PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998671

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998671

North America Eye Cream Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

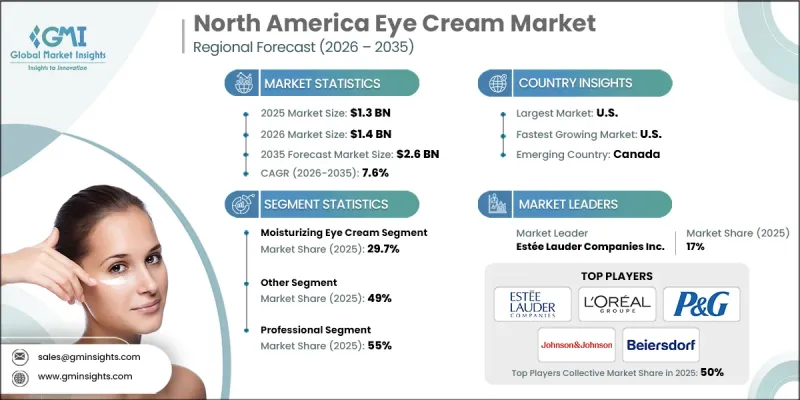

North America Eye Cream Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 2.6 billion by 2035.

The region represents one of the most mature and influential segments within the broader skincare industry, supported by well-informed consumers and a highly developed beauty and personal care ecosystem. Demand continues to rise as individuals prioritize targeted solutions formulated specifically for the delicate under-eye area. Growing awareness of visible skin concerns and heightened focus on maintaining a youthful appearance are reinforcing consistent product adoption. Preventive skincare practices and clinically supported formulations are shaping purchasing behavior across the region. Buyers are increasingly evaluating products based on their long-term benefits, ingredient integrity, and overall value. Although positioned as specialized skincare items, eye creams are no longer viewed solely as premium indulgences, but rather as routine essentials within daily regimens. Strong retail infrastructure, widespread product availability, and evolving consumer expectations are collectively supporting steady market expansion across North America.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 7.6% |

The moisturizing eye creams segment held 29.7% share, generating USD 400 million in 2025. Consumers across North America show consistent demand for formulations designed to deliver visible smoothing and revitalizing effects. Products positioned to enhance skin hydration and improve firmness continue to perform strongly, reflecting interest in effective yet accessible eye care solutions.

The professional-grade products segment accounted for 55% share in 2025, driven by increasing preference for advanced skincare treatments. These formulations typically feature higher concentrations of active ingredients and are distributed through controlled channels associated with skincare professionals. Consumers seeking targeted and performance-driven solutions are contributing to segment growth. The rising appeal of personalized skincare programs and confidence in professionally recommended regimens are further strengthening demand within this category.

United States Eye Cream Market generated USD 800 million in 2025 and is forecast to grow at a rate of 7.6% through 2035, positioning it as the second largest regional contributor within North America. The U.S. market demonstrates strong penetration of premium skincare brands and a robust direct-to-consumer landscape supported by advanced e-commerce infrastructure. Purchasing decisions are increasingly influenced by ingredient transparency, clean formulations, ethical sourcing claims, and environmentally responsible packaging, particularly among younger consumer demographics who prioritize brand authenticity and sustainability commitments.

Key participants shaping the North America Eye Cream Market include Procter & Gamble, L'Oreal Group, The Estee Lauder Companies Inc., Shiseido Company, Limited, Unilever PLC, Coty Inc., Johnson & Johnson Consumer Health, Beiersdorf AG, LVMH Moet Hennessy Louis Vuitton, Amorepacific Corporation, Murad, LLC, Supergoop! LLC, Proactiv Company, Alastin Skincare, Inc., and Deciem. Companies in the North America Eye Cream Market are reinforcing their competitive positions through continuous research and development, ingredient innovation, and strong brand storytelling. Market leaders invest in clinically tested formulations and dermatologist-backed claims to enhance product credibility. Strategic expansion across digital platforms and direct-to-consumer channels strengthens customer engagement and data-driven personalization. Many brands are emphasizing clean-label positioning, sustainable packaging initiatives, and ethical sourcing practices to align with evolving consumer values. Partnerships with skincare professionals and targeted marketing campaigns further elevate brand authority.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Country

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Type

- 2.2.3 Ingredient

- 2.2.4 Skin Type

- 2.2.5 Price

- 2.2.6 Application

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Aging & Preventive Skincare Demand

- 3.2.1.2 High Awareness of Ingredient Efficacy

- 3.2.1.3 Strong E-commerce & DTC Penetration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Market Saturation & Intense Competition

- 3.2.2.2 Price Sensitivity in Mass & Mid-Range Segments

- 3.2.3 Opportunities

- 3.2.3.1 Growth of Dermocosmetic & Clinical Eye Care

- 3.2.3.2 Sustainable & Clean Beauty Positioning

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Country

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 North America

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Moisturizing eye cream

- 5.3 Forming eye cream

- 5.4 Anti-aging eye cream

- 5.5 Anti-allergy eye cream

- 5.6 Brightening eye cream

- 5.7 De-puffing eye cream

Chapter 6 Estimates & Forecast, By Ingredient, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Vitamin E

- 6.3 Niacinamide

- 6.4 vitamin A

- 6.5 Retinol

- 6.6 Other (hyaluronic acid, etc)

Chapter 7 Market Estimates and Forecast, By Skin Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Dry skin

- 7.3 Oily skin

- 7.4 Other (all skin, sensitive skin)

Chapter 8 Estimates & Forecast, By Price 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Professional

- 9.3 Personal

Chapter 10 Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce websites

- 10.2.2 Company websites

- 10.3 Offline

- 10.3.1 Hypermarket/supermarket

- 10.3.2 Departmental stores

- 10.3.3 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

Chapter 12 Company Profiles

- 12.1 Alastin Skincare, Inc.

- 12.2 Amorepacific Corporation

- 12.3 Beiersdorf AG

- 12.4 Coty Inc.

- 12.5 Deciem

- 12.6 Johnson & Johnson Consumer Health

- 12.7 L’Oreal Group

- 12.8 LVMH Moet Hennessy Louis Vuitton

- 12.9 Murad, LLC

- 12.10 Proactiv Company

- 12.11 Procter & Gamble

- 12.12 Shiseido Company, Limited

- 12.13 Supergoop! LLC

- 12.14 The Estee Lauder Companies Inc.

- 12.15 Unilever PLC