PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982371

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982371

U.S. OTC Hearing Aids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

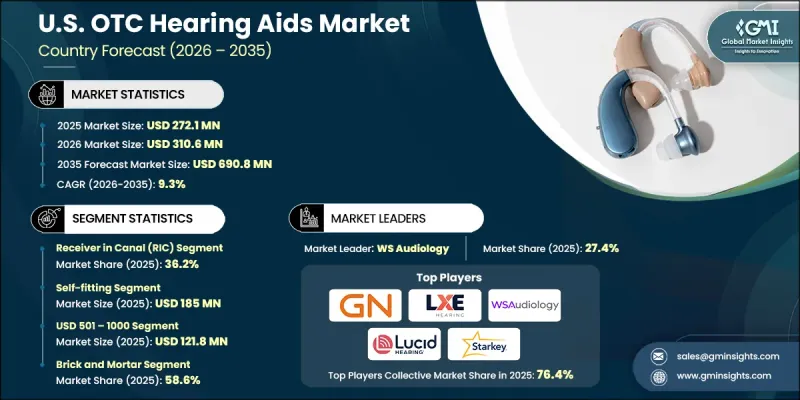

U.S. OTC Hearing Aids Market was valued at USD 272.1 million in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 690.8 million by 2035.

Market expansion is driven by the rising incidence of hearing loss, technological advancements, and regulatory support for over-the-counter devices. OTC hearing aids are designed for adults with mild to moderate hearing loss, enabling direct purchase without prescriptions or professional fittings. This approach reduces barriers to access compared to traditional prescription-based solutions. Increasing exposure to environmental noise and an aging population are fueling demand for convenient, user-friendly hearing aids. Innovations such as digital signal processing, Bluetooth connectivity, self-fitting capabilities, and rechargeable batteries have significantly improved device performance and consumer experience. These improvements also address historical concerns about the quality and reliability of direct-to-consumer products. As awareness grows, more adults are seeking accessible and technologically advanced hearing solutions to improve daily communication and overall quality of life.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $272.1 Million |

| Forecast Value | $690.8 Million |

| CAGR | 9.3% |

The receiver-in-canal (RIC) segment held a 36.2% share in 2025. RIC devices place the speaker closer to the eardrum, enhancing sound clarity, naturalness, and speech comprehension across a wider frequency range. Consumers prefer RIC aids for their discreet designs, superior audio quality, flexibility in fitting, and compatibility with smartphones, making them a popular choice for mild to moderate hearing loss.

The self-fitting category segment reached USD 185 million and is expected to grow at a CAGR of 9.6% in 2025. These devices allow users to customize settings and sound profiles independently, eliminating the need for frequent professional appointments. Real-time personalization improves comfort, satisfaction, and consistent use, reducing the overall financial burden associated with clinical intervention.

South Atlantic OTC Hearing Aids Market generated USD 58.6 million in 2025. This region's growth is fueled by a rapidly aging population, which drives higher demand for easily accessible hearing aids that do not require prescriptions or professional fittings. The demographic trend directly supports regional market expansion.

Key players in the U.S. OTC Hearing Aids Market include Audien Hearing, GN Store Nord, Starkey, LXE Hearing, Ceretone Hearing Aids, MDHearing, NuvoMed, Audicus, Elehear, WS Audiology, Lucid Hearing (Hearing Lab Technology), Sonova, NUHEARA, and Soundwave Hearing. Leading companies strengthen their U.S. OTC Hearing Aids Market position through multiple strategies. They invest in research and development to introduce innovative, user-friendly devices, expand online and offline distribution networks, and enhance brand credibility via professional endorsements. Marketing initiatives leverage digital campaigns and influencer partnerships to increase awareness among adult consumers. Companies focus on subscription models, loyalty programs, and after-sales support to encourage repeat purchases. Competitive pricing, bundled offerings, and continuous technology upgrades ensure consumer retention while capturing a growing segment of self-directed users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by zone

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Zonal trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Price band trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of hearing loss

