PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998700

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998700

Atrial Fibrillation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

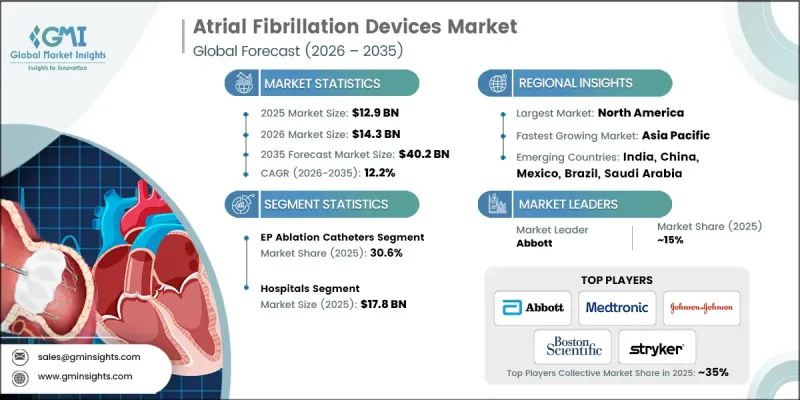

The Global Atrial Fibrillation Devices Market was valued at USD 12.9 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 40.2 billion by 2035.

Market expansion is driven by ongoing technological innovations in AF devices, the rising prevalence of atrial fibrillation, increasing adoption of cardiac ablation procedures, and heightened awareness about early diagnosis and management. AF devices, including ablation catheters, implantable cardiac monitors, pacemakers, and defibrillators, are designed to restore normal heart rhythm, prevent stroke, and reduce AF-related symptoms. Public health campaigns and patient education programs are promoting early detection and timely intervention, boosting demand for diagnostic and monitoring tools. Minimally invasive procedures, wearable and remote monitoring technologies, and hybrid treatment approaches are gaining traction, further accelerating market growth. Continuous innovation in energy delivery systems, precision targeting, and device miniaturization is expanding AF treatment options and improving procedural outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.9 Billion |

| Forecast Value | $40.2 Billion |

| CAGR | 12.2% |

The EP ablation catheters segment held a 30.6% share in 2025 owing to their central role in catheter-based ablation procedures. These devices allow precise lesion formation, improved tissue targeting, and higher procedural success rates, making them the preferred choice among electrophysiologists. Innovations such as irrigated tip catheters, contact force-sensing technology, and enhanced energy delivery systems are improving patient safety, increasing procedural efficiency, reducing treatment time, and driving further adoption.

The hospitals segment captured a 43.7% share in 2025 and is expected to reach USD 17.8 billion by 2035. Demand is being fueled by specialized AF treatment centers within hospitals, which require comprehensive device inventories for diagnosis, treatment, and patient monitoring. Accreditation programs and quality improvement initiatives motivate hospitals to procure advanced AF devices, increasing market uptake.

North America Atrial Fibrillation Devices Market held a 40.6% share in 2025, driven by a high prevalence of atrial fibrillation, an aging population, and the rising incidence of cardiovascular risk factors such as hypertension, diabetes, and obesity. The region's substantial healthcare expenditure supports investment in advanced AF technologies, including ablation catheters, pacemakers, and diagnostic devices. Early adoption of innovative solutions by healthcare providers, along with per capita spending on cardiac care, further strengthens regional growth.

Prominent players in the Global Atrial Fibrillation Devices Market include Abbott, Acutus Medical, AtriCure, Biotronik, Boston Scientific Corporation, CardioFocus, CathRx, Hansen Medical, Imricor, Johnson and Johnson, Medtronic, MicroPort Scientific Corporation, OSYPKA MEDICAL, Stryker Corporation, and Synaptic Medical. Key strategies adopted by companies in minimally invasive, energy-efficient, and precision ablation technologies; expanding product portfolios to include remote monitoring and wearable solutions; forming strategic partnerships with hospitals, clinics, and diagnostic centers; pursuing regulatory approvals and certifications to enter new markets; enhancing global distribution networks to improve accessibility; and implementing patient awareness campaigns to drive early diagnosis. Firms also focus on clinician training programs, after-sales service, and hybrid procedural solutions to strengthen their market footprint, build brand loyalty, and maintain competitive advantage.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High adoption rate of advanced technologies and presence of sophisticated healthcare infrastructure

- 3.2.1.2 Increase in prevalence of cardiovascular diseases

- 3.2.1.3 Favorable reimbursement scenario

- 3.2.1.4 Rise in prevalence of rheumatic valvular heart diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with atrial fibrillation devices

- 3.2.2.2 Lack of awareness regarding enhanced medical technologies in developing countries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of minimally invasive and catheter-based therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Atrial fibrillation devices market, 2022 -2035 (Units)

- 3.7.1 Global

- 3.7.2 North America

- 3.7.3 Europe

- 3.7.4 Asia Pacific

- 3.7.5 Latin America

- 3.7.6 MEA

- 3.8 Catheter ablation centres, by region, 2022 - 2025

- 3.9 Patent analysis

- 3.10 Pricing analysis, 2025 (Driven by Primary Research)

- 3.11 Customer insights

- 3.12 Impact of AI and generative AI on the market

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 EP ablation catheters

- 5.2.1 Radiofrequency (RF)

- 5.2.2 Laser

- 5.2.3 Cryoablation

- 5.2.4 Ultrasound

- 5.2.5 Microwave

- 5.2.6 Other EP ablation catheters

- 5.3 Cardiac monitors or implantable loop recorder

- 5.4 EP diagnostic catheters

- 5.4.1 Advanced mapping catheters

- 5.4.2 Steerable catheters

- 5.4.3 Fixed curve catheters

- 5.5 Mapping and recording systems

- 5.6 Access devices

- 5.7 Intracardiac echocardiography (ICE)

- 5.8 Left atrial appendage (LAA) closure devices

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Cardiac centers

- 6.4 Ambulatory surgical centers

- 6.5 Other end-users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Acutus Medical

- 8.3 AtriCure

- 8.4 Biotronik

- 8.5 Boston Scientific Corporation

- 8.6 CardioFocus

- 8.7 CathRx

- 8.8 Hansen Medical

- 8.9 Imricor

- 8.10 Johnson and Johnson

- 8.11 Medtronic

- 8.12 MicroPort Scientific Corporation

- 8.13 OSYPKA MEDICAL

- 8.14 Stryker Corporation

- 8.15 Synaptic Medical