PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998674

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998674

Power Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

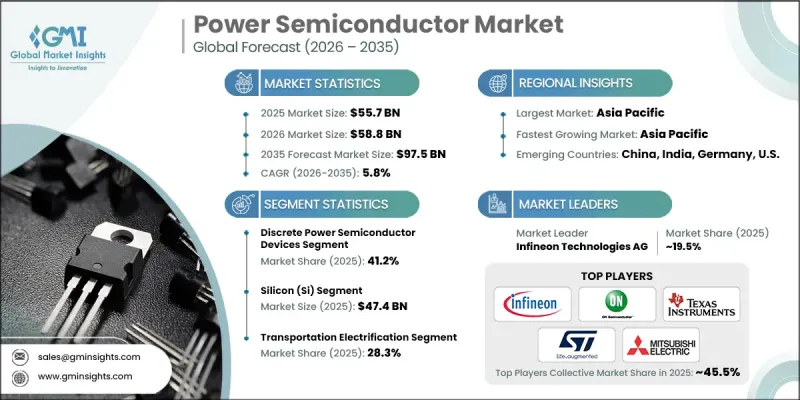

The Global Power Semiconductor Market was valued at USD 55.7 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 97.5 billion by 2035.

The power semiconductor market continues to gain momentum as multiple technology-driven industries increase their reliance on advanced power electronics. Growing electrification across transportation, the rising need for efficient power management, and the expanding footprint of digital infrastructure are contributing significantly to market expansion. Increased deployment of energy-efficient electronic systems and the evolution of high-performance power management technologies are further strengthening demand. Additionally, the continuous development of next-generation semiconductor materials is supporting improved efficiency and higher performance across a wide range of applications. Companies are also focusing on improving manufacturing capacity and strengthening supply chain resilience to support the increasing global demand for power semiconductors. As energy efficiency becomes a key priority for governments and industries worldwide, power semiconductor technologies are becoming essential components in modern electronic systems. These combined factors are expected to support the sustained growth of the global power semiconductor market over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $55.7 Billion |

| Forecast Value | $97.5 Billion |

| CAGR | 5.8% |

Rapid electrification of transportation systems continues to play a critical role in the growth of the power semiconductor market. Increasing vehicle production that relies on advanced power electronics has significantly strengthened demand for high-performance semiconductor components. These devices support efficient energy conversion, voltage regulation, and power management within modern vehicle architectures. At the same time, industrial facilities are increasingly transitioning toward advanced automation technologies designed to improve operational efficiency and reduce energy consumption. The expansion of digital infrastructure and computing facilities worldwide is also raising demand for reliable power management solutions capable of supporting high-performance electronic systems. The development of advanced charging infrastructure and improved energy systems further contributes to rising semiconductor adoption.

The discrete power semiconductor devices segment accounted for 41.2% share in 2025. This segment maintains a strong position due to the extensive use of individual semiconductor components across multiple electronic systems. Discrete devices remain widely adopted because they offer cost efficiency, operational flexibility, and design adaptability for various power management requirements. Their ability to perform essential switching and power control functions across numerous electronic applications supports consistent demand in both consumer-oriented and industrial environments. In addition, the scalability of discrete semiconductor solutions allows manufacturers to integrate them easily into a broad range of power electronics architectures. As industries continue to adopt advanced electrical systems requiring reliable power regulation, the importance of discrete power semiconductor devices is expected to remain significant throughout the forecast period.

The silicon segment reached USD 47.4 billion in 2025. Silicon-based semiconductor technologies continue to maintain a strong industry position due to their mature manufacturing infrastructure and widespread commercial availability. The well-established production ecosystem surrounding silicon devices allows manufacturers to achieve cost efficiency while maintaining reliable performance standards. Silicon power devices are widely implemented in various electronic systems requiring stable power conversion and voltage management. Their long history of industrial use, standardized design frameworks, and broad supplier network contribute to sustained demand in the global semiconductor landscape. As a result, silicon remains a core material within the power semiconductor market despite the emergence of alternative semiconductor technologies.

North America Power Semiconductor Market represented 21.9% share in 2025. The region continues to experience steady expansion due to increasing electrification initiatives and rising energy-efficiency requirements across multiple sectors. Infrastructure modernization efforts and the transition toward more advanced electrical systems are contributing to higher demand for sophisticated semiconductor components in the region. Businesses across industrial and commercial environments are investing in technologies designed to improve power management and optimize energy consumption. In addition, the expanding digital ecosystem and increasing reliance on advanced electronic systems continue to drive semiconductor demand across North America. As industries focus on improving operational efficiency while reducing energy losses, the integration of advanced power electronics is becoming increasingly important across the regional technology landscape.

