PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982381

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982381

Automotive HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

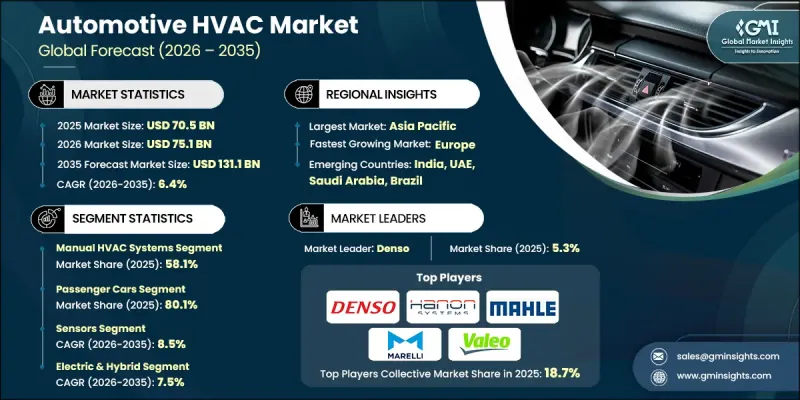

The Global Automotive HVAC Market was valued at USD 70.5 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 131.1 billion by 2035.

Market growth is driven by increasing vehicle ownership worldwide, supported by rising disposable income and shifting consumer mobility preferences. As more consumers invest in personal vehicles, demand for advanced heating, ventilation, and air conditioning systems continues to accelerate. Mid-range and premium vehicle categories are increasingly incorporating enhanced HVAC technologies that deliver improved cabin comfort and climate control performance. At the same time, manufacturers are integrating intelligent climate solutions equipped with advanced sensing technologies that allow occupants to personalize airflow and temperature settings. The rapid growth of electric vehicles has further elevated the importance of HVAC efficiency, as these systems directly influence battery performance and overall driving range. To address this, companies are developing energy-efficient solutions such as heat pump systems and advanced thermal management modules. In parallel, evolving environmental regulations are encouraging the adoption of low global warming potential refrigerants, improved sealing systems, and recyclable components, reinforcing the shift toward sustainable automotive HVAC technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.5 Billion |

| Forecast Value | $131.1 Billion |

| CAGR | 6.4% |

The manual HVAC systems segment accounted for 58.1% share in 2025, generating USD 40.9 billion. Their leadership position stems from cost efficiency, simplified design architecture, and lower production and maintenance expenses compared to automatic systems. With fewer electronic components and sensors, these systems offer dependable performance and straightforward servicing, making them highly attractive across large vehicle production volumes. Their durability and reduced technical complexity further support sustained demand.

The passenger cars segment held 80.1% share in 2025 and is forecast to reach USD 107.6 billion by 2035. Higher global production and sales volumes of passenger vehicles compared to commercial vehicles significantly increase HVAC system demand within this category. Automakers continue to enhance cabin comfort features to meet consumer expectations, reinforcing segment dominance. Passenger vehicles prioritize occupant comfort and interior experience, which drives greater integration of advanced climate control technologies.

U.S. Automotive HVAC Market reached USD 7.8 million in 2025, supported by high vehicle ownership rates and strong consumer preference for comfort-oriented features. Growth is further driven by the expansion of electric and hybrid vehicle sales, which require optimized energy-efficient HVAC systems. Smart climate control technologies, including zonal management and connected controls, are gaining traction in both OEM and aftermarket channels. Regulatory measures increasingly emphasize vehicle energy efficiency, reinforcing innovation in system design and component optimization.

Leading companies operating in the Global Automotive HVAC Market include Valeo, Denso, Marelli, Hanon Systems, Sensata, Mahle, Air International Thermal Systems, Sanden, Johnson Electric, and Visteon. Companies in the Global Automotive HVAC Market are strengthening their competitive positions through continuous innovation and strategic partnerships. Major players are investing in advanced thermal management technologies, energy-efficient compressors, and intelligent climate control systems tailored for electric and hybrid vehicles. Collaboration with automakers enables early integration of next-generation HVAC platforms into new vehicle architectures. Firms are expanding global manufacturing footprints to improve supply chain resilience and reduce production costs. Research and development efforts focus on lightweight materials, smart sensors, and environmentally friendly refrigerants to comply with tightening emission regulations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Propulsion

