Interventional Cardiology and Peripheral Vascular Devices Market include Abbott Laboratories, AngioDynamics, B. Braun Melsungen AG, Becton, Dickinson and Company, Biotronik SE & Co. KG, Boston Scientific Corporation, Cardinal Health, Cook Medical, Cordis, Endologix, iVascular, Medtronic Plc, Teleflex Inc., Terumo Corporation, and W.L. Gore & Associates, Inc. Companies in the Interventional Cardiology and Peripheral Vascular Devices Market strengthen their position by investing heavily in R&D to enhance device performance, safety, and design. Strategic collaborations with hospitals, research institutions, and technology partners enable the development of next-generation stents, balloons, and catheters. Firms focus on expanding global distribution networks, securing regulatory approvals in new regions, and offering training programs for healthcare providers to increase adoption. Marketing efforts highlight clinical efficacy and procedural benefits to reinforce trust among physicians and patients.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of vascular diseases worldwide

- 3.2.1.2 Technological advancements in peripheral vascular devices

- 3.2.1.3 Rising adoption of minimally invasive procedures

- 3.2.1.4 Increasing government spending pertaining to cardiovascular diseases burden

- 3.2.2 Industry Pitfalls and Challenges:

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 Post-procedural complications associated with devices

- 3.2.3 Market Opportunities

- 3.2.3.1 Growth in outpatient and ambulatory surgical centers

- 3.2.3.2 Increasing use of robotics in interventions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Reimbursement scenario (Driven by Primary Research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Interventional catheters

- 5.3 Guidewires

- 5.4 Stents

- 5.4.1 Bioabsorbable stents

- 5.4.2 Drug eluting stents

- 5.4.3 Bare metal stents

- 5.4.4 Other stents

- 5.5 PTCA balloons

- 5.6 Atherectomy devices

- 5.7 Chronic total occlusion devices

- 5.8 Synthetic surgical grafts

- 5.9 Embolic protection devices

- 5.10 Inferior vena cava filters

- 5.11 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Congenital heart defect correction

- 6.3 Coronary thrombectomy

- 6.4 Angioplasty

- 6.5 Valvuloplasty

- 6.6 Percutaneous valve repair

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AngioDynamics

- 9.3 B. Braun Melsungen AG

- 9.4 Becton, Dickinson and Company

- 9.5 Biotronik SE & Co. KG

- 9.6 Boston Scientific Corporation

- 9.7 Cardinal Health

- 9.8 Cook Medical

- 9.9 Cordis

- 9.10 Endologix

- 9.11 iVascular

- 9.12 Medtronic Plc

- 9.13 Teleflex Inc.

- 9.14 Terumo Corporation

- 9.15 W.L. Gore & Associates, Inc.