PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998666

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998666

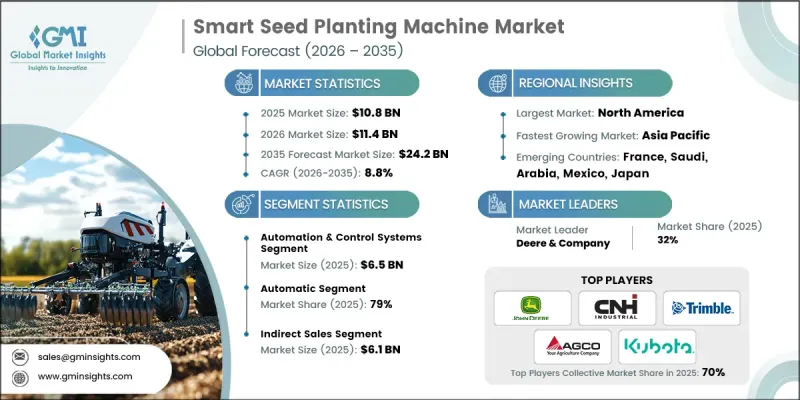

Smart Seed Planting Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Smart Seed Planting Machine Market was valued at USD 10.8 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 24.2 billion by 2035.

Expansion in the smart seed planting machine market for smart agricultural equipment is largely supported by the growing emphasis on improving farming productivity while optimizing operational efficiency. Agricultural producers are increasingly adopting advanced equipment that enables data-based decision making, allowing them to determine ideal planting conditions by evaluating factors related to soil quality, field variability, moisture distribution, and seed characteristics. The availability of advanced digital platforms, sensing technologies, and automated systems is also improving accessibility to precision farming tools. As a result, growers are recognizing that more accurate seed placement can significantly improve germination performance and reduce input wastage, which contributes to more stable crop yields. In addition, the integration of digital agriculture solutions is transforming planting operations by enabling more consistent and predictable outcomes. As farms continue to modernize operations and rely on technology-driven agricultural management, the demand for smart seed planting machines is expected to grow steadily.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.8 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 8.8% |

Changing environmental conditions have further reduced the reliability of conventional planting approaches that rely on estimation rather than data-driven insights. Precision planting systems offer a dependable alternative by delivering consistent operational performance across varying field conditions. These machines allow farmers to monitor planting efficiency continuously, adjust machine settings automatically, and maintain detailed field records that support improved planning and long-term operational strategies. The shift toward precision agriculture represents a major transformation in modern farming practices, providing producers with improved control over planting operations and enabling more efficient management of agricultural resources.

In 2025, the automation & control systems segment accounted for USD 6.5 billion. Modern smart planting equipment relies heavily on automation and control technologies to ensure highly accurate and uniform seed distribution. These systems combine digital seed metering mechanisms, electronically controlled actuators, real-time programmable control units, and machine communication platforms to regulate seed placement, depth consistency, and row spacing. By automating key operational parameters, these technologies reduce variability caused by manual intervention and improve the uniformity of crop establishment. Another important advantage of automation and control systems is their ability to integrate with advanced monitoring technologies, allowing machines to receive real-time field feedback and adjust operations accordingly.

The automatic segment held 79% share in 2025. Automatic seed planting machines are designed to perform essential planting functions with minimal operator involvement once operational parameters have been configured. Integrated electronics and mechanical actuators control seed flow, maintain accurate spacing, and regulate planting depth throughout the operation. Guidance and alignment technologies ensure that rows remain consistent across the entire field. After the operator inputs the desired settings, the system independently maintains those parameters during the planting process, even when field conditions change. This level of automation reduces operator workload and enhances planting consistency by maintaining uniform performance regardless of operational speed or terrain conditions.

U.S. Smart Seed Planting Machine Market captured 79.7% share, generating USD 3.3 billion in 2025. The United States plays a significant role in advancing smart agricultural machinery due to its highly mechanized farming sector and strong adoption of innovative technologies. Large-scale farming operations, rising labor costs, and strong capital investment capabilities encourage producers to incorporate automation and precision planting technologies into their agricultural practices. The presence of major agricultural machinery manufacturers further strengthens the country's position by enabling easier access to advanced digital farming equipment. Additionally, the continued development of agritech innovation ecosystems is supporting the advancement of intelligent planting solutions across the U.S. agricultural landscape.

Major companies operating in the Global Smart Seed Planting Machine Market include Deere & Company, AGCO, CNH Industrial, Kubota, Mahindra & Mahindra, Trimble, CLAAS KGaA, Bourgault Industries, Kinze Manufacturing, Vaderstad AB, Agrisem International, MaterMacc, Semeato, Jumil, and Yetter Farm Equipment. Companies participating in the Smart Seed Planting Machine Market are implementing several strategic initiatives to strengthen their market position and expand their global footprint. Leading manufacturers are investing heavily in research and development to introduce advanced precision planting technologies that improve accuracy, automation, and operational efficiency. Many firms are focusing on integrating digital agriculture platforms, sensor-based technologies, and connectivity features to enhance machine intelligence and real-time data analysis capabilities. Strategic partnerships with agricultural technology providers and equipment distributors are also helping companies expand their reach across key farming regions. In addition, manufacturers are emphasizing product customization to meet diverse farming requirements and crop types.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Automation level

- 2.2.4 Crop type

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for precision agriculture

- 3.2.1.2 Shift toward large-scale mechanized farming

- 3.2.1.3 Labor shortages & rising wages

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital costs

- 3.2.2.2 Limited technical knowledge among farmers

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI-driven decision support

- 3.2.3.2 Growth of autonomous & electric planters

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Automation & control systems

- 5.2.1 Guidance systems

- 5.2.2 Drive systems

- 5.2.3 Display systems

- 5.2.4 Control systems

- 5.2.5 GPS receivers

- 5.2.6 Drones/UAVS

- 5.3 Sensing & monitoring devices

- 5.3.1 Smart metering systems

- 5.3.2 Sensors

- 5.3.3 Cameras

- 5.3.4 Delivery systems

Chapter 6 Market Estimates and Forecast, By Automation Level, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic

- 6.3 Manual

Chapter 7 Market Estimates and Forecast, By Crop Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Row crops

- 7.3 Grains & cereals

- 7.4 Pulses & oilseeds

- 7.5 Vegetables & fruits

- 7.6 Forestry

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Small farms (Below 400 hectares)

- 8.3 Large farms (Above 400 hectares)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Agrisem International

- 11.3 Bourgault Industries

- 11.4 CLAAS KGaA

- 11.5 CNH Industrial

- 11.6 Deere & Company

- 11.7 Jumil

- 11.8 Kinze Manufacturing

- 11.9 Kubota

- 11.10 Mahindra & Mahindra

- 11.11 MaterMacc

- 11.12 Semeato

- 11.13 Trimble

- 11.14 Vaderstad AB

- 11.15 Yetter Farm Equipment