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for passenger comfort

- 3.2.1.2 Rising vehicle production globally

- 3.2.1.3 Growth in electric and hybrid vehicles

- 3.2.1.4 Technological advancements in HVAC systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity in HVAC system integration

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in emerging markets

- 3.2.3.2 Lightweight and compact HVAC designs for EVs

- 3.2.3.3 Aftermarket HVAC upgrades and retrofitting

- 3.2.3.4 Integration with IoT and connected vehicle systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Environmental Protection Agency (EPA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Canadian Standards Association (CSA)

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association (ACEA)

- 3.4.2.2 European Union Emissions Trading System (EU ETS)

- 3.4.2.3 European Committee for Standardization (CEN)

- 3.4.2.4 European Environment Agency (EEA)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Road Transport and Highways (MoRTH)

- 3.4.3.2 Bureau of Energy Efficiency (BEE)

- 3.4.3.3 China Automotive Technology & Research Center (CATARC)

- 3.4.3.4 Japan Automobile Manufacturers Association (JAMA)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO

- 3.4.4.2 Ministry of Transport

- 3.4.4.3 National Agency for Land Transportation (ANTT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization & Metrology (ESMA)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.4 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electrification of HVAC Systems

- 3.7.1.2 Dual-Zone and Multi-Zone Climate Control

- 3.7.1.3 Cabin Air Filtration and Purification Systems

- 3.7.1.4 Integration with Vehicle Telematics and Infotainment

- 3.7.2 Emerging technologies

- 3.7.2.1 Thermoelectric HVAC Systems

- 3.7.2.2 Solar-Powered HVAC Units

- 3.7.2.3 Smart and AI-Enabled Climate Control

- 3.7.2.4 Lightweight and Compact HVAC Designs for EVs

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Electrification impact on HVAC architecture

- 3.11.1 High voltage vs. low voltage HVAC system comparison

- 3.11.2 Cabin preconditioning strategies and energy management

- 3.11.3 Range anxiety mitigation

- 3.11.4 Dual-source heating systems

- 3.12 OEM integration strategies and platform approaches

- 3.12.1 Modular HVAC platform development

- 3.12.2 Vehicle architecture integration challenges (ICE vs. EV)

- 3.12.3 Co-development partnerships between OEMs and suppliers

- 3.12.4 Customization vs. standardization

- 3.13 Health and wellness feature integration

- 3.13.1 HEPA filtration and PM2.5 removal capabilities

- 3.13.2 Antimicrobial and antiviral coating technologies

- 3.13.3 Humidity control for health optimization

- 3.13.4 Allergen and pathogen detection systems

- 3.13.5 Aromatherapy and air ionization features

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Automatic HVAC systems

- 5.3 Manual HVAC systems

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Sensors

- 6.2.1 Temperature sensors

- 6.2.2 Humidity sensors

- 6.2.3 Air quality sensors

- 6.2.4 Others

- 6.3 Heat exchangers

- 6.3.1 Condenser

- 6.3.2 Evaporator

- 6.4 Compressor

- 6.5 Expansion device

- 6.6 Receiver/drier

- 6.7 Blower motor

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric & hybrid

- 8.3.1 BEV

- 8.3.2 HEV

- 8.3.3 PHEV

- 8.3.4 FCEV

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Czech Republic

- 10.3.7 Belgium

- 10.3.8 Russia

- 10.3.9 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Denso

- 11.1.2 Valeo

- 11.1.3 Mahle

- 11.1.4 Hanon Systems

- 11.1.5 Sanden

- 11.1.6 Marelli

- 11.1.7 Delphi

- 11.1.8 Visteon

- 11.1.9 Johnson Electric

- 11.2 Regional players

- 11.2.1 Air International Thermal Systems

- 11.2.2 Subros

- 11.2.3 Songz

- 11.2.4 Shanghai Velle

- 11.2.5 Hubei Meibiao

- 11.2.6 Bergstrom

- 11.3 Emerging players

- 11.3.1 Gentherm

- 11.3.2 Behr Hella Service

- 11.3.3 Trans Air Manufacturing

- 11.3.4 Motherson

- 11.3.5 Modine