PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998712

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998712

Veterinary ECG Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

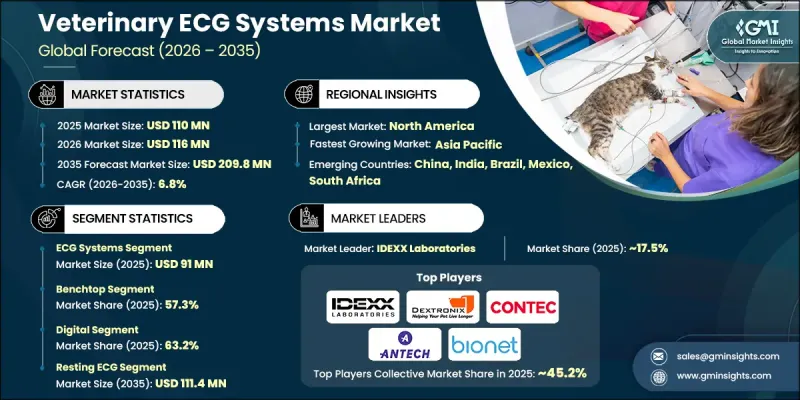

The Global Veterinary ECG Systems Market was valued at USD 110 million in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 209.8 million by 2035.

Rising awareness regarding animal health and increasing spending on veterinary care are major factors contributing to market growth. Veterinary electrocardiogram systems are non-invasive diagnostic devices designed to record and analyze the electrical activity of the heart, enabling veterinarians to evaluate cardiac performance and identify abnormalities. As veterinary infrastructure expands and the number of specialized clinics and hospitals continues to grow, demand for advanced diagnostic technologies is increasing significantly. Improvements in veterinary medical technology are also enhancing the accuracy and usability of cardiac monitoring equipment. The introduction of digital platforms, wireless connectivity, and compact diagnostic tools is transforming how cardiac assessments are performed in veterinary practice. At the same time, the growing availability of pet insurance and improved access to professional veterinary services are supporting greater adoption of modern diagnostic equipment. These combined developments are creating favorable conditions for the continued expansion of the veterinary ECG systems market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $110 Million |

| Forecast Value | $209.8 Million |

| CAGR | 6.8% |

Another important factor supporting the growth of the veterinary ECG systems market is the increasing occurrence of cardiac disorders in animals. Various heart-related conditions affecting animals require timely diagnosis and consistent monitoring to ensure effective treatment and long-term management. Veterinary professionals increasingly rely on ECG monitoring technologies because they provide precise and non-invasive methods for evaluating heart rhythm and electrical activity. As veterinary clinics and hospitals focus more on preventive care and early disease detection, the demand for reliable cardiac diagnostic equipment is rising steadily. Veterinary ECG systems play a crucial role in identifying abnormalities in heart function and enabling clinicians to monitor patient conditions over time.

The ECG systems segment accounted for USD 91 million in 2025. These systems serve as a fundamental diagnostic solution for monitoring heart rate patterns and detecting irregular cardiac activity in animals. Their role in identifying cardiovascular conditions has made them an essential component of veterinary diagnostic procedures. The increasing detection of complex cardiac complications among aging pets has contributed to the rising use of these systems across veterinary hospitals and specialized clinics. Additionally, heightened awareness among animal owners regarding potential heart-related health issues has increased the demand for advanced diagnostic testing. The growing popularity of portable and wireless ECG solutions has further supported segment expansion by enabling veterinarians to conduct real-time cardiac monitoring in both clinical environments and field-based veterinary practices.

Based on product configuration, the benchtop segment held a share of 57.3% in 2025. Benchtop systems remain widely used within veterinary practices because they provide reliable and detailed cardiac monitoring capabilities. These systems can record multiple ECG channels simultaneously, which allows veterinarians to conduct comprehensive cardiac assessments across a variety of animal species. Their ability to deliver highly accurate diagnostic data makes them particularly valuable in veterinary hospitals and diagnostic centers where detailed cardiac analysis is required. Benchtop ECG devices are often integrated with other diagnostic technologies and information management systems, which helps streamline clinical workflows and improve data management. Such integration enhances efficiency within veterinary facilities and supports more informed medical decision-making, ultimately contributing to better patient outcomes and sustained demand for these systems.

