PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982354

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982354

Automotive Pedestrian Protection System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

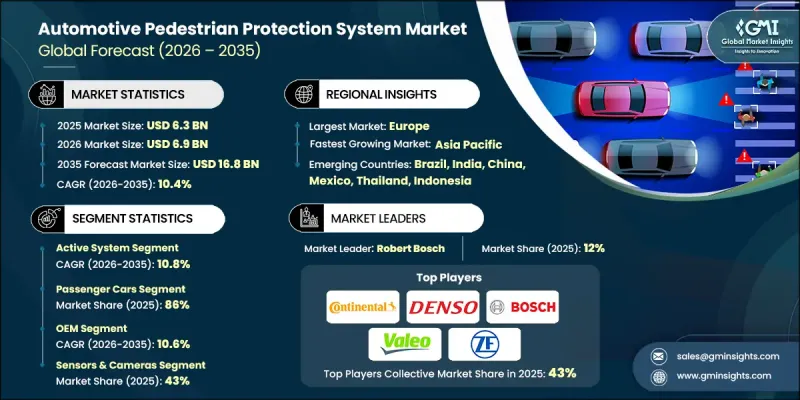

The Global Automotive Pedestrian Protection System Market was valued at USD 6.3 billion in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 16.8 billion by 2035.

The market is gaining strong momentum as automakers prioritize vehicle safety technologies designed to reduce pedestrian injuries and fatalities, particularly in high-traffic urban environments. Pedestrian protection systems (PPS) combine advanced emergency braking with pedestrian detection, deployable safety components, sensor-based monitoring, and intelligent impact mitigation technologies to either prevent collisions or reduce injury severity. The market encompasses integrated safety software, sensor hardware, actuator systems, structural energy-absorbing designs, and engineering support services supplied to OEMs and Tier 1 manufacturers. Over time, pedestrian protection solutions have evolved from passive structural designs to intelligent, AI-enabled systems capable of real-time object recognition and predictive collision avoidance. Strict safety mandates and vehicle rating programs worldwide are accelerating adoption, as regulators require advanced braking systems with pedestrian and cyclist detection capabilities in new vehicles. Growing reliance on cloud-based simulation tools and digital validation platforms is further enhancing system accuracy and accelerating innovation across the automotive pedestrian protection system market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.3 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 10.4% |

The active system segment accounted for 59% share in 2025 and is anticipated to grow at a CAGR of 10.8% from 2026 to 2035. Active pedestrian protection technologies integrate forward-facing cameras, radar sensors, and increasingly LiDAR systems with advanced processing software. These systems detect pedestrian movement, assess trajectory risks, calculate collision probability, and automatically activate braking functions when predefined safety thresholds are reached, significantly improving real-time response capabilities.

The passenger cars segment held 86% share in 2025 and is projected to grow at a CAGR of 10.2%. Demand within this segment is supported by stringent pedestrian safety assessment standards established by organizations such as the European New Car Assessment Programme and the National Highway Traffic Safety Administration, which place significant emphasis on active pedestrian safety performance. Regulatory pressure across vehicle categories is encouraging manufacturers to adopt advanced simulation and validation platforms to ensure compliance and optimize system efficiency.

Germany Automotive Pedestrian Protection System Market is forecast to grow at a CAGR of 10.9% between 2026 and 2035. The country's leadership is supported by strong investments in safety innovation from major automotive manufacturers such as BMW, Mercedes-Benz, Audi, and Porsche. Increasing urban mobility complexity and mixed-traffic environments are driving the integration of highly reliable pedestrian protection systems designed to operate effectively in dynamic real-world conditions.