- 3.2.1.2 Rising geriatric population base

- 3.2.1.3 Technological advancements

- 3.2.1.4 Steadily surging awareness & penetration of hearing devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Poor awareness and social stigma associated with wearing hearing aids

- 3.2.2.2 Concerns over device quality and efficacy

- 3.2.3 Market opportunities

- 3.2.3.1 Surging need for customized and user-friendly product innovations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 OTC hearing aids legislation

- 3.7 Future market trends

- 3.8 Consumer feature preference analysis

- 3.9 Consumer pathway

- 3.10 Market scenario

- 3.11 Pricing analysis, 2025

- 3.12 Number of OTC hearing aids sold (units), by zone, 2022 - 2035

- 3.12.1 East North Central

- 3.12.2 West South Central

- 3.12.3 South Atlantic

- 3.12.4 Northeast

- 3.12.5 East South Central

- 3.12.6 West North Central

- 3.12.7 Pacific Central

- 3.12.8 Mountain States

- 3.13 Brand analysis

- 3.14 Epidemiology scenario

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

- 3.17 Gap analysis

- 3.18 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Receiver in canal (RIC)

- 5.3 Behind-the-ear (BTE)

- 5.4 Earbud-style

- 5.5 Completely-in-the-canal (CIC)

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Self-fitting

- 6.3 Preset

Chapter 7 Market Estimates and Forecast, By Price Band, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Upto USD 500

- 7.3 USD 501 - 1000

- 7.4 Over USD 1000

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Brick and mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Zone, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 East North Central

- 9.2.1 Illinois

- 9.2.2 Indiana

- 9.2.3 Michigan

- 9.2.4 Ohio

- 9.2.5 Wisconsin

- 9.3 West South Central

- 9.3.1 Arkansas

- 9.3.2 Louisiana

- 9.3.3 Oklahoma

- 9.3.4 Texas

- 9.4 South Atlantic

- 9.4.1 Delaware

- 9.4.2 Florida

- 9.4.3 Georgia

- 9.4.4 Maryland

- 9.4.5 North Carolina

- 9.4.6 South Carolina

- 9.4.7 Virginia

- 9.4.8 West Virginia

- 9.4.9 Washington, D.C.

- 9.5 Northeast

- 9.5.1 Connecticut

- 9.5.2 Maine

- 9.5.3 Massachusetts

- 9.5.4 New Hampshire

- 9.5.5 Rhode Island

- 9.5.6 Vermont

- 9.5.7 New Jersey

- 9.5.8 New York

- 9.5.9 Pennsylvania

- 9.6 East South Central

- 9.6.1 Alabama

- 9.6.2 Kentucky

- 9.6.3 Mississippi

- 9.6.4 Tennessee

- 9.7 West North Centra

- 9.7.1 Iowa

- 9.7.2 Kansas

- 9.7.3 Minnesota

- 9.7.4 Missouri

- 9.7.5 Nebraska

- 9.7.6 North Dakota

- 9.7.7 South Dakota

- 9.8 Pacific Central

- 9.8.1 Alaska

- 9.8.2 California

- 9.8.3 Hawaii

- 9.8.4 Oregon

- 9.8.5 Washington

- 9.9 Mountain States

- 9.9.1 Arizona

- 9.9.2 Colorado

- 9.9.3 Utah

- 9.9.4 Nevada

- 9.9.5 New Mexico

- 9.9.6 Idaho

- 9.9.7 Montana

- 9.9.8 Wyoming

Chapter 10 Company Profiles

- 10.1 Audicus

- 10.2 Audien Hearing

- 10.3 Ceretone Hearing Aids

- 10.4 Elehear

- 10.5 GN Store Nord

- 10.6 Lucid Hearing (Hearing Lab Technology)

- 10.7 LXE Hearing

- 10.8 MDHearing

- 10.9 NUHEARA

- 10.10 NuvoMed

- 10.11 Sonova

- 10.12 Soundwave Hearing

- 10.13 Starkey

- 10.14 WS Audiology