PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998682

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998682

Atopic Dermatitis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

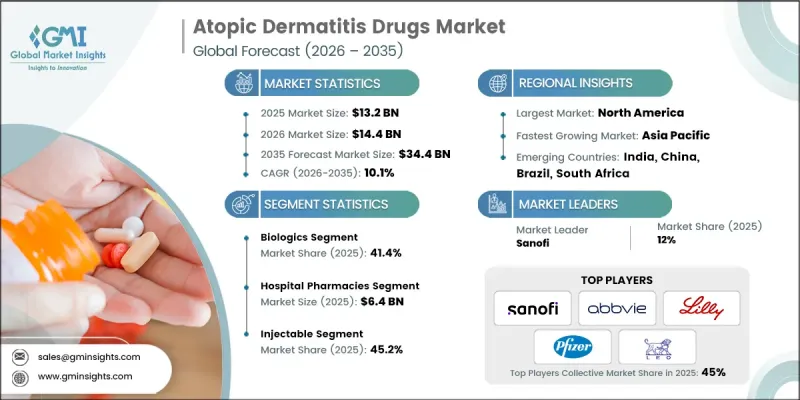

The Global Atopic Dermatitis Drugs Market was valued at USD 13.2 billion in 2025 and is estimated to grow at a CAGR of 10.1% to reach USD 34.4 billion by 2035.

The market for atopic dermatitis therapeutics is experiencing strong expansion, largely driven by the increasing global prevalence of this chronic inflammatory skin disorder and the rapid development of innovative treatment options. Atopic dermatitis continues to affect a growing number of individuals across both pediatric and adult populations, creating sustained demand for effective long-term treatment solutions. Pharmaceutical companies are actively investing in research and development to introduce advanced therapies capable of delivering improved symptom control and disease management. Continuous innovation in dermatology treatments is expanding the range of available therapeutic approaches, allowing physicians to tailor treatment strategies to individual patient needs. In addition, emerging topical and systemic therapies are contributing to the transformation of treatment frameworks for mild, moderate, and severe disease stages. As new therapies gain wider clinical acceptance and demonstrate favorable long-term outcomes in real-world use, their adoption continues to increase. The growing availability of diverse treatment classes and administration routes is helping to strengthen the therapeutic landscape and is expected to support sustained growth in the atopic dermatitis drugs market over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.2 Billion |

| Forecast Value | $34.4 Billion |

| CAGR | 10.1% |

Atopic dermatitis drugs are pharmaceutical therapies developed to manage the symptoms and progression of atopic dermatitis, a chronic skin condition characterized by inflammation, persistent itching, and dryness. These medications aim to reduce inflammatory responses, relieve discomfort associated with flare-ups, and help maintain a healthy skin condition over time. Treatment approaches are designed to control symptoms, prevent disease recurrence, and support long-term disease management through targeted therapeutic mechanisms.

The biologics segment held a 41.4% share in 2025. Biologic therapies have become an important treatment option for patients experiencing moderate to severe disease conditions because they provide highly targeted intervention within specific inflammatory pathways associated with atopic dermatitis. These therapies act by selectively regulating key immune signaling molecules that contribute to chronic inflammation. As a result, biologics can deliver sustained symptom control, reduce the frequency of disease flare-ups, and significantly improve skin health and patient quality of life. Their ability to target precise molecular drivers of inflammation rather than suppressing the immune system broadly has strengthened their clinical effectiveness while supporting favorable long-term safety outcomes for patients requiring ongoing treatment.

The injectable segment generated 45.2% share in 2025. Growth in this segment is closely linked to the increasing availability of advanced injectable therapies that focus on regulating specific inflammatory pathways involved in disease progression. The expansion of targeted treatment options has contributed significantly to the adoption of injectable medications for patients with moderate to severe forms of the condition. In addition, regulatory authorities across major pharmaceutical markets have granted approvals for several injectable therapies intended for the management of atopic dermatitis. These regulatory approvals have accelerated the introduction of new treatments into clinical practice, allowing healthcare providers to access a broader selection of effective therapeutic solutions and increasing adoption across healthcare systems.

North America Atopic Dermatitis Drugs Market held a significant share in 2025. The region maintains a strong position due to its advanced dermatology care infrastructure, high accessibility to modern treatment options, and rapid adoption of innovative therapies, including biologics and targeted immunomodulatory medications. Well-established regulatory frameworks across the region ensure consistent evaluation and approval of new dermatology therapies while maintaining high clinical safety standards. A major factor supporting regional market leadership is the substantial prevalence of atopic dermatitis among the population, which continues to drive demand for advanced treatment solutions. Patients experiencing moderate to severe disease conditions are increasingly seeking newer therapeutic options capable of providing more effective symptom control and long-term disease management, further strengthening the regional market outlook.

Prominent companies operating in the Global Atopic Dermatitis Drugs Market include Sanofi, Pfizer, AbbVie, Eli Lilly and Company, Leo Pharma, Galderma Laboratories, Incyte Corporation, Otsuka Pharmaceutical, Maruho, Arcutis Biotherapeutics, Chugai Pharmaceutical, and Viatris. Companies competing in the Global Atopic Dermatitis Drugs Market are adopting multiple strategic initiatives to reinforce their market presence and strengthen competitive positioning. Major pharmaceutical manufacturers are prioritizing extensive research and development efforts aimed at discovering innovative therapies that target specific immune pathways associated with inflammatory skin diseases. Many organizations are also investing in the development of advanced biologic treatments, targeted immunomodulators, and improved topical formulations to enhance therapeutic effectiveness and patient outcomes. Strategic collaborations with biotechnology firms and research institutions are accelerating drug discovery and clinical development activities. In addition, companies are expanding their product pipelines, pursuing regulatory approvals across global markets, and strengthening commercial distribution networks. Continuous investment in clinical trials, technological innovation, and global market expansion remains essential for sustaining long-term growth within the atopic dermatitis drugs market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Drug class trends

- 2.2.2 Route of administration trends

- 2.2.3 Patient demographics trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of atopic dermatitis

- 3.2.1.2 Advancements in biologic therapies

- 3.2.1.3 Growing awareness and access to dermatological care

- 3.2.1.4 Strengthening clinical pipeline

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of biologic and advanced therapies

- 3.2.2.2 Side effects and compliance issues

- 3.2.3 Market opportunity

- 3.2.3.1 Expansion of topical innovation and non-steroidal therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Pipeline analysis (Driven by Primary Research)

- 3.8 Impact of AI and generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Calcineurin inhibitors

- 5.4 Biologics

- 5.5 Phosphodiesterase-4 (PDE-4) inhibitors

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Oral

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Patient Demographics, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Arcutis Biotherapeutics

- 10.3 Chugai Pharmaceutical

- 10.4 Eli Lilly and Company

- 10.5 Galderma Laboratories

- 10.6 Incyte Corporation

- 10.7 Leo Pharma

- 10.8 Maruho

- 10.9 Otsuka Pharmaceutical

- 10.10 Pfizer

- 10.11 Sanofi

- 10.12 Viatris