North America Veterinary ECG Systems Market held a 37.9% share in 2025. The region's leadership position is supported by a well-developed veterinary healthcare infrastructure and a high level of spending on animal healthcare services. Strong awareness regarding animal health and the widespread adoption of advanced veterinary diagnostic technologies are further contributing to market growth. In addition, the availability of specialized veterinary medical services and advanced treatment facilities is driving demand for sophisticated cardiac monitoring solutions. The presence of numerous industry participants and continuous technological innovation within the region is also helping strengthen market development, enabling veterinary clinics and hospitals to adopt modern ECG systems designed to support efficient and accurate cardiac diagnostics.

Prominent companies operating in the Global Veterinary ECG Systems Market include Antech Diagnostics (Mars Petcare), Aspel, Bionet America, Contec Medical Systems, Dextronix, Dawei Veterinary Medical (Jiangsu), Eickemeyer Veterinary Equipment, IDEXX Laboratories, Narang Medical Limited, New Gen Medical Systems, Shenzhen Comen Medical Instruments, Technocare Medisystems, Vmed Technology, and VectraCor. Companies competing in the Global Veterinary ECG Systems Market are implementing a variety of strategic initiatives to strengthen their market presence and expand their customer base. Manufacturers are increasingly focusing on product innovation by developing compact, wireless, and technologically advanced ECG solutions that improve diagnostic accuracy and ease of use. Many organizations are also investing in research and development to enhance device functionality, connectivity, and data analysis capabilities. Strategic collaborations with veterinary hospitals, diagnostic laboratories, and research institutions are helping companies expand their distribution networks and improve product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Modality trends

- 2.2.4 Technology trends

- 2.2.5 Usage trends

- 2.2.6 Animal type trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and pet humanization

- 3.2.1.2 Increase in cardiac disorders among animals

- 3.2.1.3 Technological advancements in veterinary ECG systems

- 3.2.1.4 Growth in veterinary healthcare infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary ECG systems

- 3.2.2.2 Limited awareness in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of portable and wireless ECG technologies

- 3.2.3.2 Increasing adoption of telecardiology services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies and their impact

- 3.6 Pet population, by country

- 3.7 Patent analysis

- 3.8 Pricing analysis (Driven by primary research)

- 3.9 Future market trends (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 -2035 ($ Mn)

- 5.1 Key trends

- 5.2 ECG systems

- 5.3 Accessories and consumables

Chapter 6 Market Estimates and Forecast, By Modality, 2022 -2035 ($ Mn)

- 6.1 Key trends

- 6.2 Handheld

- 6.3 Benchtop

Chapter 7 Market Estimates and Forecast, By Technology, 2022 -2035 ($ Mn)

- 7.1 Key trends

- 7.2 Digital

- 7.3 Analog

Chapter 8 Market Estimates and Forecast, By Usage, 2022 -2035 ($ Mn)

- 8.1 Key trends

- 8.2 Resting ECG

- 8.3 Holter ECG

Chapter 9 Market Estimates and Forecast, By Animal Type, 2022 -2035 ($ Mn)

- 9.1 Key trends

- 9.2 Small companion animals

- 9.2.1 Dogs

- 9.2.2 Cats

- 9.2.3 Other small companion animals

- 9.3 Large animals

- 9.3.1 Horses

- 9.3.2 Cattle

- 9.3.3 Swine

- 9.3.4 Sheep & goats

- 9.3.5 Other large animals

Chapter 10 Market Estimates and Forecast, By End Use, 2022 -2035 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Academic and research institutions

- 10.4 Other end users

Chapter 11 Market Estimates and Forecast, By Region, 2022 -2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Antech Diagnostics

- 12.2 Aspel

- 12.3 Bionet America

- 12.4 Contec Medical Systems

- 12.5 Dextronix

- 12.6 Dawei Veterinary Medical (Jiangsu)

- 12.7 Eickemeyer Veterinary Equipment

- 12.8 IDEXX Laboratories

- 12.9 Narang Medical Limited

- 12.10 New Gen Medical Systems

- 12.11 Shenzhen Comen Medical Instruments

- 12.12 Technocare Medisystems

- 12.13 Vmed Technology

- 12.14 VectraCor