PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982334

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982334

Text to Speech (TTS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

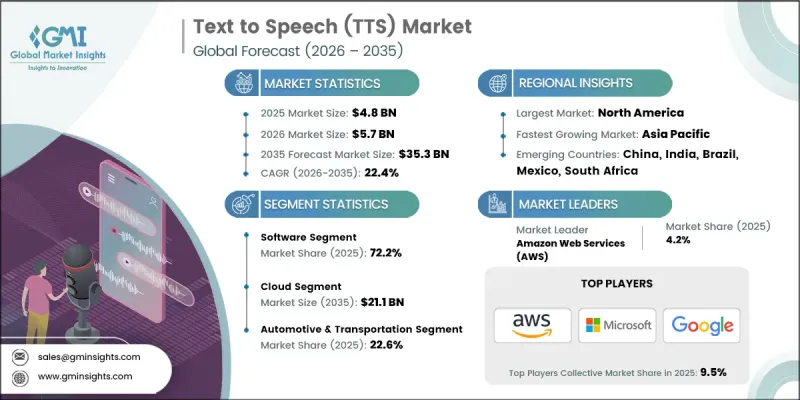

The Global Text to Speech (TTS) Market was valued at USD 4.8 billion in 2025 and is estimated to grow at a CAGR of 22.4% to reach USD 35.3 billion by 2035.

The market expansion is driven by rising demand for more natural, human-like synthesized voices, powered by advancements in artificial intelligence (AI) and natural language processing (NLP). These technologies enable TTS platforms to better interpret written content and generate highly realistic speech outputs. The adoption of TTS solutions is also fueled by the growing emphasis on accessibility, inclusivity, and assistive technologies, catering to individuals with visual impairments, learning disabilities, or those who prefer auditory learning. The integration of TTS into digital content and applications enhances information accessibility while enabling organizations to comply with accessibility standards. However, the market faces challenges, including ethical concerns and the potential misuse of synthetic voices for fraudulent activities, deep fakes, or misinformation, which can threaten privacy, reputations, and trust in digital communications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.8 Billion |

| Forecast Value | $35.3 Billion |

| CAGR | 22.4% |

The services segment is expected to grow at a CAGR of 24% from 2026 to 2035. Providers offer consulting, implementation, customization, and ongoing support, allowing businesses to deploy TTS solutions effectively while focusing on core operations. Managed TTS services, including voice personalization, speech fine-tuning, and maintenance, are increasingly sought after to enhance performance and user experience.

The hybrid segment reached USD 571.3 million in 2025 and is projected to grow at a CAGR of 22.7% during 2026-2035. Hybrid TTS combines on-device processing with cloud capabilities, balancing latency, privacy, and overall performance. This approach is gaining traction in mobile devices, wearable technologies, and automotive applications, where offline functionality complements cloud-based updates and improvements.

North America Text to Speech (TTS) Market held 38.1% share in 2025. Growth in this region is supported by stringent digital accessibility regulations and widespread adoption of assistive technologies across government, education, and corporate sectors. Organizations are increasingly updating digital platforms to comply with accessibility standards, driving TTS integration across multiple industries and use cases.

Key companies operating in the Global Text to Speech (TTS) Market include Google Inc., IBM Corporation, Amazon.com Inc., DEEPBRAIN AI, ElevenLabs, iFLYTEK Co., Ltd, Baidu Inc., and CEREPROC LTD. Companies in the Global Text to Speech (TTS) Market are focusing on strategic partnerships, technological innovation, and geographic expansion to strengthen their market presence. Providers are investing in AI-driven voice synthesis, multilingual capabilities, and personalized voice development. Collaborations with educational, corporate, and government sectors expand deployment opportunities. Companies are also enhancing cloud and hybrid offerings to provide low-latency, secure, and scalable solutions. Expanding distribution networks, improving developer tools, and offering managed services further consolidate their market position while ensuring consistent customer engagement and long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Voice technology trends

- 2.2.3 Deployment model trends

- 2.2.4 Language trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in AI and NLP for natural-sounding speech

- 3.2.1.2 Increasing adoption of TTS for accessibility and inclusive digital experiences

- 3.2.1.3 Growing demand for assistive technologies for visually impaired and elderly

- 3.2.1.4 Rising integration of TTS in customer support and IVR systems

- 3.2.1.5 Demand for multilingual and regional language support

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Ethical considerations and misuse

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with low literacy rates

- 3.2.3.2 Adoption in healthcare for patient engagement and remote monitoring

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Software-as-a-service and support

- 5.3.2 Implementation & consulting

Chapter 6 Market Estimates and Forecast, By Voice Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Neural

- 6.3 Non-Neural

Chapter 7 Market Estimates and Forecast, Deployment Model, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Language, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 English

- 8.3 Hindi

- 8.4 Mandarin chinese

- 8.5 Spanish

- 8.6 Latin

- 8.7 Arabic

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Education & E-learning

- 9.3 BFSI

- 9.4 IT & telecom

- 9.5 Consumer electronics

- 9.6 Automotive & transportation

- 9.7 Healthcare

- 9.8 Media & entertainment

- 9.9 Retail & E-commerce

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Amazon.com Inc.

- 11.1.2 Google Inc.

- 11.1.3 Microsoft Corporation

- 11.1.4 IBM Corporation

- 11.1.5 Nuance Communication

- 11.2 Regional Key Players

- 11.2.1 Baidu Inc.

- 11.2.2 iFLYTEK Co., Ltd

- 11.2.3 LumenVox LLC

- 11.2.4 Readspeaker

- 11.2.5 VONAGE AMERICA, LLC

- 11.3 Niche Players / Disruptors

- 11.3.1 CEREPROC LTD.

- 11.3.2 DEEPBRAIN AI

- 11.3.3 ElevenLabs

- 11.3.4 Lovo

- 11.3.5 MURF.AI

- 11.3.6 SESTEK

- 11.3.7 SYNTHESIA LIMITED

- 11.3.8 TextSpeak