PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982322

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982322

Automotive Electric Drivetrain Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

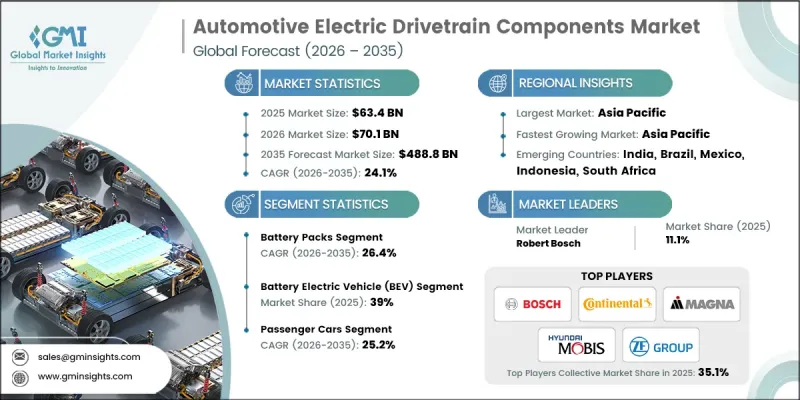

The Global Automotive Electric Drivetrain Components Market was valued at USD 63.4 billion in 2025 and is estimated to grow at a CAGR of 24.1% to reach USD 488.8 billion by 2035.

Rapid electrification across the automotive sector is accelerating demand for advanced electric drivetrain systems. Tightening emission standards worldwide compel original equipment manufacturers to transition toward electric vehicle platforms at a faster pace. This regulatory pressure is significantly increasing the production of e-drives, inverters, power electronics, and integrated electric propulsion modules. Continuous cost reductions in lithium-ion battery manufacturing and improvements in production efficiency are further reshaping vehicle pricing structures, making electric vehicles more competitive. As battery costs decline, manufacturers are scaling production of lightweight electric motors and high-efficiency inverter systems to meet growing global demand. Advancements in drivetrain technology are also enhancing vehicle range, charging compatibility, and overall system performance, which supports broader EV adoption. Automakers are integrating intelligent e-axles, connected control modules, and advanced diagnostics into electric drivetrain architectures to optimize real-time monitoring and energy management. The combination of regulatory mandates, falling battery costs, and performance-driven innovation is positioning electric drivetrain components as a core growth engine within the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $63.4 Billion |

| Forecast Value | $488.8 Billion |

| CAGR | 24.1% |

The battery packs segment held a 26% share in 2025 and is anticipated to grow at a CAGR of 26.4% from 2026 to 2035. Ongoing advancements in energy density, battery management systems, and next-generation cell chemistries are improving driving range and operational safety. Industry focus remains centered on faster charging capabilities, enhanced durability, and cost optimization. Emerging battery technologies and evolving material compositions are expected to further strengthen performance benchmarks and manufacturing scalability throughout the forecast period.

The passenger cars segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 25.2% between 2026 and 2035. Emission reduction targets and the pursuit of improved efficiency drive increasing electrification within the passenger vehicle segment. Automakers are deploying lightweight drivetrain modules, modular architectures, and high-capacity battery systems to optimize range and vehicle dynamics. Consumers are benefiting from expanding charging networks and supportive government incentives, which are accelerating adoption across urban and suburban regions. Modern passenger electric vehicles incorporate integrated technologies such as regenerative braking, real-time energy optimization, and connected vehicle systems, all of which rely on advanced electric drivetrain components.

North America Automotive Electric Drivetrain Components Market reached USD 17.2 billion in 2025. Regional efforts to harmonize electric vehicle standards across major markets are reducing cross-border supply constraints and enabling higher-volume manufacturing of drivetrain systems. Industry collaboration among suppliers is fostering the development of next-generation e-axle technologies and integrated propulsion platforms. At the same time, continued expansion of charging infrastructure throughout 2025 is strengthening consumer confidence and stimulating further demand for electric drivetrain components.

Key companies operating in the Global Automotive Electric Drivetrain Components Market include Robert Bosch, BorgWarner, ZF Friedrichshafen, Magna International, Denso, Continental, GKN Automotive, Hyundai Mobis, Dana, and Hitachi Astemo. Companies competing in the Global Automotive Electric Drivetrain Components Market are reinforcing their competitive edge through sustained investment in research and development, strategic partnerships, and vertical integration. Manufacturers are advancing high-efficiency e-drive systems, compact inverters, and integrated e-axle platforms to enhance performance and reduce system weight. Collaborations with automakers secure long-term supply agreements and early-stage integration into new electric vehicle platforms. Firms are expanding production capacity and localizing supply chains to mitigate risk and improve responsiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption & electrification push

- 3.2.1.2 Strict emission regulations & government policies

- 3.2.1.3 Declining battery costs & improving tech performance

- 3.2.1.4 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production & component costs

- 3.2.2.2 Supply chain vulnerabilities & raw material constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Advanced power electronics & lightweight modular designs

- 3.2.3.2 Emerging & developing markets

- 3.2.3.3 Sustainability & recycling solutions

- 3.2.3.4 Collaborations & cross industry partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Alliance for Automotive Innovation

- 3.4.1.2 Automotive Industry Action Group

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations (WP.29)

- 3.4.3 Asia Pacific

- 3.4.3.1 APEC Automotive Dialogue

- 3.4.3.2 ASEAN Automotive Federation

- 3.4.4 Latin America

- 3.4.4.1 Mexican Association for the Promotion of Electric Vehicles

- 3.4.4.2 Brazilian Electric Vehicle Association

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Vendor cost structure

- 3.10.2 Implementation of cost components

- 3.10.3 Ongoing operational costs

- 3.10.4 Indirect customer costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand units)

- 5.1 Key trends

- 5.2 Battery packs

- 5.3 Electric drive module

- 5.4 DC/AC inverter

- 5.5 DC/DC converter

- 5.6 Thermal system

- 5.7 Power distribution module (PDM)

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Thousand units)

- 6.1 Key trends

- 6.2 Battery electric vehicle (BEV)

- 6.3 Hybrid electric vehicle (HEV)

- 6.4 Plug-in hybrid electric vehicle (PHEV)

- 6.5 Fuel cell electric vehicle (FCEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Thousand units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Aisin

- 10.1.2 BorgWarner

- 10.1.3 Continental

- 10.1.4 Denso

- 10.1.5 Eaton

- 10.1.6 Hitachi Astemo

- 10.1.7 Hyundai Mobis

- 10.1.8 Magna International

- 10.1.9 Marelli

- 10.1.10 Robert Bosch

- 10.1.11 Valeo

- 10.1.12 ZF Friedrichshafen

- 10.2 Regional players

- 10.2.1 BYD Company

- 10.2.2 Contemporary Amperex Technology

- 10.2.3 Dana

- 10.2.4 Infineon Technologies

- 10.2.5 LG Energy Solution

- 10.2.6 MAHLE

- 10.2.7 Nidec

- 10.2.8 Panasonic (Automotive Division)

- 10.3 Emerging players

- 10.3.1 American Axle & Manufacturing

- 10.3.2 GKN Automotive (Dowlais Group)

- 10.3.3 Mitsubishi Electric

- 10.3.4 QuantumScape

- 10.3.5 WiTricity