Leading companies operating in the Global Power Semiconductor Market include Infineon Technologies AG, Mitsubishi Electric Corporation, STMicroelectronics NV, Fuji Electric Co., Ltd., Texas Instruments Inc., Renesas Electronics Corporation, Toshiba Corporation (E-Devices), NXP Semiconductors NV, ON Semiconductor (onsemi), Vishay Intertechnology, Inc., ROHM Semiconductor, Littelfuse, Inc., Wolfspeed, Inc., Semikron International GmbH, Powerex, Inc., and Shindengen Electric Manufacturing Co., Ltd. Companies participating in the Global Power Semiconductor Market are implementing several strategic initiatives to strengthen their competitive position and expand their technological capabilities. Many firms are investing heavily in research and development to create advanced semiconductor materials and improve device efficiency, power density, and thermal performance. Expanding manufacturing capacity and building vertically integrated production systems are also key priorities, enabling companies to secure supply stability and reduce dependence on external suppliers. Strategic collaborations and partnerships with technology developers and industrial customers help companies accelerate innovation and broaden application opportunities. Businesses are also focusing on strengthening regional manufacturing footprints to enhance supply chain resilience.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product form trends

- 2.2.2 Material type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption increasing IGBT and SiC demand

- 3.2.1.2 Industrial automation growth raising demand for power modules

- 3.2.1.3 Energy efficiency regulations mandating advanced power electronics

- 3.2.1.4 Data center power optimization increasing MOSFET consumption

- 3.2.1.5 Fast-charging infrastructure expansion boosting wide-bandgap semiconductors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing cost of SiC and GaN devices

- 3.2.2.2 Supply chain dependence on limited wafer suppliers

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of SiC in 800V electric vehicle platforms

- 3.2.3.2 Smart grid upgrades increasing demand for high-power discrete devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Form, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Discrete power semiconductor devices

- 5.2.1 Discrete power transistors

- 5.2.1.1 Discrete MOSFETs

- 5.2.1.2 Discrete IGBTs

- 5.2.1.3 Other discrete power transistors

- 5.2.2 Discrete power diodes & rectifiers

- 5.2.2.1 Rectifier diodes (PN junction)

- 5.2.2.2 Schottky barrier diodes

- 5.2.2.3 Fast & ultra-fast recovery diodes

- 5.2.3 Discrete thyristors & AC power control devices

- 5.2.3.1 SCR / thyristors

- 5.2.3.2 TRIACs and other AC power control devices

- 5.2.1 Discrete power transistors

- 5.3 Power modules

- 5.3.1 IGBT modules

- 5.3.2 MOSFET modules

- 5.3.3 Diode & thyristor modules

- 5.3.4 Hybrid & mixed-technology modules

- 5.3.5 Intelligent power modules (IPMs)

- 5.4 Power Integrated Circuits (Power ICs)

- 5.4.1 DC-DC converter ICs

- 5.4.2 AC-DC controller & converter ICs

- 5.4.3 Gate driver ICs

- 5.4.4 Power management ICs (PMICs)

- 5.4.5 Motor control & driver ICs

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Silicon (Si)

- 6.3 Silicon carbide (SiC)

- 6.4 Gallium nitride (GaN)

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Transportation electrification

- 7.3 Power generation, transmission & distribution infrastructure

- 7.4 Industrial manufacturing & automation

- 7.5 Consumer

- 7.6 ICT infrastructure

- 7.7 Commercial buildings & infrastructure

- 7.8 Aerospace, defense & space

- 7.9 Healthcare equipment

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Infineon Technologies AG

- 9.1.2 STMicroelectronics NV

- 9.1.3 Texas Instruments Inc.

- 9.1.4 Mitsubishi Electric Corporation

- 9.1.5 NXP Semiconductors NV

- 9.1.6 Renesas Electronics Corporation

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 ON Semiconductor (onsemi)

- 9.2.1.2 Littelfuse, Inc.

- 9.2.1.3 Powerex, Inc.

- 9.2.2 Asia Pacific

- 9.2.2.1 ROHM Semiconductor

- 9.2.2.2 Fuji Electric Co., Ltd.

- 9.2.2.3 Toshiba Corporation (E-Devices)

- 9.2.2.4 Shindengen Electric Manufacturing Co., Ltd.

- 9.2.3 Europe

- 9.2.3.1 Semikron International GmbH

- 9.2.3.2 Vishay Intertechnology, Inc.

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Wolfspeed, Inc.