PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982355

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982355

Space Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

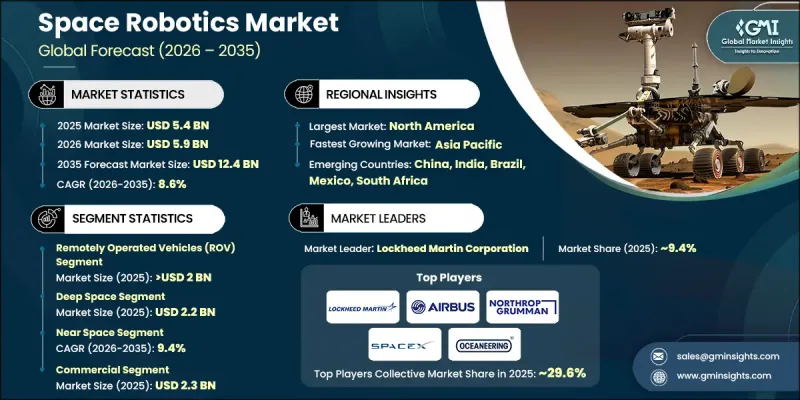

The Global Space Robotics Market was valued at USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 12.4 billion by 2035.

The sector is expanding as the complexity and scope of space missions grow, creating demand for advanced robotic and automation technologies that can operate across diverse extraterrestrial environments. Space agencies and commercial enterprises are developing robotic systems to support long-duration missions in deep space, reduce reliance on astronauts, and enhance operational efficiency. These systems are being designed for multiple applications, including in-space servicing, assembly, and planetary exploration, enabling more frequent, complex, and cost-effective missions. Integration of robotics into space programs allows for real-time monitoring, automated task execution, and mission support that would otherwise strain human resources. Governments, research institutions, and private players are collectively driving innovation, ensuring that robotics plays a pivotal role in the future of space operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 8.6% |

The remotely operated vehicles (ROV) segment reached USD 2 billion in 2025, owing to their critical role in space exploration, orbital inspections, planetary rovers, and space station operations. ROVs act as versatile platforms capable of performing remote tasks in hazardous or inaccessible environments, supporting surface exploration, sample collection, and in-orbit maintenance with both real-time control and autonomous capabilities.

The commercial segment reached USD 2.3 billion in 2025, driven by the rapid expansion of private space companies engaged in satellite deployment, space tourism, in-orbit manufacturing, and commercial stations. Commercial space robotics is extensively applied for satellite management, launch operations, inspection, and maintenance, allowing scalable and cost-efficient operations. Strong private investments, increasing launch cadence, and technological innovation further accelerate adoption across commercial missions.

North America Space Robotics Market held a 38.5% share in 2025. The region's growth is fueled by substantial government funding, robust space exploration programs, defense initiatives, and investment in space infrastructure. Agencies and enterprises in North America are leveraging long-term programs to develop advanced robotic platforms, strengthening the region's leadership in space robotics technologies.

Key players operating in the Global Space Robotics Market include Lockheed Martin Corporation, Honeybee Robotics, Astroscale Holdings Inc., Northrop Grumman, Astrobotic Technology, Intuitive Machines LLC, Made In Space Inc. (Redwire LLC), SpaceX, MAXAR TECHNOLOGIES, Airbus SE, Oceaneering International Inc., MDA Space, Altius Space Machine, ITT Corporation, Motiv Space Systems Inc., Olis Robotics, BluHaptics Inc., Ispace, and Metecs LLC. Companies in the Global Space Robotics Market are adopting several strategies to solidify their market presence and expand their global footprint. Leading players are investing in research and development to design autonomous and semi-autonomous robotic systems for deep-space exploration, orbital servicing, and planetary operations. Strategic collaborations with space agencies, commercial launch providers, and satellite operators enable deployment at scale. Firms are also focusing on modular, reconfigurable robotic platforms to support multiple mission profiles and reduce operational costs. Technological innovation in AI, machine learning, sensors, and teleoperation is a priority to enhance precision, reliability, and safety.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Mathematical impact of growth parameters on forecast

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End User trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Satellite Constellations and Deep-Space Missions

- 3.2.1.2 Rising Demand for Autonomous and AI-Enabled Space Operations

- 3.2.1.3 Growth in Space Tourism and Commercial Space Activities

- 3.2.1.4 Increasing Public-Private Sector Collaboration in Space Programs

- 3.2.1.5 Need for In-Orbit Servicing, Debris Removal, and Satellite Maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Development Costs and Technical Complexity

- 3.2.2.2 Operational Risks in Harsh and Unpredictable Space Environments

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of autonomous robotic systems for space missions

- 3.2.3.2 Growing demand for in-orbit servicing, assembly, and manufacturing (ISAM)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Remotely Operated Vehicles (ROV)

- 5.2.1 Rovers/Spacecraft Landers

- 5.2.2 Space Probes

- 5.2.3 Others

- 5.3 Remote Manipulator System (RMS)

- 5.3.1 Robotic Arms/Manipulator Systems

- 5.3.2 Gripping & Docking Systems

- 5.3.3 Others

- 5.4 Software

- 5.5 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Remote Sensing

- 6.3 Autonomous Systems

- 6.4 Teleoperation

- 6.5 Robotic Software

- 6.6 Artificial Intelligence (AI) and Machine Learning (ML)

- 6.7 Human-Robot Interaction

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Deep Space

- 7.2.1 Planetary Exploration

- 7.2.2 Asteroid Mining

- 7.2.3 Space Research

- 7.3 Near Space

- 7.3.1 Satellite Operations

- 7.3.2 Space Station Maintenance

- 7.3.3 Orbital Transportation

- 7.3.4 Others

- 7.4 Ground

- 7.4.1 Launch Operations

- 7.4.2 Ground Control Operations

- 7.4.3 Space Research Labs

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

- 8.4 Defence

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Airbus SE

- 10.1.2 ITT Corporation

- 10.1.3 Lockheed Martin Corporation

- 10.1.4 MAXAR TECHNOLOGIES

- 10.1.5 MDA Space

- 10.1.6 Northrop Grumman

- 10.1.7 SpaceX

- 10.2 Regional Players

- 10.2.1 Altius Space Machine

- 10.2.2 Astrobotic Technology

- 10.2.3 Astroscale Holdings Inc.

- 10.2.4 Honeybee Robotics

- 10.2.5 Intuitive Machines, LLC.

- 10.2.6 Ispace

- 10.2.7 Made In Space Inc. (Redwire LLC)

- 10.2.8 Metecs, LLC.

- 10.2.9 Oceaneering International, Inc.

- 10.3 Local / Niche Players

- 10.3.1 BluHaptics, Inc.

- 10.3.2 Motiv Space Systems, Inc.

- 10.3.3 Olis Robotics