PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998663

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998663

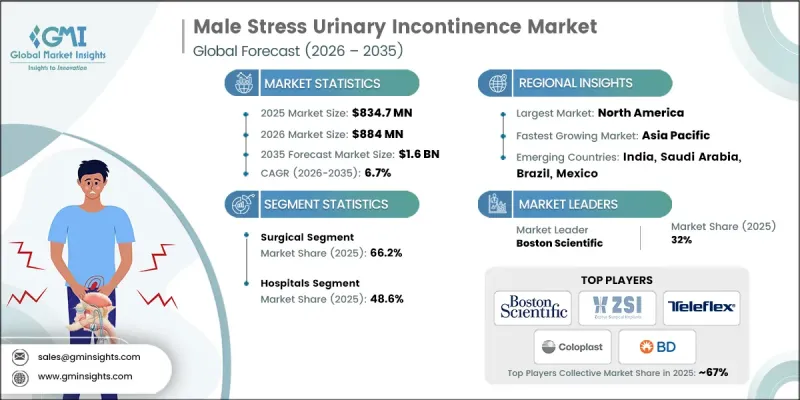

Male Stress Urinary Incontinence Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Male Stress Urinary Incontinence Market was valued at USD 834.7 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 1.6 billion by 2035.

Market growth is fueled by the rising incidence of prostate cancer, the increasing prevalence of male stress urinary incontinence (SUI), and continuous innovation in medical devices and surgical procedures. As prostate cancer remains one of the most frequently diagnosed cancers among men, the number of patients experiencing urinary control complications following treatment continues to grow. The expanding aging male population worldwide further contributes to higher diagnosis rates and subsequent incontinence management needs. As awareness surrounding post-treatment urinary complications improves, demand for both interventional and non-invasive management solutions is steadily increasing. The market encompasses specialized medical technologies developed to manage involuntary urine leakage associated with physical exertion. Core product categories include artificial urinary sphincters and male sling systems designed to restore continence and significantly enhance patient quality of life. Additionally, the expansion of urology-focused specialty centers and the advancement of next-generation artificial urinary sphincter designs are reinforcing long-term industry demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $834.7 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 6.7% |

The surgical treatment segment held a 66.2% share in 2025, supported by the growing number of outpatient and ambulatory surgical center-based procedures. Surgical intervention remains the preferred approach for moderate to severe male SUI cases. Artificial urinary sphincter systems are widely recognized as the clinical benchmark due to their strong long-term efficacy data and consistent continence outcomes. Male sling systems also represent an important therapeutic option, particularly for patients with less severe symptoms and preserved urethral function. Clinical recommendations and established treatment protocols continue to reinforce surgical adoption rates across healthcare systems.

The hospitals segment captured 48.6% share in 2025. These institutions serve as primary centers for complex surgical procedures, including artificial urinary sphincter implantation, which requires experienced surgical teams and advanced operating facilities. Hospital-based urology departments frequently manage more complicated post-treatment incontinence cases and provide comprehensive patient care through multidisciplinary collaboration. Even as outpatient surgical models expand, hospitals remain central to delivering advanced male SUI interventions.

North America Male Stress Urinary Incontinence Market held 46.6% share in 2025 and is expected to witness steady growth throughout the forecast period. Regional expansion is supported by strong awareness of urinary incontinence following prostate-related treatments and high adoption of advanced therapeutic technologies. A well-established urology infrastructure enables timely diagnosis, structured referral pathways, and access to both surgical and conservative management strategies, strengthening overall treatment accessibility.

Key companies operating in the Global Male Stress Urinary Incontinence Market include Boston Scientific, Coloplast, Becton, Dickinson and Company, Teleflex, and A.M.I. GmbH, Promedon, Rigicon, Inc., Zephyr Surgical Implants (ZSI), Neomedic, and CL Medical. These organizations compete through technological innovation, clinical validation, and expansion of global distribution networks. Companies in the Global Male Stress Urinary Incontinence Market are strengthening their competitive positions through continuous product development and clinical research investments. Manufacturers are focusing on enhancing device durability, ease of implantation, and patient comfort to improve long-term treatment outcomes. Strategic partnerships with urology centers and surgeon training programs help expand procedural adoption and build physician confidence. Firms are also pursuing geographic expansion strategies to penetrate emerging markets while reinforcing their presence in established regions. Regulatory compliance, post-market surveillance programs, and real-world clinical data generation further strengthen brand credibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of male stress urinary incontinence (post-prostatectomy dominance)

- 3.2.1.2 Technological advancements in devices and surgical techniques

- 3.2.1.3 Growing incidence of prostate cancer

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procedural cost

- 3.2.3 Opportunities

- 3.2.3.1 Large untreated moderate-to-severe SUI population

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Consumer insights

- 3.7 Investment landscape

- 3.8 Number of procedures, by region, 2025

- 3.8.1 Male slings

- 3.8.2 Artificial urinary sphincters (AUS)

- 3.9 Epidemiology scenario by severity of incontinence

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical

- 5.2.1 Artificial Urinary Sphincter (AUS)

- 5.2.2 Male slings

- 5.2.3 Adjustable continence balloons

- 5.3 Non-Surgical

- 5.3.1 Condom catheters

- 5.3.2 Penile clamps

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Urology clinics

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 A.M.I. GmbH

- 8.2 Becton, Dickinson and Company

- 8.3 Boston Scientific

- 8.4 CL Medical

- 8.5 Coloplast

- 8.6 Neomedic

- 8.7 Promedon

- 8.8 Rigicon, Inc.

- 8.9 Teleflex

- 8.10 Zephyr Surgical Implants (ZSI)