PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982352

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982352

Food Processor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

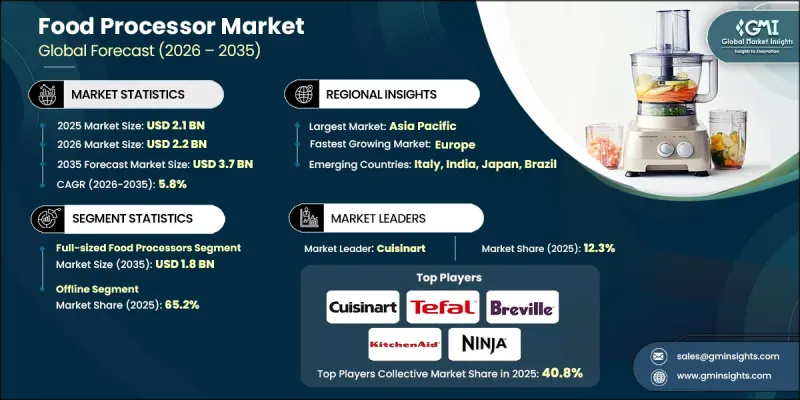

The Global Food Processor Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 3.7 billion by 2035.

Growth in the global food processor market is being driven by increasing demand for efficient kitchen appliances that support modern cooking habits. Food processors are widely used for chopping, slicing, blending, grinding, kneading, and mixing, making them essential tools for time-conscious households. Rising awareness of balanced diets and healthier eating patterns, supported by public initiatives promoting improved nutrition, is further strengthening market demand. Consumers are seeking appliances that simplify meal preparation while maintaining quality and consistency. In response, manufacturers are introducing technologically advanced models featuring smart connectivity, multifunctional capabilities, and enhanced safety features. The growing popularity of partially prepared and easy-to-cook food products is also reinforcing the need for reliable food processing solutions. As lifestyles become busier and urban populations expand, consumers increasingly prefer appliances that combine convenience, performance, and durability. Continuous product innovation and evolving consumer preferences are shaping the competitive dynamics of the food processor market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 5.8% |

Millennials and working professionals are showing strong interest in multifunctional kitchen appliances that streamline meal preparation and maximize efficiency. Convenience remains a primary purchasing factor, particularly among urban households seeking to reduce preparation time. Rapid urban development, supportive policy frameworks, and shifting dietary habits are contributing to sustained expansion in the food processor industry. As demand rises, manufacturers continue to launch new models designed to align with contemporary culinary trends and space-conscious kitchen designs.

The full-sized food processors segment generated USD 1 billion in 2025 and is forecast to reach USD 1.8 billion by 2035. Full-sized units dominate this category due to their ability to handle larger food volumes and deliver versatile performance suitable for both household and professional use. These appliances typically offer multiple speed settings, larger processing capacities, and enhanced functionality to support diverse cooking needs. Growing emphasis on sustainability and energy-efficient appliances is also influencing product development strategies within this segment.

The offline distribution channels segment accounted for 65.2% share in 2025. Physical retail outlets remain significant because they allow consumers to evaluate products directly before purchasing. In-store demonstrations, personal assistance from sales representatives, and the opportunity to compare models contribute to stronger buyer confidence. This purchasing behavior is particularly relevant in developing regions where consumers value hands-on product assessment. Government-backed initiatives that encourage shopping through local retail networks have also supported offline sales growth. In response, several leading brands are expanding their brick-and-mortar presence to strengthen market penetration.

U.S. Food Processor Market held 73.9% share in 2025. The North American food processor market is benefiting from increased home cooking activity and meal preparation trends. Strong retail infrastructure, steady import volumes, and consistent domestic manufacturing output are supporting product availability and consumer access. Trade data from federal sources indicates ongoing growth in small kitchen appliance shipments and imports, underscoring resilient demand across the region.

Key companies operating in the Global Food Processor Market include KitchenAid, Braun, Philips, Black + Decker, Kenwood, Panasonic, Moulinex, Breville, Oster, Magimix, Tefal, Hamilton Beach, Cuisinart, Bosch, and Ninja. Companies in the Food Processor Market are reinforcing their competitive position through innovation, portfolio expansion, and strategic distribution enhancements. Manufacturers are investing heavily in research and development to introduce multifunctional, energy-efficient, and smart-enabled appliances that address evolving consumer preferences. Many brands are focusing on product differentiation through advanced motor technologies, improved durability, and compact designs suited for modern kitchens. Strategic collaborations with retail chains and e-commerce platforms are strengthening omnichannel presence and improving customer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.3.1 Source consistency protocol

- 1.4 Research Trail & Confidence Scoring

- 1.4.1 Research Trail Components

- 1.4.2 Scoring Components

- 1.5 Data Collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.7 Paid sources

- 1.7.1 Sources, by region

- 1.8 Base estimates and calculations

- 1.8.1 Base year calculation for any one approach

- 1.9 Forecast model

- 1.9.1 Quantified market impact analysis

- 1.9.1.1 Mathematical impact of growth parameters on forecast

- 1.9.1 Quantified market impact analysis

- 1.10 Research transparency addendum

- 1.10.1 Source attribution framework

- 1.10.2 Quality assurance metrics

- 1.10.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Mode of Operation

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 Price

- 2.2.7 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenience in food preparation

- 3.2.1.2 Increasing health and wellness awareness

- 3.2.1.3 Technological advancements and product innovation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rising competition & product commoditization

- 3.2.2.2 Consumer shift toward all in one smart kitchen systems

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for convenience driven home cooking solutions

- 3.2.3.2 Growth of smart, connected kitchen appliances

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Pricing analysis, 2025

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Trade statistics

- 3.9.1 Major importing countries

- 3.9.2 Major exporting countries

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behaviour

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Full-sized food processors

- 5.3 Mini food processors

- 5.4 Hand-operated food processors

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Capacity, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Up to 2 liters

- 7.3 2-5 liters

- 7.4 Above 5 liters

Chapter 8 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-Commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Supermarkets/Hypermarkets

- 10.3.2 Specialty Stores

- 10.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 11 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 France

- 11.3.3 UK

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Black+Decker

- 12.2 Bosch

- 12.3 Braun

- 12.4 Breville

- 12.5 Cuisinart

- 12.6 Hamilton Beach

- 12.7 Kenwood

- 12.8 KitchenAid

- 12.9 Magimix

- 12.10 Moulinex

- 12.11 Ninja

- 12.12 Oster

- 12.13 Panasonic

- 12.14 Philips

- 12.15 Tefal