Key companies operating in the Global Automotive Pedestrian Protection System Market include ZF Friedrichshafen, Aptiv, Denso, Valeo, Robert Bosch, Autoliv, Continental, Marelli, Hitachi Astemo, and Hella. Companies in the Automotive Pedestrian Protection System Market strengthen their competitive position through continuous investment in research and development focused on AI-driven sensing, advanced braking algorithms, and sensor fusion technologies. Strategic collaborations with OEMs and Tier 1 suppliers enable co-development of integrated safety platforms tailored to specific vehicle architectures. Firms are expanding simulation capabilities using cloud-based validation tools to accelerate product certification and regulatory compliance. Geographic expansion, portfolio diversification, and modular system designs allow suppliers to serve both premium and mass-market vehicle segments. In addition, companies emphasize cost optimization, scalable production, and software updates to enhance long-term system performance, ensuring sustainable growth and stronger market penetration in the evolving global automotive safety landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Components

- 2.2.3 Product

- 2.2.4 Vehicles

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent global pedestrian safety regulations & mandates

- 3.2.1.2 Rising pedestrian fatality rates in urban areas

- 3.2.1.3 Increasing consumer demand for advanced safety features

- 3.2.1.4 Growing adoption of ADAS & autonomous driving technologies

- 3.2.1.5 Insurance industry push for safety-rated vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation & integration costs

- 3.2.2.2 Low system efficiency in adverse weather conditions

- 3.2.2.3 Limited aftermarket adoption due to technical complexity

- 3.2.2.4 One-time use nature of passive systems (external airbags)

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit solutions for existing commercial vehicle fleets

- 3.2.3.2 Integration with V2X & smart city infrastructure

- 3.2.3.3 Emerging markets with developing safety standards

- 3.2.3.4 AI-enhanced nighttime detection systems

- 3.2.3.5 Lightweight materials for passive protection systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal safety rules & ADAS deployment guidance

- 3.4.1.2 Canada - Safety framework for connected & automated vehicles (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- Euro NCAP pedestrian safety ratings

- 3.4.2.2 UK- Post-Brexit ADAS flexibility

- 3.4.2.3 France- National ADAS testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging ADAS & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (camera, LiDAR, RADAR, ultrasonic)

- 3.7.1.2 Sensor fusion & integration

- 3.7.1.3 AI & machine learning in pedestrian detection

- 3.7.2 Emerging technologies

- 3.7.2.1 V2X communication for enhanced detection

- 3.7.2.2 Nighttime & low-light detection technologies

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Key patent trends

- 3.8.2 Technology innovation hotspots

- 3.8.3 Patent filing by key players

- 3.8.4 Emerging IP strategies

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Use cases & success stories

- 3.11 Case studies

- 3.11.1 OEM integration of PPS technologies

- 3.11.2 Commercial vehicle fleet deployments

- 3.11.3 Retrofit pedestrian protection programs

- 3.11.4 Urban pilot projects in smart cities

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Future trends and market outlook

- 3.14.1 Next-generation sensor technologies

- 3.14.2 Integration with autonomous driving ecosystems

- 3.14.3 AI-driven predictive pedestrian safety systems

- 3.14.4 Expansion in emerging markets

- 3.15 Market risks and mitigation strategies

- 3.15.1 Regulatory compliance risks

- 3.15.2 Technology adoption barriers

- 3.15.3 Supply chain disruptions

- 3.15.4 Cybersecurity and data privacy concerns

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Sensors & cameras

- 5.3 Control unit

- 5.4 Actuators

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Active system

- 6.3 Passive system

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.3.9 Denmark

- 9.3.10 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Israel

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Autoliv

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 Ford Motor

- 10.1.5 Magna International

- 10.1.6 Mobileye

- 10.1.7 Nissan Motor

- 10.1.8 Robert Bosch

- 10.1.9 Toyota Motor

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 Aptiv

- 10.2.2 HELLA

- 10.2.3 Hitachi Astemo

- 10.2.4 Hyundai Mobis

- 10.2.5 Knorr-Bremse

- 10.2.6 Magneti Marelli

- 10.2.7 Subaru

- 10.2.8 Valeo

- 10.3 Emerging Players & Technology Enablers

- 10.3.1 Gentex

- 10.3.2 Luminar Technologies